ZLEMA FusionZLEMA Fusion - Advanced Zero-Lag Momentum & Trailing Stop System

A sophisticated overlay indicator combining the power of Zero Lag EMA (ZLEMA) with ATR-based Moving Stop (MOST) for precision trend following and dynamic support/resistance tracking.

Core Components:

1. ZLEMA (Zero Lag Exponential Moving Average)

Eliminates lag inherent in traditional EMAs

Provides faster response to price changes

Customizable length for different trading styles

Smooth, responsive trend line

2. MOST (Moving Stop - ATR Trailing Stop)

Dynamic ATR-based trailing stop system

Automatically adjusts to market volatility

Never moves backward - only trails in favourable direction

Green line = Uptrend support | Red line = Downtrend resistance

Customizable ATR multiplier and lookback period

Signal Generation:

BUY (⇑): When ZLEMA crosses above MOST

SELL (⇓): When ZLEMA crosses below MOST

Clean visual arrows with no label boxes

Signals trigger on candle close only (no repainting)

Advanced Features:

✅ Signal Cooldown System - Prevents signal spam with configurable minimum bars between signals

✅ ADX Trend Strength Filter - Optional filter to trade only in strong trends

✅ Higher Timeframe ZLEMA Confirmation - Multi-timeframe trend alignment for higher probability setups

✅ Background Color Coding - Quick visual trend identification (Green = Uptrend, Red = Downtrend)

✅ Alert System - Built-in alerts for buy and sell signals

Fully Customizable:

ZLEMA length

ATR period and multiplier

MOST lookback period

Signal cooldown bars

ADX filter threshold

Higher timeframe settings

Visual display options

Best Used For:

Index trading

Swing trading

Trend following strategies

Dynamic support/resistance identification

Entry/exit timing

Optimized for Indian Markets - Calibrated for Nifty, Bank Nifty, and other NSE instruments.

⚠️ Important Notes:

This indicator is for educational purposes

No repainting - all signals confirmed at candle close

Use proper risk management

Combine with your trading plan and additional confirmation

Norepaint

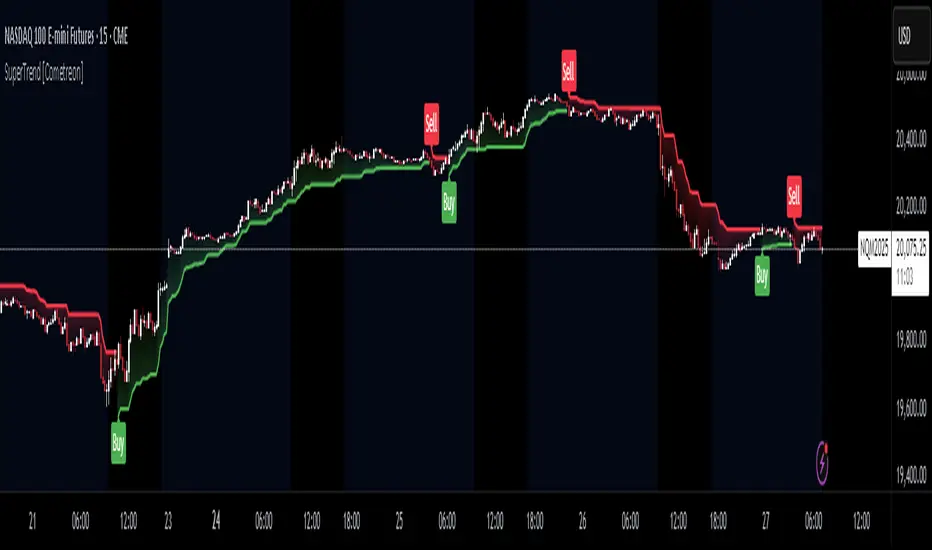

Trend Cloud with Buy/Sell Text [wjdtks255]Indicator Title: Trend Cloud with Buy/Sell Signal Pro

Short Description

A high-probability trend-following indicator based on Supertrend dynamics, enhanced with a Volume Filter to pinpoint explosive entries while minimizing false breakouts.

Detailed Description (Overview)

The Trend Cloud with Buy/Sell Text is designed for traders who prioritize clarity and momentum. It visualizes market trends through a "Trend Cloud" system and generates real-time BUY/SELL signals only when price action is backed by significant trading volume.

Key Technical Pillars

Dynamic Trend Cloud: Fills the area between the price and the Supertrend line, providing immediate visual feedback on trend strength and potential support/resistance zones.

Smart Volume Filter: A unique logic that compares current volume against a 20-period moving average. Labels only appear when a trend shift occurs with above-average volume, filtering out weak "fakeouts."

No-Repaint Labels: Signals are calculated and fixed at the close of the candle, ensuring that the BUY/SELL text remains permanent for reliable historical backtesting and live execution.

The Alpha Hunter Strategy (How to Trade)

1. Long Entry (Buy)

Condition: The cloud turns Aqua and a "BUY" label appears below the candle.

Confirmation: Ensure the price remains above the Aqua Trend Line.

Volume Check: The indicator automatically verifies if the volume is higher than the 20-period average before displaying the label.

Exit: Exit when a "SELL" signal appears or the price closes below the Aqua line.

2. Short Entry (Sell)

Condition: The cloud turns Red and a "SELL" label appears above the candle.

Confirmation: Price should stay below the Red Trend Line.

Exit: Exit when a "BUY" signal appears or the price closes above the Red line.

Input Parameters & Optimization

ATR Period (Default: 10): Determines the sensitivity to price volatility.

