Strategy UtilitiesThis library comprises valuable functions for implementing strategies on TradingView, articulated in a professional writing style.

The initial version features a monthly Profit & Loss table with percentage variations, utilizing a modified version of the script by @QuantNomad.

Library "strategy_utilities"

monthly_table(results_prec, results_dark)

monthly_table prints the Monthly Returns table, modified from QuantNomad. Please put calc_on_every_tick = true to plot it.

Parameters:

results_prec (int) : for the precision for decimals

results_dark (bool) : true or false to print the table in dark mode

Returns: nothing (void), but prints the monthly equity table

Sample Usage

import TheSocialCryptoClub/strategy_utilities/1 as su

results_prec = input(2, title = "Precision", group="Results Table")

results_dark = input.bool(defval=true, title="Dark Mode", group="Results Table")

su.monthly_table(results_prec, results_dark)

Göstergeler ve stratejiler

Uptrend Downtrend Loopback Candle Identification LibThis library is for identifying uptrends and downtrends using a loopback candle analysis method. Which contains two functions:

uptrendLoopbackCandleIdentification() and downtrendLoopbackCandleIdentification() . These functions check if the current candle is part of an uptrend or downtrend, respectively, based on the specified lookback period.

The uptrendLoopbackCandleIdentification() takes two arguments: index , which is the index of the current bar, and lookbackPeriod , which is the number of previous candles to check for an uptrend. The function returns false if the index is less than the lookback period. Otherwise, it initializes a boolean variable isHigherHigh as true and loops through the previous candles. If any of the previous candles have a higher high than the current candle, isHigherHigh is set to false , and the loop breaks. Finally, the function returns the value of isHigherHigh .

The downtrendLoopbackCandleIdentification() takes the same arguments and returns false if the index is less than the lookback period. The function initializes a boolean variable isHigherLow as true and loops through the previous candles. If any of the previous candles have a higher low than the current candle, isHigherLow is set to false , and the loop breaks. The function returns the value of isHigherLow .

BankNifty_CSMLibrary "BankNifty_CSM"

TODO: add library description here

getLtp_N_Chang(openPrice, closePrice, highPrice, hl2Price, lowPrice, hlc3Price, bankNiftyClose)

Parameters:

openPrice (float)

closePrice (float)

highPrice (float)

hl2Price (float)

lowPrice (float)

hlc3Price (float)

bankNiftyClose (float)

ka66: lib/MovingAveragesLibrary "MovingAverages"

Exotic or Interesting Moving Averages Collection. Just the one right now!

alphaConfigurableEma(src, alpha, nSmooth)

Calculates a variation of the EMA by specifying a custom alpha value.

Parameters:

src (float) : a float series to get the EMA for, e.g. close, hlc3, etc.

alpha (float) : a value between 0 (ideally greater, to get any MA!) and 1. Closer

to one makes it more responsive, and choppier.

nSmooth (int) : Just applies the same alpha and EMA to the last Alpha-EMA output.

A value between 0 and 10 (just keeping a a reasonable bound). The idea is

you can first use a reasonably high alpha, then smooth it out. Default 0,

no further smoothing.

Returns: MA series.

bands(src, multiplier)

Calculates fixed bands around a series, can be any series, though the intent

here is for MA series.

Parameters:

src (float) : a float series.

multiplier (float) : a value greater than or equal to 0 (ideally greater, to get any MA!),

determines the width of the bands. Start with small float values, or it may go

beyond the scale, e.g. 0.005.

Returns: a 2-tuple of (upBand, downBand)

Spider_PlotIntroduction:

Spider charts, also known as radar charts or web charts, are a powerful data visualization tool that can display multiple variables in a circular format. They are particularly useful when you want to compare different data sets or evaluate the performance of a single data set across multiple dimensions. In this blog post, we will dive into the world of spider charts, explore their benefits, and demonstrate how you can create your own spider chart using the Spider_Plot library.

Why Spider Charts are Cool:

Spider charts have a unique visual appeal that sets them apart from other chart types. They allow you to display complex data in a compact, easy-to-understand format, making them perfect for situations where you need to convey a lot of information in a limited space. Some of the key benefits of spider charts include:

Multi-dimensional analysis: Spider charts can display multiple variables at once, making them ideal for analyzing relationships between different data sets or examining a single data set across multiple dimensions.

Easy comparison: By displaying data in a circular format, spider charts make it simple to compare different data points, identify trends, and spot potential issues.

Versatility: Spider charts can be used for a wide range of applications, from business and finance to sports and health. They are particularly useful for situations where you need to analyze performance or make comparisons between different entities.

Creating Your Own Spider Chart with the Spider_Plot Library:

The Spider_Plot library is a user-friendly, easy-to-use tool that allows you to create stunning spider charts with minimal effort. To get started, you'll need to import the Spider_Plot library:

import peacefulLizard50262/Spider_Plot/1

With the library imported, you can now create your own spider chart. The first step is to normalize your data. Normalizing ensures that all data points fall within the 0 to 1 range, which is important for creating a visually balanced spider chart.

The Spider_Plot library provides the data_normalize function to help you normalize your data. This function accepts several parameters, including the normalization style ("All Time", "Range", or "Custom"), length of the range, outlier level, lookback period for standard deviation, and minimum and maximum values for the "Custom" normalization style.

Once you have normalized your data, you can create an array of your data points using the array.from function. This array will be used as input for the draw_spider_plot function, which is responsible for drawing the spider plot on your chart.

