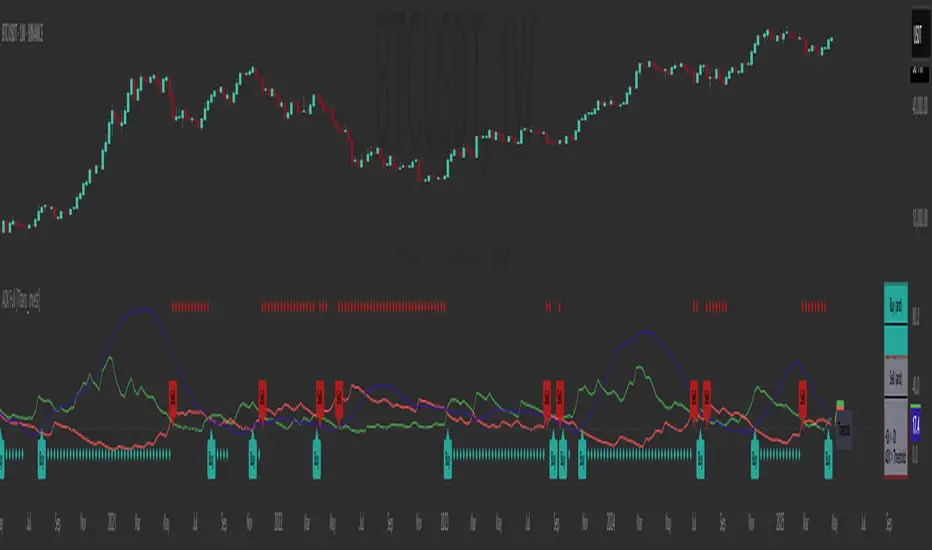

Stochastics + VixFix Buy/Sell SignalsThis script is designed for long-term investors using ETFs on a weekly timeframe, where catching high-probability bottoms is the goal. It combines the Stochastic Oscillator with the Williams VixFix to identify moments of extreme fear and potential reversals.

A Buy signal is triggered when:

Stochastic %K drops below 20

VixFix forms a green spike (suggesting a panic-driven market flush)

A Sell signal is triggered when:

Stochastic %K rises above 90

VixFix falls below 5 (indicating excessive complacency)

Catching tops is much harder than catching bottoms.

These Sell signals are not designed to fully exit positions. Instead, they suggest trimming a small portion of ETF holdings — simply to free up liquidity for future opportunities.

This strategy is ideal for:

Long-term ETF investors

Weekly charts

Systematic decision-making in volatile markets

Use in conjunction with macro indicators, sector rotation, and valuation frameworks for best results.

Pine Script® göstergesi