ATR Factor (Default: 3.0): Controls the distance of the trend line. Increase to 3.5 - 4.0 to reduce noise in choppy markets.

Volume Filter (Toggle): When enabled, only high-momentum signals are shown.

Recommended Usage

Best Timeframes: 15m, 1h, 4h.

Asset Classes: Highly effective for Crypto (BTC/ETH) and high-volume stocks.

Alpha Hunter Integrated MACD & Oscillator [wjdtks255]Indicator Title: Alpha Hunter Integrated MACD & Oscillator Pro

Short Description

A high-precision hybrid oscillator that integrates MACD dynamics with a secondary-smoothed histogram to eliminate market noise and capture trend reversals with minimal lag.

Detailed Description

Overview

The Alpha Hunter Integrated MACD & Oscillator is designed to overcome the inherent lag of standard MACD indicators. By applying an exponential moving average (EMA) filter to the histogram itself and incorporating a momentum direction check, this tool identifies high-probability entry points while filtering out "whipsaws" commonly found in choppy markets.

Key Technical Pillars

Dual-Smoothed Histogram: Unlike standard oscillators, this script smooths the raw histogram values using a secondary filtering period. This reveals the true underlying momentum before price action fully shifts.

Momentum Directional Filter: Entry signals are only triggered when the MACD line’s slope aligns with the crossover, ensuring you don't enter against a stalling trend.

Dynamic Trend Clouds: The visual fill between the MACD and Signal lines acts as a "Trend Cloud," providing immediate visual feedback on the strength and duration of the current trend.

The Winning Trading Strategy (How to Use)

To maximize win rates, it is highly recommended to use this indicator as a Confirmation Oscillator alongside a Long-term Trend Filter (like a 200 EMA) on your main chart.

1. Long Setup (Buy)

Context: Price must be trading above the 200 EMA on the main chart.

Signal: A green "BUY" triangle and label appear on the oscillator.

Confirmation: The Histogram should be green and rising.

Exit: Exit at a pre-defined Take Profit (TP) box or when a bearish MACD crossunder occurs.

2. Short Setup (Sell)

Context: Price must be trading below the 200 EMA on the main chart.

Signal: A red "SELL" triangle and label appear on the oscillator.

Confirmation: The Histogram should be red and falling.

Exit: Exit at the designated Stop Loss (SL) or when a bullish MACD crossover occurs.

Input Parameters & Optimization

Fast/Slow/Signal: Default 12, 26, 9. (Standard for most markets).

Signal Smoothing: Set to 5 for a balance of speed and reliability. Increase to 8+ for swing trading on higher timeframes.

Recommended Timeframes: 15m, 1h, and 4h for the best signal-to-noise ratio.

Author's Note

This indicator is a "No-Repaint" script. Signals are confirmed at the close of the candle to ensure reliability during live trading. Always use proper risk management.

Intuitive Predictive MACD TargetsThis indicator uses Reverse Engineering math to calculate the exact price the market needs to reach for specific MACD events to happen on the current bar.

Standard MACD is a lagging indicator—you usually wait for the candle to close to confirm a signal. This script changes that by drawing "Finish Lines" on your chart, showing you exactly where price must go right now to trigger a Crossover or a Momentum Hook.

The "Reverse Engineering" Concept

Instead of calculating MACD from Price, we calculate the Required Price from the Target MACD.

Q: "At what price will the MACD line cross the Signal line?"

A: The script solves this and draws the Green/Red "Crossover" Line.

Key Features

1. Three Distinct Targets

Crossover Target (PCO/NCO): The exact price needed to trigger a Buy/Sell signal on the current candle.

Dynamic Coloring: Turns Green if price needs to go UP to cross, Red if price needs to go DOWN.

Settlement Target (The Hook): The exact price where the MACD momentum flattens out (Angle = 0). If price touches this Orange Dashed Line, the trend is likely pausing or preparing to reverse.

Zero Cross Target: The price needed for MACD to reclaim the Zero Line.

2. Smart "Staggered" Labels (No Overlap)

Unlike other scripts where text piles up and becomes unreadable, this indicator automatically spreads labels horizontally.

Crossover info stays near the price.

Settlement info is shifted to the right.

Zero info is shifted further right.

Result: You can read all three targets clearly, even if the prices are almost identical.

3. Full Customization

Line Length: Choose "Infinite" to see targets as Support/Resistance levels across the screen, or "Short" to keep your chart background clean.

Text Visibility: Option to force text to White or Black for high contrast on Dark/Light themes.

Styles: Fully adjustable colors, line widths, and styles (Solid, Dashed, Dotted) for each target type.

How to Use

The "Finish Line" Strategy: If you are Long, and the Red NCO Line appears just below the current price, be cautious. It means a very small drop will confirm a Bearish Cross.

Momentum Checks: Watch the Orange "Settlement" Line.

If price is moving away from the Orange line, the trend is accelerating (Safe to hold).

If price touches the Orange line, momentum has died (Consider taking profit).

Settings

Visual Settings: Change Line Length (Infinite/Short) and Text Color.

MACD Settings: Standard inputs (Default 12, 26, 9).

Toggles: Option to show/hide the Zero Line target.

Double&Triple Pattern[TS_Indie]📌 Description – Double & Triple Pattern Indicator

The Double & Triple Pattern Indicator is developed to help traders systematically and clearly identify Double Top, Double Bottom, Triple Top, and Triple Bottom chart patterns.

⚙️ Core Logic & Working Mechanism

The Double & Triple Pattern Indicator is built on the concept of price swing formation, based on the logic of Trend Entry_0 , which focuses on structured market analysis and price action behavior.