The draw_spider_plot function accepts an array of float values (the normalized data points), an array of background colors for each sector, a color for the axes, and a scaling factor.

Example Usage:

Here's an example script that demonstrates how to create a spider chart using the Spider_Plot library:

oc = data_normalize(ta.ema(math.abs(open - close), 20), "Range", 20)

// Create an array of your data points

data = array.from(tr, rsi, stoch, dev, tr, oc, tr)

// Define colors for each sector

colors = array.from(color.new(color.red, 90), color.new(color.blue, 90), color.new(color.green, 90), color.new(color.orange, 90), color.new(color.purple, 90), color.new(color.purple, 90), color.new(color.purple, 90))

// Draw the spider plot on your chart

draw_spider_plot(data, colors, color.gray, 100)

In this example, we have first normalized six different data points (rsi, source, stoch, dev, tr, and oc) using the data_normalize function. Next, we create an array of these normalized data points and define an array of colors for each sector of the spider chart. Finally, we call the draw_spider_plot function to draw the spider chart on our chart.

Conclusion:

Spider charts are a versatile and visually appealing tool for analyzing and comparing multi-dimensional data. With the Spider_Plot library, you can easily create your own spider charts and unlock valuable insights from your data. Just remember to normalize your data and create an array of data points before calling the draw_spider_plot function. Happy charting!

Library "Spider_Plot"

data_normalize(data, style, length, outlier_level, dev_lookback, min, max)

data_normalize(data, string style, int length, float outlier_level, simple int dev_lookback, float min, float max)

Parameters:

data (float) : float , A float value to normalize.

style (string) : string , The normalization style: "All Time", "Range", or "Custom".

length (int) : int , The length of the range for "Range" normalization style.

outlier_level (float) : float , The outlier level to exclude from calculations.

dev_lookback (simple int) : int , The lookback period for calculating the standard deviation.

min (float) : float , The minimum value for the "Custom" normalization style.

max (float) : float , The maximum value for the "Custom" normalization style.

Returns: array , The normalized float value.

draw_spider_plot(values, bg_colors, axes_color, scale)

draw_spider_plot(array values, array bg_colors, color axes_color, float scale)

Parameters:

values (float ) : array , An array of float values to plot in the spider plot.

bg_colors (color ) : array , An array of background colors for each sector in the spider plot.

axes_color (color) : color , The color of the axes in the spider plot. Default: color.gray

scale (float) : float , A scaling factor for the spider plot. Default: 10

Returns: void , Draws the spider plot on the chart.

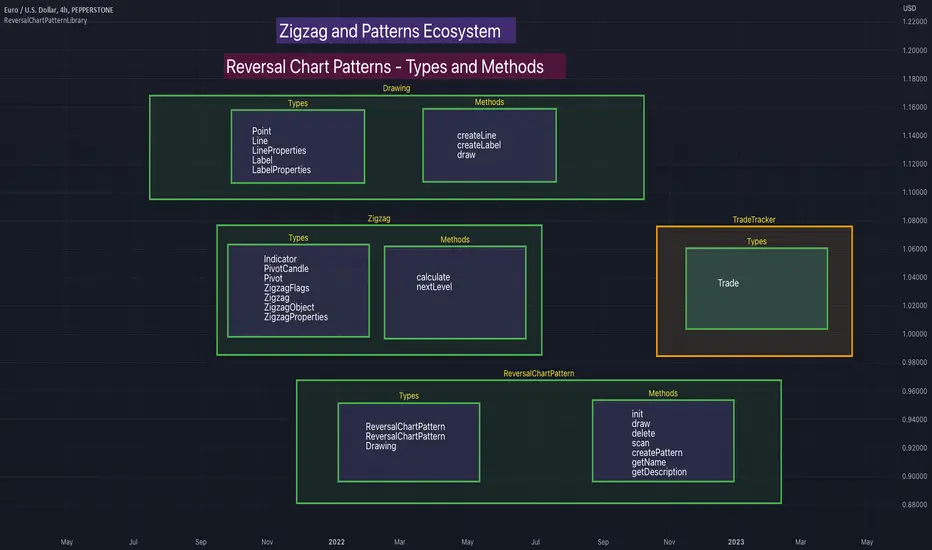

ReversalChartPatternLibraryLibrary "ReversalChartPatternLibrary"

User Defined Types and Methods for reversal chart patterns - Double Top, Double Bottom, Triple Top, Triple Bottom, Cup and Handle, Inverted Cup and Handle, Head and Shoulders, Inverse Head and Shoulders

method delete(this)

Deletes the drawing components of ReversalChartPatternDrawing object

Namespace types: ReversalChartPatternDrawing

Parameters:

this (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object

Returns: current ReversalChartPatternDrawing object

method delete(this)

Deletes the drawing components of ReversalChartPattern object. In turn calls the delete of ReversalChartPatternDrawing

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: current ReversalChartPattern object

method lpush(this, obj, limit, deleteOld)

Array push with limited number of items in the array. Old items are deleted when new one comes and exceeds the limit

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern ) : array object

obj (ReversalChartPattern) : ReversalChartPattern object which need to be pushed to the array

limit (int) : max items on the array. Default is 10

deleteOld (bool) : If set to true, also deletes the drawing objects. If not, the drawing objects are kept but the pattern object is removed from array. Default is false.

Returns: current ReversalChartPattern object

method draw(this)

Draws the components of ReversalChartPatternDrawing

Namespace types: ReversalChartPatternDrawing

Parameters:

this (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object

Returns: current ReversalChartPatternDrawing object

method draw(this)

Draws the components of ReversalChartPatternDrawing within the ReversalChartPattern object.

