Fusion: Trend and thresholdsThis is your basic single moving average but with a "slope" component. The idea here is that once a slope reaches a value great enough you should probably only trade with the trend so this indicator allows you to set that threshold separately for going long and short.

The indicator is designed to display on both the main chart and a separate chart area. If you want to display it on the main chart then the quick way is to just check the "On main chart" option and it will disable off main chart items and then just move it to the main chart.

There's half a dozen or so moving average types to select from so you will probably find one that suits you pretty well.

Once a threshold is reached you will get a signal showing the trend is strong enough where you probably should not trade in the opposite direction.

There is a "normalize" option which will fix the oscillator to a maximum of 100. The upside of this is that you can be more consistent in your settings of a threshold. The down side is that normalization happens over a predefined number of bars so it's a floating number, not an absolute number however I set the number of bars default to 3,000 so it should be pretty close to ideal. I haven't found a perfect way of getting a consistent maximum on the oscillator as a benchmark yet so if anyone has any ideas please contact me and I'll do an update. I may look into using percentage rank instead of normalization.

I like to see it as both an oscillator and on the main chart so I generally have two copies.

The settings are certainly not optimized so set to whatever suits your needs as my defaults will probably be wrong for you.

The code is structured to easily drop into a bigger system so use it as a lone indicator or add the code to some bigger project you are creating. If you do, send me a note, it would be nice to know it's being well used.

Finally, if you find value please do make a comment, give a thumbs up etc.

Enjoy and good luck!

Doğrusal Regresyon

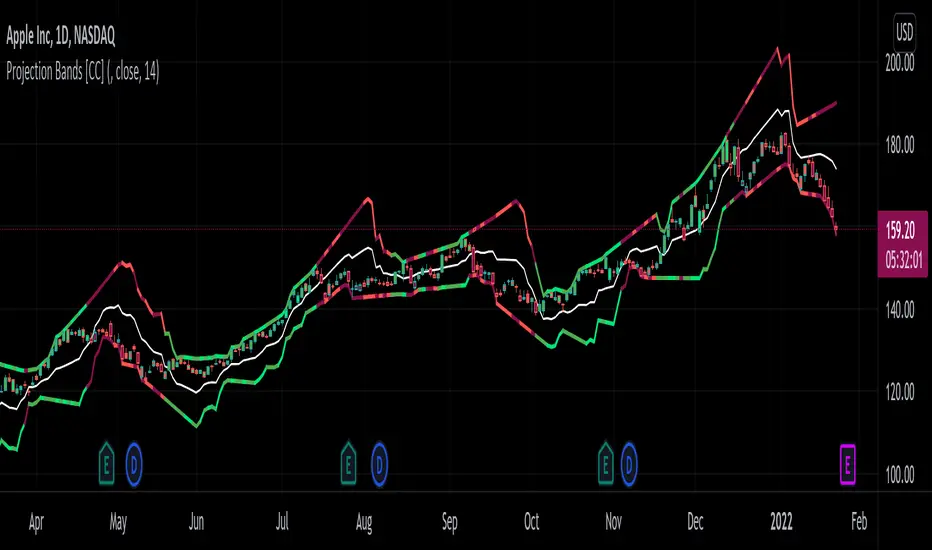

Projection Bands [CC]The Projection Bands were created by Mel Widner (Stocks and Commodities Jul 1995) and this indicator and the other two that rely on this one (I will publish them later) are very underappreciated in my humble opinion. The biggest strength of this indicator is the fact that it is a leading indicator for dramatic price movements. As you can see in my example chart it consistently gives great exit points before a downturn. I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

Linear Regression 200/100/50/20Four time frames in one indicator in different colors, showing current price trend in different scopes.

If the slope of the smaller time frame is in a (0,75;1,25) interval of some of the bigger ones the smaller one is omitted (different signs near zero are not coalesced in that way though).

Every time frame has four deltas of range in trend lines of different grade of transparency (2-1-4-3), as well as a vertical line denoting regression date range start, also bearing the same color (blue-red-green-gray for 200/100/50/20).