The indicator detects three main swing points (Swing 1, Swing 2, and Swing 3). A Fibonacci Box is then created using Swing A and Swing B as reference points to define the swing detection zone.

When all three swings remain inside the defined Fibonacci Box, the structure is considered a valid Price Action setup.

The indicator then plots key lines on the chart:

➩ Break Line – used to confirm the signal (confirmation)

➩ Cancel Line – used to invalidate the price action if price moves against the conditions

➛ When price breaks the Break Line , the structure is confirmed and a Pending Order is placed at Swing B , with the Stop Loss set at Swing 1.

➛ If price breaks the Cancel Line first, the price action structure is immediately invalidated.

⚙️ Fibonacci Entry Zone & Change SL Settings

➩ When Fibo Entry Zone is set to 0, the Pending Order is placed directly at Swing B.

➩ When the value is greater than 0, the Pending Order is calculated using Fibonacci levels drawn from Swing B to the Stop Loss level.

➩ Change SL allows switching the Stop Loss reference between Swing 1 and Swing A.

⚙️ Min & Max Control for Swing Size : xATR

When enabling Control Size Swing : xATR , the indicator filters Swing B based on the defined Min and Max range.

This allows traders to selectively test larger or smaller swing-based price actions , depending on their trading strategy.

⭐ Pending Order Cancellation Conditions

A Pending Order will be canceled under the following conditions:

1.A new Price Action signal appears on either the Buy or Sell side.

2.When Time Session is enabled, the Pending Order is canceled once price exits the selected session.

🕹 Order Management Rule

When there is an active open position, the indicator restricts the creation of new Pending Orders to prevent overlapping positions.

💡 Double Pattern Example

💡 Triple Pattern Example

⚠️ Disclaimer

This indicator is designed for technical analysis purposes only and does not constitute investment advice.

Users should apply proper risk management and make decisions at their own discretion.

🥂 Community Sharing

If you find parameter settings that work well or produce strong statistical results, feel free to share them with the community so we can improve and develop this indicator together.

Moving Average Channel Breakout (No Repaint) This indicator creates a channel using two simple moving averages: SMA of highs (upper line) and SMA of lows (lower line).

How it works:

- When a candle closes above the upper channel line, the following candles turn green (bullish trend)

- When a candle closes below the lower channel line, the following candles turn red (bearish trend)

- The trend color remains until a breakout in the opposite direction occurs

Anti-repaint:

This indicator does NOT repaint. The candle color is determined at the open, based on the previous candle's close. Once a candle opens with a color, that color never changes.

Breakout strategy:

- Candle opens green → Long entry signal

- Candle opens red → Short entry signal

The signal and entry moment are perfectly synchronized at the candle open, making it ideal for systematic breakout strategies.

ParabolicSAR+EMA[TS_Indie]🚀 EMA + Parabolic SAR Reversal Trading Strategy

This trading system effectively combines the use of Exponential Moving Averages (EMA) with the Parabolic SAR to identify both price trends and key reversal points. The EMA Fast is used to signal the primary short-term trend, while the EMA Slow acts as a filter for the long-term trend direction. The Parabolic SAR then helps to confirm the reversal signals.

🛠️ Tools Used

1. EMA Fast – Primary Short-Term Trend

2. EMA Slow – Long-Term Trend Filter

3. Parabolic SAR – Reversal Confirmation

🎯 Entry Rules

📈 Buy Setup

1. Trend Filter: EMA Fast > EMA Slow → Uptrend

2. Pullback: Price pulls back and closes below the EMA Fast line.

3. Reversal: Price reverses/pulls back up and closes above the EMA Fast line.

4. SAR Confirmation: The previous Parabolic SAR dot is above the high, and the dot in the current candle is below the low → Reversal signal confirmed.

5. Entry: Enter Buy immediately.

📉 Sell Setup

1. Trend Filter: EMA Fast < EMA Slow → Downtrend

2. Pullback: Price pulls back and closes above the EMA Fast line.

3. Reversal: Price reverses/pulls back down and closes below the EMA Fast line.

4. SAR Confirmation: The previous Parabolic SAR dot is below the low, and the dot in the current candle is above the high → Reversal signal confirmed.

5. Entry: Enter Sell immediately.

💰 Exit Management (Entry, Stop Loss, Take Profit)

1. Entry: Enter the order at the closing price of the signal candle.

2. Stop Loss (SL): Set the Stop Loss at the Parabolic SAR dot.

3. Take Profit (TP): Calculated from the Entry and Stop Loss points, multiplied by the Risk Reward Ratio.

⚙️ Optional Parameters

➭ Custom Risk/Reward Ratio for Take Profit.

➭ Option to add an ATR buffer to the Stop Loss.

➭ Adjustable EMA Fast period.

➭ Adjustable EMA Slow period.

➭ Adjustable Parabolic SAR parameters.

➭ Option to enable Long-only / Short-only positions.

➭ Customizable Backtest start and end date.

➭ Customizable trading session time.

🔔 Alert Function

Alerts display:

➭ Entry Price

➭ Stop Loss Price

➭ Take Profit Price

💡 This strategy allows for many parameter adjustments, such as the MA type, adding/subtracting from the Stop Loss using ATR, and selecting specific sessions for backtesting. If you find interesting or profitable results after adjusting the parameters, please share your comments with other traders!

⚠️ Disclaimer

This indicator is designed for educational and research purposes only. It does not guarantee profits and should not be considered financial advice. Trading in financial markets involves significant risk , including the potential loss of capital.