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: current ReversalChartPattern object

method scan(zigzag, patterns, errorPercent, shoulderStart, shoulderEnd)

Scans zigzag for ReversalChartPattern occurences

Namespace types: zg.Zigzag

Parameters:

zigzag (Zigzag type from HeWhoMustNotBeNamed/ZigzagTypes/2) : ZigzagTypes.Zigzag object having array of zigzag pivots and other information on each pivots

patterns (ReversalChartPattern ) : Existing patterns array. Used for validating duplicates

errorPercent (float) : Error threshold for considering ratios. Default is 13

shoulderStart (float) : Starting range of shoulder ratio. Used for identifying shoulders, handles and necklines

shoulderEnd (float) : Ending range of shoulder ratio. Used for identifying shoulders, handles and necklines

Returns: int pattern type

method createPattern(zigzag, patternType, patternColor, riskAdjustment)

Create Pattern from ZigzagTypes.Zigzag object

Namespace types: zg.Zigzag

Parameters:

zigzag (Zigzag type from HeWhoMustNotBeNamed/ZigzagTypes/2) : ZigzagTypes.Zigzag object having array of zigzag pivots and other information on each pivots

patternType (int) : Type of pattern being created. 1 - Double Tap, 2 - Triple Tap, 3 - Cup and Handle, 4 - Head and Shoulders

patternColor (color) : Color in which the patterns are drawn

riskAdjustment (float) : Used for calculating stops

Returns: ReversalChartPattern object created

method getName(this)

get pattern name of ReversalChartPattern object

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: string name of the pattern

method getDescription(this)

get consolidated description of ReversalChartPattern object

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: string consolidated description

method init(this)

initializes the ReversalChartPattern object and creates sub object types

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: ReversalChartPattern current object

ReversalChartPatternDrawing

Type which holds the drawing objects for Reversal Chart Pattern Types

Fields:

patternLines (Line type from HeWhoMustNotBeNamed/DrawingTypes/1) : array of Line objects representing pattern

entry (Line type from HeWhoMustNotBeNamed/DrawingTypes/1) : Entry price Line

target (Line type from HeWhoMustNotBeNamed/DrawingTypes/1) : Target price Line

patternLabel (Label type from HeWhoMustNotBeNamed/DrawingTypes/1)

ReversalChartPattern

Reversal Chart Pattern master type which holds the pattern components, drawings and trade details

Fields:

pivots (Pivot type from HeWhoMustNotBeNamed/ZigzagTypes/2) : Array of Zigzag Pivots forming the pattern

patternType (series int) : Defines the main type of pattern 1 - Double Tap, 1 - Triple Tap, 3 - Cup and Handle, 4 - Head and Shoulders

patternColor (series color) : Color in which the pattern will be drawn on chart

riskAdjustment (series float) : Percentage adjustment of risk. Used for setting stops

drawing (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object which holds the drawing components

trade (Trade type from HeWhoMustNotBeNamed/TradeTracker/1) : TradeTracker.Trade object holding trade components

TradeTrackerLibrary "TradeTracker"

Simple Library for tracking trades

method track(this)

tracks trade when called on every bar

Namespace types: Trade

Parameters:

this (Trade) : Trade object

Returns: current Trade object

Trade

Has the constituents to track trades generated by any method.

Fields:

id (series int)

direction (series int) : Trade direction. Positive values for long and negative values for short trades

initialEntry (series float) : Initial entry price. This value will not change even if the entry is changed in the lifecycle of the trade

entry (series float) : Updated entry price. Allows variations to initial calculated entry. Useful in cases of trailing entry.

initialStop (series float) : Initial stop. Similar to initial entry, this is the first calculated stop for the lifecycle of trade.

stop (series float) : Trailing Stop. If there is no trailing, the value will be same as that of initial trade

targets (float ) : array of target values.

startBar (series int) : bar index of starting bar. Set by default when object is created. No need to alter this after that.

endBar (series int) : bar index of last bar in trade. Set by tracker on each execution

startTime (series int) : time of the start bar. Set by default when object is created. No need to alter this after that.

endTime (series int) : time of the ending bar. Updated by tracking method.

status (series int) : Integer parameter to track the status of the trade

retest (series bool) : Boolean parameter to notify if there was retest of the entry price

MathEasingFunctionsLibrary "MathEasingFunctions"

A collection of Easing functions.

Easing functions are commonly used for smoothing actions over time, They are used to smooth out the sharp edges

of a function and make it more pleasing to the eye, like for example the motion of a object through time.

Easing functions can be used in a variety of applications, including animation, video games, and scientific

simulations. They are a powerful tool for creating realistic visual effects and can help to make your work more

engaging and enjoyable to the eye.

---

Includes functions for ease in, ease out, and, ease in and out, for the following constructs:

sine, quadratic, cubic, quartic, quintic, exponential, elastic, circle, back, bounce.