On the right of the latest bar are Pearson coefficients and slopes of the regressions, 200/100/50/20 bottom-up, also appropriately colored.

Pairs Trading (basic OLS regression)Pairs trading using hedge ratio.

Firstly, it calculates hedge ration using OLS linear regression.

Then it calculates spread and z-score of spread.

if spread in specific range (which it's possible to change in settings) it makes Long/Short orders.

The very basic script.

Linear Regression Histogram [LuxAlgo]This indicator is inspired by traditional statistical histograms. It will return the number of occurrences of price falling within each interval (bins) of the linear regression channel. This can be useful to highlight zones of interest within a trend.

Settings

Length: Number of recent closing prices used for the computation of the linear regression.

Bins Number: Number of intervals constructed from the linear regression channel.

Mult: Multiplicative factor for the RMSE. Controls the width of the linear regression channel.

Src: Input source of the indicator.

Usage

The indicator is constructed by dividing the linear regression channel range into a series of intervals (bins) of equal width. We then count the number of price values falling within each interval.

If a significant number of price values fall within a specific interval then that interval can highlight a potential zone of interest within a trend.

The zone of interest is highlighted in blue.

RSI Linear Regression with ZigZag by zdmreBoth the RSI (Relative Strength Index) and the Linear Regression ( LR ) rank among the most popular momentum indicators used in trading. When used in combination with other technical indicators (ZigZag), both RSI, LR and ZigZag can offer value in validating trade opportunities to optimize your risk management practices.

Here’s a look at how to use RSI, LR and ZigZag (Can be used for divergence patterns.) as part of your trade analysis.

If you have new ideas to improve this indicator then let me know please.

***Use it at your own risk

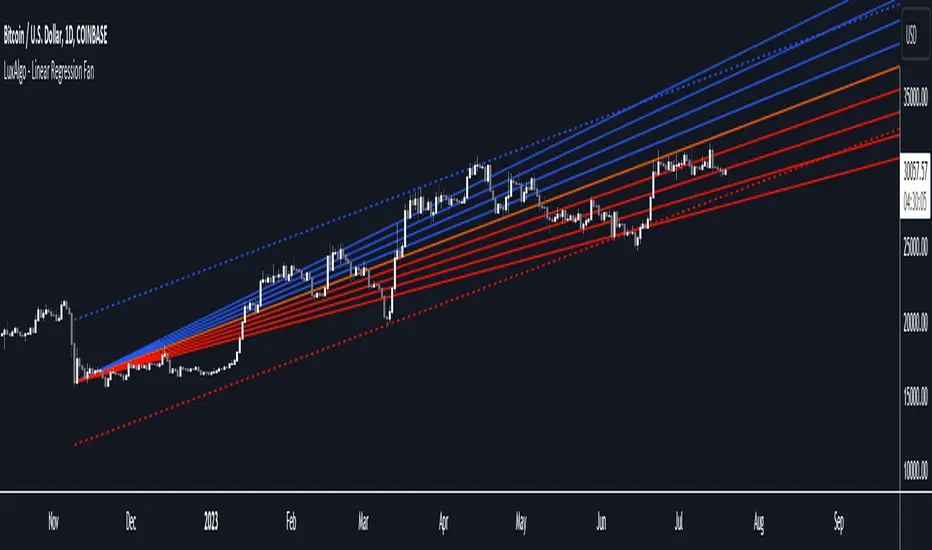

Linear Regression Fan [LuxAlgo]This indicator displays a fan using a linear regression fit to the price as a base. All lines are equidistant and are drawn from the first point of the linear regression to the most recent point of the linear regression plus the root-mean-square deviation (RMSD) multiplied by a certain factor.

Settings

Length: Lookback period for the linear regression.

Mult: Multiplier for the RMSD, allows returning wider fans.

Lines Per Side: Number of lines on each side of the fan.

Src: Input source of the indicator.

Usage

Traders often use the lines of fans to determine significant points of support or resistance at which they might expect price variations to reverse.