Trend Entry_0 [TS_Indie]Trend Entry_0 — Mechanism Overview

The core structure of this strategy is based on a price action reversal pattern, as detailed below:

In the case of a Bullish Trend Reversal:

The price initially moves in a bearish direction. When candle A forms a low lower than the previous low, the high of candle A becomes a key reference point.

If the next candle closes above the high of candle A , it confirms a Bullish Trend Reversal.

* Upon a Bullish signal, a Long position is opened at the opening price of the next candle (candle B).

* When a subsequent Bearish signal occurs, the Long position is closed at the opening price of the next candle (candle C).

In the case of a Bearish Trend Reversal:

The price initially moves in a bullish direction. When candle A forms a high higher than the previous high, the low of candle A becomes a key reference point.

If the next candle closes below the low of candle A , it confirms a Bearish Trend Reversal.

* Upon a Bearish signal, a Short position is opened at the opening price of the next candle (candle B).

* When a subsequent Bullish signal occurs, the Short position is closed at the opening price of the next candle (candle C).

Options

* The start and end dates of the backtest can be customized.

* The swing lines of the trend can be displayed as an optional visual aid.

* The user can choose whether to open only Long or Short positions.

Backtest Results and Observations

Based on the backtesting results of this strategy across various assets and timeframes, it has been observed that this approach works best on trending assets such as Gold, BTC, and stocks.

It also performs well on higher timeframes, starting from the Daily timeframe and above, especially when taking Long positions only.

However, when applied to currency pairs such as EUR/USD, the results tend to be less impressive.

I encourage everyone to try backtesting and further developing this strategy — adding new conditions or filters may potentially lead to improved performance.

Disclaimer

This script is intended solely for backtesting purposes, based on a particular price action pattern.

It does not constitute financial or investment advice.

Backtest results do not guarantee future performance.

Institutional Composite Moving Average (ICMA) [Volume Vigilante]Institutional Composite Moving Average (ICMA)

The Next Evolution of Moving Averages — Built for Real Traders.

ICMA blends the strength of four powerful averages (SMA, EMA, WMA, HMA) into a single ultra-responsive, ultra-smooth signal.

It reacts faster than traditional MAs while filtering out noise, giving you clean trend direction with minimal lag.

🔹 Key Features:

• Faster reaction than SMA, EMA, or WMA individually

• Smoother and more stable than raw HMA

• Naturally adapts across trend, momentum, and consolidation conditions

• Zero gimmicks. Zero repainting. Full institutional quality.

🔹 Designed For:

• Scalping

• Swing trading

• Signal engines

• Algorithmic systems

📎 How to Use:

• Overlay it on any chart

• Fine-tune the length per timeframe

• Combine with your entries/exits for maximum edge

Created by Volume Vigilante 🧬 — Delivering Real-World Trading Tools.

SuperTrend MTF Pro [Cometreon]The SuperTrend MTF Pro takes the classic SuperTrend to a whole new level of customization and accuracy. Unlike the standard version, this indicator allows you to select different moving averages, apply it to various chart types, and fine-tune every key parameter.

If you're looking for an advanced, non-repainting, and highly configurable SuperTrend, this is the right choice for you.

🔷 New Features and Improvements

🟩 Multi-MA SuperTrend

Now you can customize the SuperTrend calculation by choosing from 15 different moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

🟩 Multiple Chart Types

You're no longer limited to candlestick charts! Now you can use SuperTrend with different chart formats, including:

Heikin Ashi

Renko

Kagi

Line Break

Point & Figure

🟩 Customizable Timeframe

Now you can adjust the SuperTrend timeframe without repainting issues, avoiding signal distortions.

🔷 Technical Details and Customizable Inputs

SuperTrend offers multiple customization options to fit any trading strategy:

1️⃣ ATR Period – Defines the ATR length, affecting the indicator’s sensitivity.

2️⃣ Source – Selects the price value used for calculations (Close, HL2, Open, etc.).

3️⃣ ATR Mult – Multiplies the ATR to determine band distance. Higher values reduce false signals, lower values make it more reactive.

4️⃣ Change ATR Calculation Method – When enabled, uses the default ATR method; when disabled, allows selecting another Moving Average with "Use Different Type".

5️⃣ Source Break – Defines the price source for trend changes (Close for more stability, High/Low for more reactivity).

6️⃣ Use Different Type – Allows selecting an alternative Moving Average for ATR calculation if "Change ATR Calculation Method" is disabled.

7️⃣ SuperTrend Type – Advanced options for specific MAs (JMA, ALMA, FRAMA, VIDYA), with dedicated parameters like Phase, Sigma, and Offset for optimized responsiveness.

8️⃣ Ticker Settings – Customize parameters for special chart types such as Renko, Heikin Ashi, Kagi, Line Break, and Point & Figure, adjusting reversal, number of lines, and ATR length.

9️⃣ Timeframe – Enables using SuperTrend on a higher timeframe.

🔟 Wait for Timeframe Closes -

✅ Enabled – Prevents multiple signals, useful for precise alerts.

❌ Disabled – Displays SuperTrend smoothly without interruptions.

🔷 How to Use SuperTrend MTF Pro

🔍 Identifying Trends

SuperTrend follows the ongoing trend and provides clear visual signals:

When the price is above the line, the trend is bullish.

When the price is below the line, the trend is bearish.