---

Reference:

easings.net

learn.microsoft.com

ease_in_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

select(v, formula, effect, bounded)

Parameters:

v (float)

formula (string)

effect (string)

bounded (bool)

SAT_BACKTEST @description TODO: Regroupement of useful functionsLibrary "SAT_BACKTEST"

ex_timezone(tz)

switch case return exact @timezone for timezone input

Parameters:

tz (simple string)

Returns: syminfo.timezone or tz

if_in_date_range(usefromDate, fromDate, usetoDate, toDate, src_timezone, dst_timezone)

if_in_date_range : check if @time_close is range

Parameters:

usefromDate (simple bool)

fromDate (simple int)

usetoDate (simple bool)

toDate (simple int)

src_timezone (simple string)

dst_timezone (simple string)

Returns: true if @time_close is range

if_in_session(useSessionStart, sessionStartHour, sessionStartMinute, useSessionEnd, sessionEndHour, sessionEndMinute, useSessionDay, mon, tue, wed, thu, fri, sat, sun, src_timezone, dst_timezone)

if_in_session : check if @time_close is range

Parameters:

useSessionStart (simple bool)

sessionStartHour (simple int)

sessionStartMinute (simple int)

useSessionEnd (simple bool)

sessionEndHour (simple int)

sessionEndMinute (simple int)

useSessionDay (simple bool)

mon (simple bool)

tue (simple bool)

wed (simple bool)

thu (simple bool)

fri (simple bool)

sat (simple bool)

sun (simple bool)

src_timezone (simple string)

dst_timezone (simple string)

Returns: true if @time_close is range

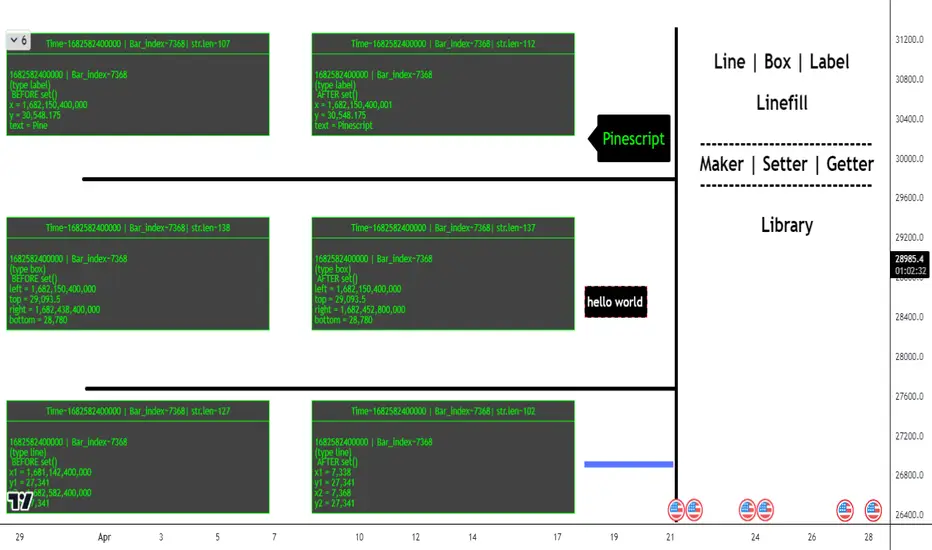

ObjectHelpersLibrary "ObjectHelpers"

Line | Box | Label | Linefill -- Maker, Setter, Getter Library

TODO: add table functionality

set(object)

set all params for `line`, `box`, `label`, `linefill` objects with 1 function

***

## Overloaded

***

```

method set(line Line, int x1=na, float y1=na, int x2=na, float y2=na,string xloc=na,string extend=na,color color=na,string style=na,int width=na,bool update=na) => line

```

### Params

- **Line** `line` - line object | `required`

- **x1** `int` - value to set x1

- **y1** `float` - value to set y1

- **x2** `int` - value to set x2

- **y2** `float` - value to set y2

- **xloc** `int` - value to set xloc

- **yloc** `int` - value to set yloc

- **extend** `string` - value to set extend

- **color** `color` - value to set color

- **style** `string` - value to set style

- **width** `int` - value to set width

- **update** `bool` - value to set update

***

```

method set(box Box,int left=na,float top=na,int right=na, float bottom=na,color bgcolor=na,color border_color=na,string border_style=na,int border_width=na,string extend=na,string txt=na,color text_color=na,string text_font_family=na,string text_halign=na,string text_valign=na,string text_wrap=na,bool update=false) => box

```

### Params

- **Box** `box` - box object

- **left** `int` - value to set left

- **top** `float` - value to set top

- **right** `int` - value to set right

- **bottom** `float` - value to set bottom

- **bgcolor** `color` - value to set bgcolor

- **border_color** `color` - value to set border_color

- **border_style** `string` - value to set border_style

- **border_width** `int` - value to set border_width

- **extend** `string` - value to set extend

- **txt** `string` - value to set _text

- **text_color** `color` - value to set text_color

- **text_font_family** `string` - value to set text_font_family

- **text_halign** `string` - value to set text_halign

- **text_valign** `string` - value to set text_valign

- **text_wrap** `string` - value to set text_wrap

- **update** `bool` - value to set update

***

```

method set(label Label,int x=na,float y=na, string txt=na,string xloc=na,color color=na,color textcolor=na,string size=na,string style=na,string textalign=na,string tooltip=na,string text_font_family=na,bool update=false) => label

```

### Paramas

- **Label** `label` - label object

- **x** `int` - value to set x

- **y** `float` - value to set y

- **txt** `string` - value to set text add`"+++"` to the _text striing to have the current label text concatenated to the location of the "+++")

- **textcolor** `color` - value to set textcolor

- **size** `string` - value to set size

- **style** `string` - value to set style (use "flip" ,as the style to have label flip to top or bottom of bar depending on if open > close and vice versa)

- **text_font_family** `string` - value to set text_font_family

- **textalign** `string` - value to set textalign

- **tooltip** `string` - value to set tooltip

- **update** `bool` - update label to next bar

***

```

method set(linefill Linefill=na,line line1=na,line line2=na,color color=na) => linefill

```

### Params

- **linefill** `linefill` - linefill object

- **line1** `line` - line object

- **line2** `line` - line object

- **color** `color` - color

Parameters:

object (obj)