The length can be adjusted so that the starting point of the linear regression is located at a pivot high/low.

Some technical analysts use the measure rule of broadening wedges with fans when price breaks one of the extremities. This allows setting precise take-profits/stop-losses.

To learn more about the measure rule see:

log-log Regression From ArraysCalculates a log-log regression from arrays. Due to line limits, for sets greater than the limit, only every nth value is plotted in order to cover the entire set.

Exponential Regression From ArraysCalculates an exponential regression from arrays. Due to line limits, for sets greater than the limit, only every nth value is plotted in order to cover the entire set.

The Echo Forecast [LuxAlgo]This indicator uses a simple time series forecasting method derived from the similarity between recent prices and similar/dissimilar historical prices. We named this method "ECHO".

This method originally assumes that future prices can be estimated from a historical series of observations that are most similar to the most recent price variations. This similarity is quantified using the correlation coefficient. Such an assumption can prove to be relatively effective with the forecasting of a periodic time series. We later introduced the ability to select dissimilar series of observations for further experimentation.

This forecasting technique is closely inspired by the analogue method introduced by Lorenz for the prediction of atmospheric data.

1. Settings

Evaluation Window: Window size used for finding historical observations similar/dissimilar to recent observations. The total evaluation window is equal to "Forecast Window" + "Evaluation Window"

Forecast Window: Determines the forecasting horizon.

Forecast Mode: Determines whether to choose historical series similar or dissimilar to the recent price observations.

Forecast Construction: Determines how the forecast is constructed. See "Usage" below.

Src: Source input of the forecast

Other style settings are self-explanatory.

2. Usage

This tool can be used to forecast future trends but also to indicate which historical variations have the highest degree of similarity/dissimilarity between the observations in the orange zone.

The forecasting window determines the prices segment (in orange) to be used as a reference for the search of the most similar/dissimilar historical price segment (in green) within the gray area.

Most forecasting techniques highly benefit from a detrended series. Due to the nature of this method, we highly recommend applying it to a detrended and periodic series.

You can see above the method is applied on a smooth periodic oscillator and a momentum oscillator.

The construction of the forecast is made from the price changes obtained in the green area, denoted as w(t) . Using the "Cumulative" options we construct the forecast from the cumulative sum of w(t) . Finally, we add the most recent price value to this cumulated series.

Using the "Mean" options will add the series w(t) with the mean of the prices within the orange segment.

Finally the "Linreg" will add the series w(t) to an extrapolated linear regression fit to the prices within the orange segment.

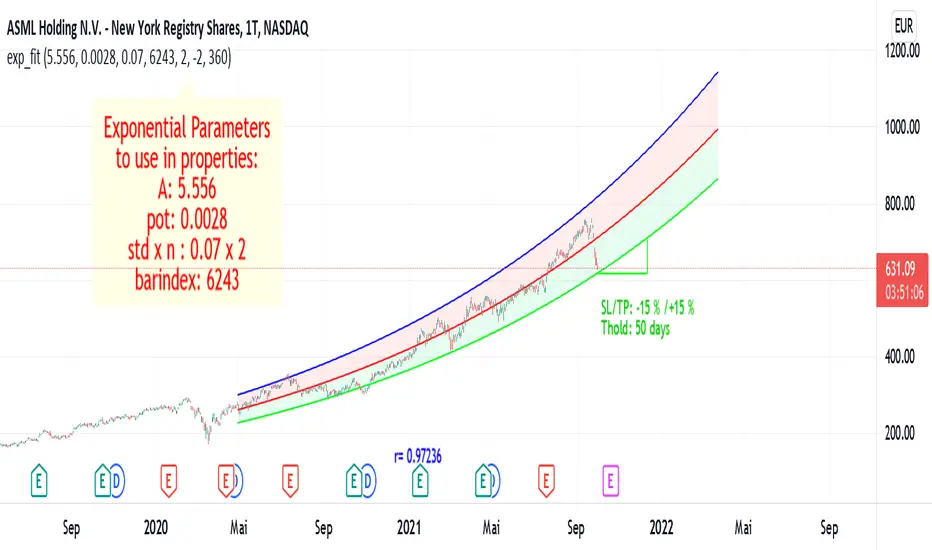

Exponential Regression Channel with novel volatilityThis code is a modified version of the built-in "linear regression" script of Tradingviews which can be plotted correctly on logarithmic charts

The log reg code of Forza was adjusted by altustro to generate an exponential regression (or a correct linear regression on the log scale, this is equivalent).