📈 Interpreting Signals

Line color and position change → Possible trend reversal

Bounce off the line → Potential trend continuation

Strong breakout of the line → Possible reversal

🛠 Integration with Other Tools

RSI or MACD to filter false signals

Moving Averages to confirm trend direction

Support and Resistance to improve entry points

☄️ If you find this indicator useful, leave a Boost to support its development!

Every feedback helps to continuously improve the tool, offering an even more effective trading experience. Share your thoughts in the comments! 🚀🔥

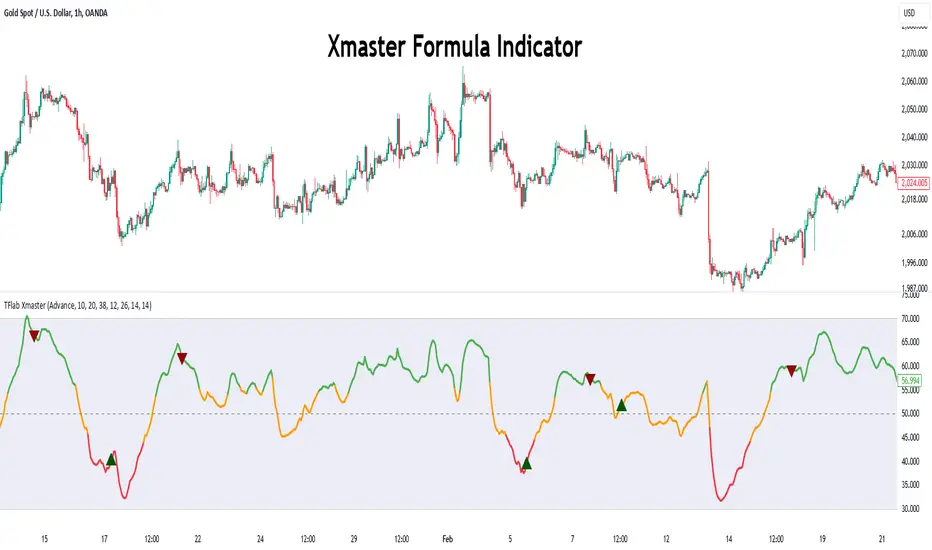

Xmaster Formula Indicator [TradingFinder] No Repaint Strategies🔵 Introduction

The Xmaster Formula Indicator is a powerful tool for forex trading, combining multiple technical indicators to provide insights into market trends, support and resistance levels, and price reversals. Developed in the early 2010s, it is widely valued for generating reliable buy and sell signals.

Key components include Exponential Moving Averages (EMA) for identifying trends and price momentum, and MACD (Moving Average Convergence Divergence) for analyzing trend strength and direction.

The Stochastic Oscillator and RSI (Relative Strength Index) enhance accuracy by signaling potential price reversals. Additionally, the Parabolic SAR assists in identifying trend reversals and managing risk.

By integrating these tools, the Xmaster Formula Indicator provides a comprehensive view of market conditions, empowering traders to make informed decisions.

🔵 How to Use

The Xmaster Formula Indicator offers two distinct methods for generating signals: Standard Mode and Advance Mode. Each method caters to different trading styles and strategies.

Standard Mode :

In Standard Mode, the indicator uses normalized moving average data to generate buy and sell signals. The difference between the short-term (10-period) and long-term (38-period) EMAs is calculated and normalized to a 0-100 scale.

Buy Signal : When the normalized value crosses above 55, accompanied by the trend line turning green, a buy signal is generated.

Sell Signal : When the normalized value crosses below 45, and the trend line turns red, a sell signal is issued.

This mode is simple, making it ideal for traders looking for straightforward signals without the need for additional confirmations.

Advance Mode :

Advance Mode combines multiple technical indicators to provide more detailed and robust signals.

This method analyzes trends by incorporating :

🟣 MACD

Buy Signal : When the MACD histogram bars are positive.

Sell Signal : When the MACD histogram bars are negative.

🟣 RSI

Buy Signal : When RSI is below 30, indicating oversold conditions.

Sell Signal : When RSI is above 70, suggesting overbought conditions.

🟣 Stochastic Oscillator

Buy Signal : When Stochastic is below 20.

Sell Signal : When Stochastic is above 80.

🟣 Parabolic SAR

Buy Signal : When SAR is below the price.

Sell Signal : When SAR is above the price.

A signal is generated in Advance Mode only when all these indicators align :

Buy Signal : All conditions point to a bullish trend.

Sell Signal : All conditions indicate a bearish trend.

This mode is more comprehensive and suitable for traders who prefer deeper analysis and stronger confirmations before executing trades.

🔵 Settings

Method :

Choose between "Standard" and "Advance" modes to determine how signals are generated. In Standard Mode, signals are based on normalized moving average data, while in Advance Mode, signals rely on the combination of MACD, RSI, Stochastic Oscillator, and Parabolic SAR.

Moving Average Settings :

Short Length : The period for the short-term EMA (default is 10).

Mid Length : The period for the medium-term EMA (default is 20).

Long Length : The period for the long-term EMA (default is 38).

MACD Settings :

Fast Length : The period for the fast EMA in the MACD calculation (default is 12).

Slow Length : The period for the slow EMA in the MACD calculation (default is 26).

Signal Line : The signal line period for MACD (default is 9).

Stochastic Settings :

Length : The period for the Stochastic Oscillator (default is 14).

RSI Settings :

Length : The period for the Relative Strength Index (default is 14).

🔵 Conclusion

The Xmaster Formula Indicator is a versatile and reliable tool for forex traders, offering both simplicity and advanced analysis through its Standard and Advance modes. In Standard Mode, traders benefit from straightforward signals based on normalized moving average data, making it ideal for quick decision-making.