Returns: `line`, `box`, `label`, `linefill`

method set(Line, x1, y1, x2, y2, xloc, extend, color, style, width, update)

set the location params of a line with 1 function auto detects time or bar_index for xloc param

Namespace types: series line

Parameters:

Line (line) : `line` - line object | `required`

x1 (int) : `int` - value to set x1

y1 (float) : `float` - value to set y1

x2 (int) : `int` - value to set x2

y2 (float) : `float` - value to set y2

xloc (string) : `int` - value to set xloc

extend (string) : `string` - value to set extend

color (color) : `color` - value to set color

style (string) : `string` - value to set style

width (int) : `int` - value to set width

update (bool) : `bool` - value to set update

Returns: `line`

method set(Box, left, top, right, bottom, bgcolor, border_color, border_style, border_width, extend, txt, text_color, text_font_family, text_halign, text_valign, text_wrap, update)

set the location params of a box with 1 function

Namespace types: series box

Parameters:

Box (box) : `box` - box object | `required`

left (int) : `int` - value to set left

top (float) : `float` - value to set top

right (int) : `int` - value to set right

bottom (float) : `float` - value to set bottom

bgcolor (color) : `color` - value to set bgcolor

border_color (color) : `color` - value to set border_color

border_style (string) : `string` - value to set border_style

border_width (int) : `int` - value to set border_width

extend (string) : `string` - value to set extend

txt (string) : `string` - value to set _text

text_color (color) : `color` - value to set text_color

text_font_family (string) : `string` - value to set text_font_family

text_halign (string) : `string` - value to set text_halign

text_valign (string) : `string` - value to set text_valign

text_wrap (string) : `string` - value to set text_wrap

update (bool) : `bool` - value to set update

Returns: `box`

method set(Label, x, y, txt, xloc, color, textcolor, size, style, textalign, tooltip, text_font_family, update)

set the location params of a label with 1 function auto detects time or bar_index for xloc param

Namespace types: series label

Parameters:

Label (label) : `label` | `required`

x (int) : `int` - value to set x

y (float) : `float` - value to set y

txt (string) : `string` - value to set text add`"+++"` to the _text striing to have the current label text concatenated to the location of the "+++")

xloc (string)

color (color)

textcolor (color) : `color` - value to set textcolor

size (string) : `string` - value to set size

style (string) : `string` - value to set style (use "flip" ,as the style to have label flip to top or bottom of bar depending on if open > close and vice versa)

textalign (string) : `string` - value to set textalign

tooltip (string) : `string` - value to set tooltip

text_font_family (string) : `string` - value to set text_font_family

update (bool) : `bool` - update label to next bar

Returns: `label`

method set(Linefill, line1, line2, color)

change the 1 or 2 of the lines in a linefill object

Namespace types: series linefill

Parameters:

Linefill (linefill)

line1 (line) : `line` - line object

line2 (line) : `line` - line object

color (color) : `color` - color

Returns: `linefill`

get(object)

get all of the location variables for `line`, `box`, `label` objects or the line objects from a `linefill`

***

## Overloaded

***

```

method get(line Line) =>

```

### Params

- **Line** `line` - line object | `required`

***

```

method get(box Box) =>

```

### Params

- **Box** `box` - box object | `required`

***

```

method get(label Label) =>

```

### Paramas

- **Label** `label` - label object | `required`

***

```

method get(linefill Linefill) =>

```

### Params

- **Linefill** `linefill` - linefill object | `required`

Parameters:

object (obj)

Returns: ` `

method get(Line)

Gets the location paramaters of a Line

Namespace types: series line

Parameters:

Line (line) : `line` - line object

Returns:

method get(Box)

Gets the location paramaters of a Box

Namespace types: series box

Parameters:

Box (box) : `box` - box object

Returns:

method get(Label)

Gets the `x`, `y`, `text` of a Label

Namespace types: series label

Parameters:

Label (label) : `label` - label object

Returns:

method get(Linefill)

Gets `line 1`, `line 2` from a Linefill

Namespace types: series linefill

Parameters:

Linefill (linefill) : `linefill` - linefill object

Returns:

method set_x(Line, x1, x2)

set the `x1`, `x2` of a line

***

### Params

- **Line** `line` - line object | `required`

- **x1** `int` - value to set x1 | `required`

- **x2** `int` - value to set x2 | `required`

Namespace types: series line

Parameters:

Line (line) : `line` - line object

x1 (int) : `int` - value to set x1

x2 (int) : `int` - value to set x2

Returns: `line`

method set_y(Line, y1, y2)

set `y1`, `y2` of a line

***

### Params

- **Line** `line` - line object | `required`

- **y1** `float` - value to set y1 | `required`

- **y2** `float` - value to set y2 | `required`

Namespace types: series line

Parameters:

Line (line) : `line` - line object

y1 (float) : `float` - value to set y1

y2 (float) : `float` - value to set y2

Returns: `line`

method Line(x1, y1, x2, y2, extend, color, style, width)

Similar to `line.new()` but can detect time or bar_index for xloc param and has defaults for all params but `x1`, `y1`, `x2`, `y2`