The standard deviation in the log scale is a better volatility measure which we call novola, and which defines the trend channel displayed in addition to the main indicator.

The exponential regression slope and channel also defines the typical holding time of the stock and the SL/TP boundaries, which are calculated and displayed at the last bar.

The display works both in log and regular scale. But only in the log scale it can be compared to the linear extension, which can also be plotted when activated in the properties.

The underlying exponential fit can not be displayed in regular scale as only lines can be plotted by TV. But with the related script Exponental Regression also the exponential regression can be exactly displayed using a workaround.

Exponential RegressionIn Tradingview it is not possible to actually display arbitrary non-linear functions retrospectively.

Series objects can only depend on the current or past bars

Thus, while regression is possible, display of a non-linear curve into the past is not possible

This script is a workaround to be able to still display an exponential fit of the last n bars.

It is based on a linear regression of the log(close). The parameters of this regression are printed in the label.

To create the correct plot, these parameters have to be written into the properties of the indicator.

The functions displayed follow the expression exp(A)* exp(pot*t+d)

where d =0 for the center line, and d = +-std * upperMult for the upper and lower line respectiveley.

The parameters of the function are:

amplitude in log scale A

exponent of the exponential function pot

standard deviation of the linear regression std

number of bars of the current chart bindex

multiplicator of the std of the upper and lower exponential line upperMult and lowerMult +

This code is a version of the built-in "linear regression" script of Tradingview alztered by Forza so it can be plotted correctly on logarithmic charts

The code of Forza was further adjusted by altustro to be able to plot the full exponential curve also in regular scale

MACD Linear Regression by zdmreBoth the Moving Average Convergence Divergence (MACD) and the Linear Regression (LR) rank among the most popular momentum indicators used in trading. When used in combination with other technical indicators, both MACD and LR can offer value in validating trade opportunities to optimize your risk management practices.

While they represent a similar approach to evaluating trades, the functions of both MACD and LR are distinct, which makes them useful indicators to combine in trade evaluation. Here’s a look at how to use MACD and LR as part of your trade analysis.

***Use it at your own risk

If you have new ideas to improve this indicator then let me know please.

Keep Learning, Keep Earning

MACandles-LinearRegression-StrategyThis is combination of multiple indicators and strategies. Mainly useful for indexes and to time the entry and exits of indexes. No stoploss used - makes it less desirable for leveraged trades or trading individual stocks.

Let us rewind and look back at some of the indicators/strategies published earlier.

1. Moving Average Candles - this is one of my favourite tool for general trend filtering. Applying supertrend on moving average candles is one of the easiest ways to find reversal in trending market without exiting positions too early. Few scripts published on this basis are:

MA Candles Supertrend

MA Candles Supertrend Strategy

2. VixFix and Linear Regression - this itself is combination of two indicators.

Williams-Vix-Fix-Finds-Market-Bottoms - by @ChrisMoody

Squeeze-Momentum-Indicator - by @LazyBear

I have combined these two indicators to derive VIX-Fix linear regression to find absolute market bottoms. More description here:

VixFixLinReg-Strategy

VixFixLinReg-Indicator

Now, in this strategy, we combine all these together.

Derive moving average candles

Derive momentum of moving average candles

Derive Linear regression on momentum

Optionally, also calculate VIX Fix and Linear regression on VixFix momentum

To find market bottom:

There are two options

1. Use when momentum of MA candles hit bottom (red) and slowly turn up (orange). In aggressiveLong mode, signals are also generated when momentum starts going positive from negative.