Advance Mode, on the other hand, provides a more detailed analysis by combining multiple indicators like MACD, RSI, Stochastic Oscillator, and Parabolic SAR, delivering stronger confirmations for critical market decisions.

While the Xmaster Formula Indicator offers valuable insights and reliable signals, it is important to use it alongside proper risk management and other analytical methods. By leveraging its capabilities effectively, traders can enhance their trading strategies and achieve better outcomes in the dynamic forex market.

Leading T3Hello Fellas,

Here, I applied a special technique of John F. Ehlers to make lagging indicators leading. The T3 itself is usually not realling the classic lagging indicator, so it is not really needed, but I still publish this indicator to demonstrate this technique of Ehlers applied on a simple indicator.

The indicator does not repaint.

In the following picture you can see a comparison of normal T3 (purple) compared to a 2-bar "leading" T3 (gradient):

The range of the gradient is:

Bottom Value: the lowest slope of the last 100 bars -> green

Top Value: the highest slope of the last 100 bars -> purple

Ehlers Special Technique

John Ehlers did develop methods to make lagging indicators leading or predictive. One of these methods is the Predictive Moving Average, which he introduced in his book “Rocket Science for Traders”. The concept is to take a difference of a lagging line from the original function to produce a leading function.

The idea is to extend this concept to moving averages. If you take a 7-bar Weighted Moving Average (WMA) of prices, that average lags the prices by 2 bars. If you take a 7-bar WMA of the first average, this second average is delayed another 2 bars. If you take the difference between the two averages and add that difference to the first average, the result should be a smoothed line of the original price function with no lag.

T3

To compute the T3 moving average, it involves a triple smoothing process using exponential moving averages. Here's how it works:

Calculate the first exponential moving average (EMA1) of the price data over a specific period 'n.'

Calculate the second exponential moving average (EMA2) of EMA1 using the same period 'n.'

Calculate the third exponential moving average (EMA3) of EMA2 using the same period 'n.'

The formula for the T3 moving average is as follows:

T3 = 3 * (EMA1) - 3 * (EMA2) + (EMA3)

By applying this triple smoothing process, the T3 moving average is intended to offer reduced noise and improved responsiveness to price trends. It achieves this by incorporating multiple time frames of the exponential moving averages, resulting in a more accurate representation of the underlying price action.

Thanks for checking this out and give a boost, if you enjoyed the content.

Best regards,

simwai

---

Credits to @loxx

Adaptive Fisherized Z-scoreHello Fellas,

It's time for a new adaptive fisherized indicator of me, where I apply adaptive length and more on a classic indicator.

Today, I chose the Z-score, also called standard score, as indicator of interest.

Special Features

Advanced Smoothing: JMA, T3, Hann Window and Super Smoother

Adaptive Length Algorithms: In-Phase Quadrature, Homodyne Discriminator, Median and Hilbert Transform

Inverse Fisher Transform (IFT)

Signals: Enter Long, Enter Short, Exit Long and Exit Short

Bar Coloring: Presents the trade state as bar colors

Band Levels: Changes the band levels

Decision Making

When you create such a mod you need to think about which concepts are the best to conclude. I decided to take Inverse Fisher Transform instead of normalization to make a version which fits to a fixed scale to avoid the usual distortion created by normalization.

Moreover, I chose JMA, T3, Hann Window and Super Smoother, because JMA and T3 are the bleeding-edge MA's at the moment with the best balance of lag and responsiveness. Additionally, I chose Hann Window and Super Smoother because of their extraordinary smoothing capabilities and because Ehlers favours them.

Furthermore, I decided to choose the half length of the dominant cycle instead of the full dominant cycle to make the indicator more responsive which is very important for a signal emitter like Z-score. Signal emitters always need to be faster or have the same speed as the filters they are combined with.

Usage

The Z-score is a low timeframe scalper which works best during choppy/ranging phases. The direction you should trade is determined by the last trend change. E.g. when the last trend change was from bearish market to bullish market and you are now in a choppy/ranging phase confirmed by e.g. Chop Zone or KAMA slope you want to do long trades.

Interpretation

The Z-score indicator is a momentum indicator which shows the number of standard deviations by which the value of a raw score (price/source) is above or below the mean value of what is being observed or measured. Easily explained, it is almost the same as Bollinger Bands with another visual representation form.

Signals

B -> Buy -> Z-score crosses above lower band

S -> Short -> Z-score crosses below upper band

BE -> Buy Exit -> Z-score crosses above 0

SE -> Sell Exit -> Z-score crosses below 0

If you were reading till here, thank you already. Now, follows a bunch of knowledge for people who don't know the concepts I talk about.

T3

The T3 moving average, short for "Tim Tillson's Triple Exponential Moving Average," is a technical indicator used in financial markets and technical analysis to smooth out price data over a specific period. It was developed by Tim Tillson, a software project manager at Hewlett-Packard, with expertise in Mathematics and Computer Science.

The T3 moving average is an enhancement of the traditional Exponential Moving Average (EMA) and aims to overcome some of its limitations. The primary goal of the T3 moving average is to provide a smoother representation of price trends while minimizing lag compared to other moving averages like Simple Moving Average (SMA), Weighted Moving Average (WMA), or EMA.

To compute the T3 moving average, it involves a triple smoothing process using exponential moving averages. Here's how it works:

Calculate the first exponential moving average (EMA1) of the price data over a specific period 'n.'

Calculate the second exponential moving average (EMA2) of EMA1 using the same period 'n.'