***

### Params

- **x1** `int` - value to set

- **y1** `float` - value to set

- **x2** `int` - value to set

- **y2** `float` - value to set

- **extend** `string` - extend value to set line

- **color** `color` - color to set line

- **style** `string` - style to set line

- **width** `int` - width to set line

Namespace types: series int, simple int, input int, const int

Parameters:

x1 (int) : `int` - value to set

y1 (float) : `float` - value to set

x2 (int) : `int` - value to set

y2 (float) : `float` - value to set

extend (string) : `string` - extend value to set line

color (color) : `color` - color to set line

style (string) : `string` - style to set line

width (int) : `int` - width to set line

Returns: `line`

method Box(left, top, right, bottom, extend, border_color, bgcolor, text_color, border_width, border_style, txt, text_halign, text_valign, text_size, text_wrap)

similar to box.new() with the but can detect xloc param and has defaults for everything but location params

***

### Params

- **left** `int` - value to set

- **top** `float` - value to set

- **right** `int` - value to set

- **bottom** `float` - value to set

- **extend** `string` - extend value to set box

- **border_color** `color` - color to set border

- **bgcolor** `color` - color to set background

- **text_color** `color` - color to set text

- **border_width** `int` - width to set border

- **border_style** `string` - style to set border

- **txt** `string` - text to set

- **text_halign** `string` - horizontal alignment to set text

- **text_valign** `string` - vertical alignment to set text

- **text_size** `string` - size to set text

- **text_wrap** `string` - wrap to set text

Namespace types: series int, simple int, input int, const int

Parameters:

left (int) : `int` - value to set

top (float) : `float` - value to set

right (int) : `int` - value to set

bottom (float) : `float` - value to set

extend (string) : `string` - extend value to set box

border_color (color) : `color` - color to set border

bgcolor (color) : `color` - color to set background

text_color (color) : `color` - color to set text

border_width (int) : `int` - width to set border

border_style (string) : `string` - style to set border

txt (string) : `string` - text to set

text_halign (string) : `string` - horizontal alignment to set text

text_valign (string) : `string` - vertical alignment to set text

text_size (string) : `string` - size to set text

text_wrap (string) : `string` - wrap to set text

Returns: `box`

method Label(txt, x, y, yloc, color, textcolor, style, size, textalign, text_font_family, tooltip)

Similar to label.new() but can detect time or bar_index for xloc param and has defaults for all params but x, y, txt, tooltip

***

### Params

- **txt** `string` - string to set

- **x** `int` - value to set

- **y** `float` - value to set

- **yloc** `string` - y location to set

- **color** `color` - label color to set

- **textcolor** `color` - text color to set

- **style** `string` - style to set

- **size** `string` - size to set

- **textalign** `string` - text alignment to set

- **text_font_family** `string` - font family to set

- **tooltip** `string` - tooltip to set

Namespace types: series string, simple string, input string, const string

Parameters:

txt (string) : `string` - string to set

x (int) : `int` - value to set

y (float) : `float` - value to set

yloc (string) : `string` - y location to set

color (color) : `color` - label color to set

textcolor (color) : `color` - text color to set

style (string) : `string` - style to set

size (string) : `string` - size to set

textalign (string) : `string` - text alignment to set

text_font_family (string) : `string` - font family to set

tooltip (string) : `string` - tooltip to set

Returns: `label`

obj

Fields:

obj (series__string)

peacefulIndicatorsWe are delighted to present the PeacefulIndicators library, a modest yet powerful collection of custom technical indicators created to enhance your trading analysis. The library features an array of practical tools, including MACD with Dynamic Length, Stochastic RSI with ATR Stop Loss, Bollinger Bands with RSI Divergence, and more.

The PeacefulIndicators library offers the following functions:

macdDynamicLength: An adaptive version of the classic MACD indicator, which adjusts the lengths of the moving averages based on the dominant cycle period, providing a more responsive signal.

rsiDivergence: A unique implementation of RSI Divergence detection that identifies potential bullish and bearish divergences using a combination of RSI and linear regression.

trendReversalDetection: A helpful tool for detecting trend reversals using the Rate of Change (ROC) and Moving Averages, offering valuable insights into possible market shifts.

volume_flow_oscillator: A custom oscillator that combines price movement strength and volume to provide a unique perspective on market dynamics.

weighted_volatility_oscillator: Another custom oscillator that factors in price volatility and volume to deliver a comprehensive view of market fluctuations.

rvo: The Relative Volume Oscillator highlights changes in volume relative to historical averages, helping to identify potential breakouts or reversals.

acb: The Adaptive Channel Breakout indicator combines a moving average with an adjustable volatility multiplier to create dynamic channels, useful for identifying potential trend shifts.

We hope this library proves to be a valuable addition to your trading toolbox.

Library "peacefulIndicators"

A custom library of technical indicators for trading analysis, including MACD with Dynamic Length, Stochastic RSI with ATR Stop Loss, Bollinger Bands with RSI Divergence, and more.

macdDynamicLength(src, shortLen, longLen, signalLen, dynLow, dynHigh)

Moving Average Convergence Divergence with Dynamic Length

Parameters:

src (float) : Series to use

shortLen (int) : Shorter moving average length

longLen (int) : Longer moving average length

signalLen (int) : Signal line length

dynLow (int) : Lower bound for the dynamic length

dynHigh (int) : Upper bound for the dynamic length

Returns: tuple of MACD line and Signal line

Computes MACD using lengths adapted based on the dominant cycle period

rsiDivergence(src, rsiLen, divThreshold, linRegLength)

RSI Divergence Detection

Parameters:

src (float) : Series to use

rsiLen (simple int) : Length for RSI calculation

divThreshold (float) : Divergence threshold for RSI

linRegLength (int) : Length for linear regression calculation

Returns: tuple of RSI Divergence (positive, negative)