2. Use Vix Fix linear regression of MA candles as described in the original script of VixFixLinReg-Strategy

To find market top

Here only Ma candles momentum decreasing is used as signal. If looking for longTrades , exit signal is generated only when momentum is turning negative extreme(orange). Or else, exit signal is generated when momentum has turned neutral.

At this stage, it is very much experimental - use it with caution :)

KINSKI Volume Regression TrendRegression trends are typically used to determine when a price is unusually far from its baseline. The script calculates the linear regression of volume and price to determine the trend direction and strength. This can be used to determine the volume support for upward/downward trends.

As a special feature, this indicator allows you to choose from three (as of 07/20/2021) templates with special presets.

The following templates are available:

"Precise" (Period: 4, Smoothing Factor Type: "DISABLED", Smoothing Factor Length = 1).

"Smooth" (Period: 4, Smoothing Factor Type: "RMA", Smoothing Factor Length = 2)

"Long Term (Period: 20, Smoothing Factor Type: "DISABLED", Smoothing Factor Length = 1)

In the selection for templates, the option "DISABLED" can also be selected. Then the user-defined settings selectable under it take effect. There are the following setting options.

"Length": Adjustable period

"Smoothing Factor: Type": Type of moving average

"Smoothing Factor: Length": Adjustable period

Other setting options are:

Color codes: The color codes are explained in the settings

Display types: "Columns", "Histogram", "Area", "Line", "Stepline"

DAYOFWEEK performance1 -Objective

"What is the ''best'' day to trade .. Monday, Tuesday...."

This script aims to determine if there are different results depending on the day of the week.

The way it works is by dividing data by day of the week (Monday, Tuesday, Wednesday ... ) and perform calculations for each day of the week.

1 - Objective

2 - Features

3 - How to use (Examples)

4 - Inputs

5 - Limitations

6 - Notes

7 - Final Tooughs

2 - Features

AVG OPEN-CLOSE

Calculate de Percentage change from day open to close

Green % (O-C)

Percentage of days green (open to close)

Average Change

Absolute day change (O-C)

AVG PrevD. Close-Close

Percentage change from the previous day close to the day of the week close

(Example: Monday (C-C) = Friday Close to Monday close

Tuesday (C-C) = Monday C. to Tuesday C.

Green % (C1-C)

Percentage of days green (open to close)

AVG Volume

Day of the week Average Volume

Notes:

*Mon(Nº) - Nº = Number days is currently calculated

Example: Monday (12) calculation based on the last 12 Mondays. Note: Discrepancies in numbers example Monday (12) - Friday (11) depend on the initial/end date or the market was closed (Holidays).

3 - How to use (Examples)

For the following example, NASDAQ:AAPL from 1 Jan 21 to 1 Jul 21 the results are following.

The highest probability of a Close being higher than the Open is Monday with 52.17 % and the Lowest Tuesday with 38.46 %. Meaning that there's a higher chance (for NASDAQ:AAPL ) of closing at a higher value on Monday while the highest chance of closing is lower is Tuesday. With an average gain on Tuesday of 0.21%

Long - The best day to buy (long) at open (on average) is Monday with a 52.2% probability of closing higher

Short - The best day to sell (short) at open (on average) is Tuesday with a 38.5% probability of closing higher (better chance of closing lower)

Since the values change from ticker to ticker, there is a substantial change in the percentages and days of the week. For example let's compare the previous example ( NASDAQ:AAPL ) to NYSE:GM (same settings)

For the same period, there is a substantial difference where there is a 62.5% probability Friday to close higher than the open, while Tuesday there is only a 28% probability.

With an average gain of 0.59% on Friday and an average loss of -0.34%

Also, the size of the table (number of days ) depends if the ticker is traded or not on that day as an example COINBASE:BTCUSD

4 - Inputs

DATE RANGE

Initial Date - Date from which the script will start the calculation.

End Date - Date to which the script will calculate.

TABLE SETTINGS

Text Color - Color of the displayed text

Cell Color - Background color of table cells

Header Color - Color of the column and row names

Table Location - Change the position where the table is located.