Calculate the third exponential moving average (EMA3) of EMA2 using the same period 'n.'

The formula for the T3 moving average is as follows:

T3 = 3 * (EMA1) - 3 * (EMA2) + (EMA3)

By applying this triple smoothing process, the T3 moving average is intended to offer reduced noise and improved responsiveness to price trends. It achieves this by incorporating multiple time frames of the exponential moving averages, resulting in a more accurate representation of the underlying price action.

JMA

The Jurik Moving Average (JMA) is a technical indicator used in trading to predict price direction. Developed by Mark Jurik, it’s a type of weighted moving average that gives more weight to recent market data rather than past historical data.

JMA is known for its superior noise elimination. It’s a causal, nonlinear, and adaptive filter, meaning it responds to changes in price action without introducing unnecessary lag. This makes JMA a world-class moving average that tracks and smooths price charts or any market-related time series with surprising agility.

In comparison to other moving averages, such as the Exponential Moving Average (EMA), JMA is known to track fast price movement more accurately. This allows traders to apply their strategies to a more accurate picture of price action.

Inverse Fisher Transform

The Inverse Fisher Transform is a transform used in DSP to alter the Probability Distribution Function (PDF) of a signal or in our case of indicators.

The result of using the Inverse Fisher Transform is that the output has a very high probability of being either +1 or –1. This bipolar probability distribution makes the Inverse Fisher Transform ideal for generating an indicator that provides clear buy and sell signals.

Hann Window

The Hann function (aka Hann Window) is named after the Austrian meteorologist Julius von Hann. It is a window function used to perform Hann smoothing.

Super Smoother

The Super Smoother uses a special mathematical process for the smoothing of data points.

The Super Smoother is a technical analysis indicator designed to be smoother and with less lag than a traditional moving average.

Adaptive Length

Length based on the dominant cycle length measured by a "dominant cycle measurement" algorithm.

Happy Trading!

Best regards,

simwai

---

Credits to

@cheatcountry

@everget

@loxx

@DasanC

@blackcat1402

Ehlers Combo Strategy🚀 Presenting the Enhanced Ehlers Combo Strategy 🚀

Hello Traders! 👋 I'm thrilled to share the latest version of the Ehlers Combo Strategy v2.0. This powerful algorithm combines Ehlers Elegant Oscillator, Decycler, Instantaneous Trendline, Spearman Rank, and introduces the Signal to Noise Ratio for even more precise trading signals.

📊 Strategy Highlights:

Ehlers Elegant Oscillator: Captures market momentum and turning points.

Ehlers Decycler: Filters out market noise for clearer trend signals.

Instantaneous Trendline: Offers a dynamic view of the market trend.

Spearman Rank: Analyzes market rank correlations for enhanced insights.

Signal to Noise Ratio (SNR): Filters out noise for more accurate signals.

💡 Key Features & Customizations:

Adaptive Length: Enable adaptive length based on the market's current conditions.

SNR Threshold: Set your desired SNR threshold for filtering signals.

Exit Length: Define the length for exit signals.

📈 Trading Signals:

Long Entry: Elegant Oscillator and Decycler cross above 0, source crosses above Decycler, source is greater than an increasing Instantaneous Trendline, Spearman Rank is positive, and SNR exceeds the threshold.

Long Exit: Source crosses below the Instantaneous Trendline after entering a long position.

Short Entry: Elegant Oscillator and Decycler cross below 0, source crosses below Decycler, source is less than a decreasing Instantaneous Trendline, Spearman Rank is negative, and SNR exceeds the threshold.

Short Exit: Source crosses above the Instantaneous Trendline after entering a short position.

📊 Insights & Enhancements:

Dynamic Length: The strategy adapts its length dynamically based on market conditions.

Improved SNR: Signal to Noise Ratio ensures better filtering of signals.

Enhanced Visualization: The Elegant Oscillator now features improved color coding for a clearer interpretation.

🚨 Disclaimer:

Trading involves risk, and this script should be used judiciously. It's not a guaranteed profit machine, but with careful use, it can be a valuable addition to your toolkit.

Feel free to backtest, tweak, and make it your own! Let's conquer the markets together! 💪📈

🚀✨ Happy Trading! ✨🚀

---

🙌 Credits:

A big shoutout to the original contributors:

@blackcat1402

@cheatcountry

@DasanC

ATR_RSI_Strategy v2 with no repaint [liwei666]🎲 Overview

🎯 this is a optimized version based on ATR_RSI_Strategy with no-repaint.

Sharpe ratio: 1.4, trade times: 116 ,

trade symbol: BINANCE:BTCUSDTPERP 15M

you can get same backtesting result with the correct settings.

🎲 Strategy Logic

🎯 the core logic is quite simple, use ATR and RSI and SMA

1. when price is in high volatility ( atr_value > atr_ma);

2. wait for a break signal (rsi_value > rsi_buy or rsi_value < rsi_sell);

3. entry Long or Short,use trailing stop-loss to max security and percent TP to keep profit.

🎲 Settings

🎯 there are 7 input properties in script, but I only finetune 4 of them ( bold field below ),

you may change other parameter to get better result by yourself.

atr_length: length to get atr value

atr_ma_length : length of smoothing atr value

atr_ma_norm_min : atr_ma normalized min value, filter high volatility ranges

atr_ma_norm_max : atr_ma normalized max value, filter high volatility ranges

rsi_length : length to get rsi value

rsi_entry: 50 +/- rsi_entry to get entry threshold

trailing_percent: trailing stop-loss percent

🎲 Usage

🎯 the commission set to 0.05% , part of exchange the commission is less than 0.05% in reality,

but I will still use 0.05% in my next script.