Computes RSI Divergence detection that identifies bullish (positive) and bearish (negative) divergences

trendReversalDetection(src, rocLength, maLength, maType)

Trend Reversal Detection (TRD)

Parameters:

src (float) : Series to use

rocLength (int) : Length for Rate of Change calculation

maLength (int) : Length for Moving Average calculation

maType (string) : Type of Moving Average to use (default: "sma")

Returns: A tuple containing trend reversal direction and the reversal point

Detects trend reversals using the Rate of Change (ROC) and Moving Averages.

volume_flow_oscillator(src, length)

Volume Flow Oscillator

Parameters:

src (float) : Series to use

length (int) : Period for the calculation

Returns: Custom Oscillator value

Computes the custom oscillator based on price movement strength and volume

weighted_volatility_oscillator(src, length)

Weighted Volatility Oscillator

Parameters:

src (float) : Series to use

length (int) : Period for the calculation

Returns: Custom Oscillator value

Computes the custom oscillator based on price volatility and volume

rvo(length)

Relative Volume Oscillator

Parameters:

length (int) : Period for the calculation

Returns: Custom Oscillator value

Computes the custom oscillator based on relative volume

acb(price_series, ma_length, vol_length, multiplier)

Adaptive Channel Breakout

Parameters:

price_series (float) : Price series to use

ma_length (int) : Period for the moving average calculation

vol_length (int) : Period for the volatility calculation

multiplier (float) : Multiplier for the volatility

Returns: Tuple containing the ACB upper and lower values and the trend direction (1 for uptrend, -1 for downtrend)

Antares_messages_publicLibrary "Antares_messages_public"

This library add messages for yours strategy for use in Antares trading system for binance and bybit exchanges.

Данная библиотека позволяет формировать сообщения в алертах стратегий для Antares в более упрощенном для пользователя режиме, включая всплывающие подсказки и т.д.

set_leverage(token, market, ticker_id, leverage)

Set leverage for ticker on specified market.

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

leverage (float) : (float) leverage level. Устанавливаемое плечо.

Returns: 'Set leverage message'.

pause(time_pause)

Set pause in message. '::' -left and '::' -right included.

Parameters:

time_pause (int)

LongLimit(token, market, ticker_id, type_qty, quantity, price, orderId, leverageforqty)

Buy order with limit price and quantity.

Лимитный ордер на покупку(в лонг).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Limit Buy order'. Лимитный ордер на покупку (лонг).

LongMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Market Buy order with quantity.

Рыночный ордер на покупку (в лонг).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Buy order'. Маркетный ордер на покупку (лонг).

ShortLimit(token, market, ticker_id, type_qty, quantity, price, leverageforqty, orderId)

Sell order with limit price and quantity.

Лимитный ордер на продажу(в шорт).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

Returns: 'Limit Sell order'. Лимитный ордер на продажу (шорт).

ShortMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Sell by market price and quantity.

Рыночный ордер на продажу(в шорт).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Sell order'. Маркетный ордер на продажу (шорт).

Cancel_by_ticker(token, market, ticker_id)

Cancel all orders for market and ticker in setups. Отменяет все ордера на заданной бирже и заданном токене(паре).

Parameters:

token (string)

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

Returns: 'Cancel all orders'. Отмена всех ордеров на заданной бирже и заданном токене(паре).

Cancel_by_id(token, market, ticker_id, orderId)

Cancel order by Id for market and ticker in setups. Отменяет ордер по Id на заданной бирже и заданном токене(паре).

Parameters:

token (string)

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

orderId (string)

Returns: 'Cancel order'. Отмена ордера по Id на заданной бирже и заданном токене(паре).

Close_positions(token, market, ticker_id)

Close all positions for market and ticker in setups. Закрывает все позиции на заданной бирже и заданном токене(паре).

Parameters:

token (string)

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

Returns: 'Close positions'

CloseLongLimit(token, market, ticker_id, type_qty, quantity, price, orderId, leverageforqty)

Close limit order for long position. (futures)

Лимитный ордер на продажу(в шорт) для закрытия лонговой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Limit Sell order reduce only (close long position)'. Лимитный ордер на продажу для снижения текущего лонга(в шорт не входит).

CloseLongMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Close market order for long position.

Рыночный ордер на продажу(в шорт) для закрытия лонговой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Sell order reduce only (close long position)'. Ордер на снижение/закрытие текущего лонга(в шорт не входит) по рыночной цене.

CloseShortLimit(token, market, ticker_id, type_qty, quantity, price, orderId, leverageforqty)

Close limit order for short position.

Лимитный ордер на покупку(в лонг) для закрытия шортовой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Limit Buy order reduce only (close short position)' . Лимитный ордер на покупку (лонг) для сокращения/закрытия текущего шорта.

CloseShortMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Set Close limit order for long position.

Рыночный ордер на покупку(в лонг) для сокращения/закрытия шортовой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Buy order reduce only (close short position)'. Маркетного ордера на покупку (лонг) для сокращения/закрытия текущего шорта.

cancel_all_close(token, market, ticker_id)

Parameters:

token (string)

market (string)

ticker_id (string)

limit_tpsl_bybitfu(token, ticker_id, order_id, side, type_qty, quantity, price, tp_price, sl_price, leverageforqty)

Set multi order for Bybit : limit + takeprofit + stoploss

Выставление тройного ордера на Bybit лимитка со стоплоссом и тейкпрофитом

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

order_id (string)

side (bool) : (bool) "buy side" if true or "sell side" if false. true для лонга, false для шорта.