Table Size - Changes text size and by consequence the size of the table

5 - LIMITATIONS

The code determines average values based on the stored data, therefore, the range (Initial data) is limited to the first bar time.

As a consequence the lower the timeframe the shorter the initial date can be and fewer weeks can be calculated. To warn about this limitation there's a warning text that appears in case the initial date exceeds the bar limit.

Example with initial date 1 Jan 2021 and end date 18 Jul 2021 in 5m and 10 m timeframe:

6 - Notes and Disclosers

The script can be moved around to a new pane if need. -> Object Tree > Right Click Script > Move To > New pane

The code has not been tested in higher subscriptions tiers that allow for more bars and as a consequence more data, but as far I can tell, it should work without problems and should be in fact better at lower timeframes since it allows more weeks.

The values displayed represent previous data and at no point is guaranteed future values

7 - Final Tooughs

This script was quite fun to work on since it analysis behavioral patterns (since from an abstract point a Tuesday is no different than a Thursday), but after analyzing multiple tickers there are some days that tend to close higher than the open.

PS: If you find any mistake ex: code/misspelling please comment.

Support and ResistanceThis indicator shows three types of support and resistance lines: Horizontal, Parallel (using linear regression) and Fibonacci Retracement. Lines can be adjusted or turned on and off in settings. A great tool for setting up entries, exits and locating pivot points.

Martyv Auto Fib Extension with Logarithmic SupportSimilar to the Auto Fib Retracement tool - I took the out-of-the-box functionality and added Logarithmic support, as well as nicer colors and easier management of levels. I'm... 90% sure I got the Fib calculations correct. If you see something, say something! Would love any suggestions for improvement.

Grid Bot AutoThis script is an auto-adjusting grid bot simulator. This is an improved version of the original Grid Bot Simulator. The grid bot is best used for ranging/choppy markets. Prices are divided into grids, or trade zones, that will trigger signals each time a new zone is entered. During ranging markets, each transaction is followed by a “take profit.” As the market starts to trend, transactions are stacked (compare to DCA ), until the market consolidates. No signals are triggered above the Upper Limit or Below the Lower Limit. Unlike the previous version, the upper and lower limits are calculated automatically. Grid levels are determined by four factors: Smoothing, Laziness, Elasticity, and Grid Intervals.

Smoothing:

A moving average (or linear regression) is applied to each close price as a basis. Options for smoothing are Linear Regression, Simple Moving Average, Exponential Moving Average, Volume-Weighted Moving Average, Triple-Exponential Moving Average.

Laziness:

Laziness is the percentage change required to reach the next level. If laziness is 1.5, the price must move up or down by 1.5% before the grid will change. This concept is based on Alex Grover’s Efficient Trend Step. This allows the grids to be based on even price levels, as opposed to jagged moving averages.

Elasticity:

Elasticity is the degree of “stickiness” to the current price trend. If the smoothing line remains above (or below) the current grid center without reverting but still not enough to reach the next grid level, the grid line will start to curve toward the next grid level. Elasticity is added to (or subtracted from) the gridline by a factor of minimum system ticks for the current pair. Elasticity of zero will keep the gridlines horizontal. If elasticity is too high, the grid will distort.

Grid Intervals:

Grid intervals are the percentage of space between each grid.

Laziness = 4%, Elasticity = 0. Price must move at least 4% before reaching the next level. With zero elasticity, gridlines are straight.

Laziness = 5%, Elasticity = 100. For each bar at a new grid level, the grid will start “curve” toward the next price level (up if price is greater than the middle grid, down if less than middle grid). Elasticity is calculated by the user-inputted “Elasticity” multiplied by the minimum tick for the current pair (ELSTX = syminfo.mintick * iELSTX)

Try experimenting with different combinations of the Smoothing Length, Smoothing Type, Laziness, Elasticity, and Grid Intervals to find the optimum settings for each chart. Lower-priced pairs (e.g. XRP/ADA/DODGE) will require lower Elasticity. Also note that different exchanges may have different minimum tick values. For example, minimum tick for BITMEX:XBTUSD and BYBIT:BTCUSD is .5, but BINANCE:BTCUSDT and COINBASE:BTCUSD is .01.

s3.tradingview.com

DODGEUSDT, 5min. Laziness: 4%, Elasticity 2.5

Number of Grids: 2. Laziness: 3.75%. Elasticity: 150. Grid Interval 2%.