🎯 this script use 50% of equity to size positions follow general script position,

you can adjust the value to fix size or 100% of equity to compare result with other strategy,

but I still suggest you use 5-10% of equity for each strategy in reality.

🎯any questions please comment below. if there are any words violate House Rule, please tell me below and i will revise immediately

don't want be hiddened again 😂😂

Additionally, I plan to publish 20 profitable strategies in 2023;

let‘s witness it together!

Hope this strategy will be usefull for you :)

enjoy! 🚀🚀🚀

Adaptive Fisherized ROCIntroduction

Hello community, here I applied the Inverse Fisher Transform, Ehlers dominant cycle determination and smoothing methods on a simple Rate of Change (ROC) indicator

You have a lot of options to adjust the indicator.

Usage

The rate of change is most often used to measure the change in a security's price over time.

That's why it is a momentum indicator.

When it is positive, prices are accelerating upward; when negative, downward.

It is useable on every timeframe and could be a potential filter for you your trading system.

IMO it could help you to confirm entries or find exits (e.g. you have a long open, roc goes negative, you exit).

If you use a trend-following strategy, you could maybe look out for red zones in an in uptrend or green zones in a downtrend to confirm your entry on a pullback.

Signals

ROC above 0 => confirms bullish trend

ROC below 0 => confirms bearish trend

ROC hovers near 0 => price is consolidating

Enjoy! 🚀

Multi Supertrend with no-repaint HTF option strategyThis is the strategy version of the multi supertrend indicator.

The RoMDD looks good :)

Checked in ETHUSDT 1hour with auto HTF ON.

Have a look :)

Multi Supertrend with no-repaint and HTF optionThis indicator has 2 Supertrends to filter the trend.

The Default one uses the same timeframe as chart.

The additional Supertrend is non-repaint type and can run on higher timeframes.

It has an auto-higher timeframe selection option, thanks to LonesomeTheBlue, the original author.

It is accurate on current timeframe also.

Stochastic + ATRStochastic oscillator with dynamic buy/sell levels. Levels calculate with volatility/averag true range. No repaint

Peak/Valley EstimationEarly Signal

Estimating the Peaks and Valleys or extrema of the price is one of the best way to catch up early movements of a trend. Of course there is no perfect way to do so, if we want a perfect estimation of peaks and valleys then we must use a non causal indicator ( repainting ), if we want a causal indicator ( non repainting ) then we will need to tradeoff accuracy for allowing our indicator to be causal, its always a matter of tradeoff at the end when trying to have a desired effect (smoothness/lag for filters) .Our indicator is causal, it wont repaint but the accuracy will depend on various parameters.

In order to detect peaks and valleys in a certain period we must detrend the price, this mean subtracting it by its moving average. We take the absolute value of this result and we filter it with a local linear regression ( LSMA ) in order to eliminate noise, then we make the assumption that the highest of our result is or a peak or a valley of the price, so we divide our detrended calculation by its highest and we get a scaled result. Lets call this final result the peak index .

Parameters

There are 3 parameters in this indicator, a length parameter who control the period of the highest mentioned above, a smooth parameter who smooth our detrended price, and finally a mod parameter who select the trigger method for estimating a peak/valley.

Here are how mods work :

mod = 1 : when the peak index is equal to 1 and the previous value is not equal to 1 then we have a peak/valley. Its the fastest of the 3 mods but the one with less accuracy.

mod = 2 : when the peak index crossunder 0.8 then we have a peak/valley. This method is more robust but slower than the previous one.

mod = 3 : when the peak index is not equal to 1 and the previous peak index is equal to 1 then we have a peak/valley. Its an average of the precedents mod in term of speed and accuracy.

Lower length values tend to estimate the peak/valley of short periods of time but can also lead to the reverse desired effect ( breakouts signals ). Smoothing is important since it reduce the number of noise in our calculation and therefore help to get better results, its a parameter that should be high, sometimes higher than length if this one is low.

Estimation of medium terms peaks/valleys with length and smooth parameter both period 100 and mod = 3

Estimation peaks in palladium way to early, an example of bad accuracy. Such behaviour can be fixed with a change in the parameters.

Complementarity With Classics Indicators

As i said before its always a matter of tradeoff, here we get faster signals but we loose in accuracy, at the contrary classics indicators often have slower signals but with more accuracy. Mixing both of them can provide additional robustness in a strategy, lets take back our palladium case, using mod 3 could have been better, but its still not optimal, so lets use a classic indicator such as a moving average of period 200, our conditions are :

Long when our peak/valley estimator estimated a valley and the price crossover our moving average.

Short when our peak/valley estimator estimated a peak and the price crossunder our moving average.

here is an exemple of such signal :

We balanced our tradeoff in a way to fix both methods problems, of course its still not a perfect fix but it provide more robustness.

Other Uses

The indicator can also be used only as an order closing indicator, its safer than taking a position based on its estimation. The indicator can also give a use to the peak index used in the calculation as a trend strength indicator.

Values below 0.5 indicate a ranging market while values over 0.5 indicate a trending market.Since its a scaled measure you can use it a smoothing constant in a adaptive filter.

Conclusions

I showed how to estimate peaks and valleys and how to use such information in order to make better decision when using classical indicators, of course at the end nothing is perfect and considering the non stationarity of the markets the parameters efficiency could change drastically.

For any questions/demands feel free to pm me, i would be happy to help you