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order by 'side'. Цена лимитного ордера

tp_price (float) : (float) price for take profit order.

sl_price (float) : (float) price for stoploss order

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: Set multi order for Bybit : limit + takeprofit + stoploss.

replace_limit_tpsl_bybitfu(token, ticker_id, order_id, side, type_qty, quantity, price, tp_price, sl_price, leverageforqty)

Change multi order for Bybit : limit + takeprofit + stoploss

Изменение тройного ордера на Bybit лимитка со стоплоссом и тейкпрофитом

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

order_id (string)

side (bool) : (bool) "buy side" if true or "sell side" if false. true для лонга, false для шорта.

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order by 'side'. Цена лимитного ордера

tp_price (float) : (float) price for take profit order.

sl_price (float) : (float) price for stoploss order

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: Set multi order for Bybit : limit + takeprofit + stoploss.

long_stop(token, market, ticker_id, type_qty, quantity, l_stop, leverageforqty)

Stop market order for long position

Рыночный стоп-ордер на продажу для закрытия лонговой позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

l_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Stop Market Sell order (close long position)'. Маркетный стоп-ордер на снижения/закрытия текущего лонга.

short_stop(token, market, ticker_id, type_qty, quantity, s_stop, leverageforqty)

Stop market order for short position

Рыночный стоп-ордер на покупку(в лонг) для закрытия шорт позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

s_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Stop Market Buy order (close short position)'. Маркетный стоп-ордер на снижения/закрытия текущего шорта.

change_stop_l(token, market, ticker_id, type_qty, quantity, l_stop, leverageforqty)

Change Stop market order for long position

Изменяем стоп-ордер на продажу(в шорт) для закрытия лонг позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

l_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Change Stop Market Buy order (close long position)'. Смещает цену активации Маркетного стоп-ордер на снижения/закрытия текущего лонга.

change_stop_s(token, market, ticker_id, type_qty, quantity, s_stop, leverageforqty)

Change Stop market order for short position

Смещает цену активации Рыночного стоп-ордера на покупку(в лонг) для закрытия шорт позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string)

quantity (float) : (float) orders size. Размер ордера.

s_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Change Stop Market Buy order (close short position)'. Смещает цену активации Маркетного стоп-ордер на снижения/закрытия текущего шорта.

open_long_position(token, market, ticker_id, type_qty, quantity, l_stop, leverageforqty)

Cancel and close all orders and positions by ticker , then open Long position by market price with stop order

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает лонг по маркету с выставлением стопа (переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

l_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'command_all_close + LongMarket + long_stop.

open_short_position(token, market, ticker_id, type_qty, quantity, s_stop, leverageforqty)

Cancel and close all orders and positions , then open Short position by market price with stop order

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает шорт по маркету с выставлением стопа(переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

s_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'command_all_close + ShortMarket + short_stop'.

open_long_trade(token, market, ticker_id, type_qty, quantity, l_stop, qty_ex1, price_ex1, qty_ex2, price_ex2, qty_ex3, price_ex3, leverageforqty)

Cancell and close all orders and positions , then open Long position by market price with stop order and take 1 ,take 2, take 3

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает лонг по маркету с выставлением стопа и 3 тейками (переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) enter order size, see at type_qty. Размер ордера входа, согласно type_qty.

l_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

qty_ex1 (float) : (float). Quantity for 1th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 1го тейка, согласно type_qty.. Если 0, то строка для этого тейка не формируется

price_ex1 (float) : (float). Price for 1th take , if = 0 string for order dont set. Цена лимитного ордера для 1го тейка. Если 0, то строка для этого тейка не формируется

qty_ex2 (float) : (float). Quantity for 2th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex2 (float) : (float). Price for 2th take, if = 0 string for order dont set. Цена лимитного ордера для 2го тейка. Если 0, то строка для этого тейка не формируется

qty_ex3 (float) : (float). Quantity for 3th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex3 (float) : (float). Price for 3th take, if = 0 string for order dont set. Цена лимитного ордера для 3го тейка. Если 0, то строка для этого тейка не формируется

leverageforqty (int)

Returns: 'cancel_all_close + LongMarket + long_stop + CloseLongLimit1 + CloseLongLimit2+CloseLongLimit3'.

open_short_trade(token, market, ticker_id, type_qty, quantity, s_stop, qty_ex1, price_ex1, qty_ex2, price_ex2, qty_ex3, price_ex3, leverageforqty)

Cancell and close all orders and positions , then open Short position by market price with stop order and take 1 and take 2

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает шорт по маркету с выставлением стопа и 3 тейками (переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string)

quantity (float)

s_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

qty_ex1 (float) : (float). Quantity for 1th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 1го тейка, согласно type_qty.. Если 0, то строка для этого тейка не формируется

price_ex1 (float) : (float). Price for 1th take , if = 0 string for order dont set. Цена лимитного ордера для 1го тейка. Если 0, то строка для этого тейка не формируется

qty_ex2 (float) : (float). Quantity for 2th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex2 (float) : (float). Price for 2th take, if = 0 string for order dont set. Цена лимитного ордера для 2го тейка. Если 0, то строка для этого тейка не формируется

qty_ex3 (float) : (float). Quantity for 3th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex3 (float) : (float). Price for 3th take, if = 0 string for order dont set. Цена лимитного ордера для 3го тейка. Если 0, то строка для этого тейка не формируется

leverageforqty (int)