Settings Overview

Smoothing Length : Smoothing period

Smoothing Type : Linear Regression, Simple Moving Average, Exponential Moving Average, Volume-Weighted Moving Average, Triple-Exponential Moving Average

Laziness : Percentage required for price to move until it reaches the next level. If price does not reach the next level (up or down), the grid will remain the same as previous grid (because it’s lazy).

Elasticity : Amount of curvature toward the next grid, based on the current price trend. As elasticity increases, gridlines will curve up or down by a factor of the number of ticks since the last grid change.

Grid Interval : Percent between grid levels.

Number of Grids : Number of grids to show.

Cooldown : Number of bars to wait to prevent consecutive signals.

Grid Line Transparency : Lower transparencies brighten the gridlines; higher transparencies dim the gridlines. To hide the gridlines completely, enter 100.

Fill Transparency: Lower transparencies brighten the fill box; higher transparencies dim the fill box. To hide the fill box completely, enter 100.

Signal Size : Make signal triangles large or small.

Reset Buy/Sell Index When Grids Change : When a new grid is formed, resetting the index may prevent false signals (experimental)

Use Highs/Lows for Signals : If enabled, signals are triggered as soon as the price touches the next zone. If disabled, signals are triggered after bar closes. Enable this for “Once Per Bar alerts. Disable for “Once Per Bar Close” alerts.

Show Min Tick : If checked, syminfo.mintick is displayed in upper-righthand corner. Useful for estimating Laziness.

Reverse Fill Colors : Default fill for fill boxes is green after buy and red after sell. Check this box to reverse.

Note: The Grid Bot Simulator scripts are experimental and works in progress. Please feel free to comment or contact me if you have suggestions/complaints.

Linear Regression + Moving Average1. Linear Regression including 2 x Standard Deviation + High / Low. Middle line colour depends on colour change of Symmetrically Weighted Moving Average . Green zones indicate good long positions. Red zones indicate good short positions. (Custom)

2. Symmetrically Weighted Moving Average. Colour change depending on cross of offset -1. (Fixed)

3. Exponentially Weighted Moving Average. Colour change depending on cross with Symmetrically Weighted Moving Average. (Custom)

Envious Linear Regression TrendHey traders, this is a linear regression moving average trend indicator that is designed to filter out noise and give you a better insight of the current trend in the market. The design is a linear regression cloud that covers above the price or below the price and it changes colour based on the current dominant line through the crossover and crossunder feature. This indicator should be used as a confluence and not as a "trade the crossover indicator" and it is recommended that you combine this with analysis such as support and resistance to see how the market is doing. This indicator works best with Heikin Ashi candlesticks and it supports all chart types too.

Features:

3 Length Modes that are changeable via input on the settings.

Custom Bar Colour

Crossover Markups

Re-Entry Markups

Realtime Optimized Linear Regression Channelthis script is based on "Optimized Linear Regression Channel" by alexgrover, whose page I recommend you to visit, to read the extensive description he provides

the main difference with the original version is the fact that the start point of the channel (left point) is fixed by setting the time (Begin time input).

This way, the channel size is automatically set, meaning that the channel grows larger as new data comes in, while the starting point remains at the same spot

this can be useful to track a new trend that may be forming from an inflection point or pivot, by selecting begin time as the time of the inflection

also, an end date input is provided to limit the size of the channel.

The script provides two channels:

the main channel that contain all data from begin to end time

the best fit channel that finds the best linear fit inside data from begin to end time

one issue that the script has is the limit in the number of points of size of the channel, that if too large then make the channel disappear (sigh)