Global Liquidity IndexThe Global Liquidity Index offers a consolidated view of all major central bank balance sheets from around the world. For consistency and ease of comparison, all values are converted to USD using their relevant forex rates and are expressed in trillions. The indicator incorporates specific US accounts such as the Treasury General Account (TGA) and Reverse Repurchase Agreements (RRP), both of which are subtracted from the Federal Reserve's balance sheet to give a more nuanced view of US liquidity. Users have the flexibility to enable or disable specific central banks and special accounts based on their preference. Only central banks that both don’t engage in currency pegging and have reliable data available from late 2007 onwards are included in this aggregated liquidity model.

Global Liquidity Index = Federal Reserve System (FED) - Treasury General Account (TGA) - Reverse Repurchase Agreements (RRP) + European Central Bank (ECB) + People's Bank of China (PBC) + Bank of Japan (BOJ) + Bank of England (BOE) + Bank of Canada (BOC) + Reserve Bank of Australia (RBA) + Reserve Bank of India (RBI) + Swiss National Bank (SNB) + Central Bank of the Russian Federation (CBR) + Central Bank of Brazil (BCB) + Bank of Korea (BOK) + Reserve Bank of New Zealand (RBNZ) + Sweden's Central Bank (Riksbank) + Central Bank of Malaysia (BNM).

This tool is beneficial for anyone seeking to get a snapshot of global liquidity to interpret macroeconomic trends. By examining these balance sheets, users can deduce policy trajectories and evaluate the global economic climate. It also offers insights into asset pricing and assists investors in making informed capital allocation decisions. Historically, riskier assets, such as small caps and cryptocurrencies, have typically performed well during periods of rising liquidity. Thus, it may be prudent for investors to avoid additional risk unless there's a consistent upward trend in global liquidity.

J-SPX

CE - Market Performance TableThe 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is a sophisticated market tool designed to provide valuable insights into the current market trends and the approximate current position in the Macroeconomic Regime.

Furthermore the 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 provides the Correlation Implied Trend for the Asset on the Chart. Lastly it provides information about current "RISK ON" or "RISK OFF" periods.

Methodology:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 tracks the 15 underlying Stock ETF's to identify their performance and puts the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below ETF's:

Dividends (SPHD)

Low Beta (SPLV)

Quality (QUAL)

Defensives (DEF)

Growth (IWF)

High Beta (SPHB)

Cyclicals (IYT, IWN)

Value (IWD)

Small Caps (IWM)

Mid Caps (IWR)

Mega Cap Growth (MGK)

Size (OEF)

Momentum (MTUM)

Large Caps (IWB)

Overall Settings:

The main time values you want to change are:

Correlation Length

- Defines the time horizon for the Correlation Table

ROC Period

- Defines the time horizon for the Performance Table

Normalization lookback

- Defines the time horizon for the Trend calculation of the ETF's

- For longer term Trends over weeks or months a length of 50 is usually pretty accurate

Visuals:

There is a variety of options to change the visual settings of what is being plotted and the two table positions and additional considerations.

Everything that is relevant in the underlying logic that can help comprehension can be visualized with these options.

Market Correlation:

The Market Correlation Table takes the Correlation of the above ETF's to the Asset on the Chart, it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single ETF.

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement. This is strengthened by taking the average of all Implied Trends.

With this the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset, for Traders and Investors alike, over the defined time duration.

Market Performance:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is the actual valuable part of this Indicator.

It provides valuable information about the current market environment (whether it's risk on or risk off), the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction.

Utility:

The 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Style Factors:

Are the values green for a specific Column? If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Style Factors:

Are the values red for a specific Column? If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

EMAflowPRO -Ranges-DISCLAIMER: Always, please keep in mind that market conditions change, past results cannot guarantee the same results in the future.

EMAflowPRO - Ranges-

EMAflowPRO ranges indicator will detect key movements in the market that fit certain conditions and based on that create key tradable zones by providing dynamic and static range levels.

Before reading further please take a look at the indicator values names on the right in the main chart above - these names are linked to the content below when we talk about range structure. The examples included in charts are linked to the area we're discussing (if something was said - most likely closest chart demonstrates it - Also arrows present entries; can be limit or can be market buy/sell in to the wicks.)

Let's find out what indicator does...

Static range logic:

Indicator uses combination of market timing indicators (counting relationship between candles) , fisher transform, stoch rsi, bollinger bands to detect important market price action that show strenght - based on that it will project a static range where key goal is to predict where market will be extremely oversold, extremely overbought or where market could change bias etc.

The setups it provides are very similar to those that come out of harmonic patterns - but it was developed with unique approach without knowing what harmonic patterns are.. so it's not completly the same.

Range is represented by 3 tradable areas (actual trade ideas on charts - arrow points towards a level - on the right there is a scale with a number- limit order can be placed there )

Top of the range - It serves as a shorting area or if top is converted to support can also signal a potential breakout or start of new trend.

Example of a short the top of the range:

29732 - is area where wicks can be sold in to , or limit sell is placed - with higher leverage sl should be tight, with lower sell orders can be spread out up to the middle with sl just above 30500, targets can be choosen based on the provious range top as % moves point.

Example of longing the levels on the recent rise - price staying above middle of the top of the range keeps bias on the upside and potentially signals a break out or start of new trend

Uppper, Middle, Lower part of the range: Sideway area - middle of the range decides direction , above favors the upper levels , below favors the lower levels.

Very nice example where white line is middle of the range and shows that even in strong trend - range projection is able to accurately predict key pullback areas that provide substantial gain. See image below - again settign limit orders where middle of the range is allows you to get a comfortable entry with very big risk reward ratio.

Bottom of the range - market is extremely oversold

Spx example of our recent range from last year's summer - again chart includes both EMAflow indicator and EMAflow ranges as all indicators are extremely complementary and present two sides of the medal sideway and trend view.

Chart only contains ranges but shows the same pair and time:

If price goes below middle of the bottom of the range it could signal a break down or start of new bearish trend.

Dynamic range logic

Since sometimes static range gets broken out or is not respected and the price action is not yet sufficient to generated a new one we included a dynamic supply demand part where dynamic range is generated working in a similar way but does add clarity when static range fails.

example of this can be seen when ftx caused a btc dump we broke through the bottom of the range but dynamic range later showed us new bottom we could trade.

Confluence between both can also provide even more sure levels to place limit orders or to market buy or sell when wicks in to that area occurs.

Minuses:

Since ranges tend to work best when market is sideway - a second part is recommended with EMAflowPRO where focus on moving averages helps you navigate stronger trends.

Not all tfs are well synced with ranges on various assets so you will need to flip through few ones to find the best timeframes that historically worked the best - if you come across an asset that doens't look good you should just change timeframe to higher until you see something that fits or change asset until you get something that looks clear.

Settings:

EMAflow - Ranges - allows you to preset minimum potential of a trade setup you want to look for - default is 6% that ensures you can get a good setup on lower and higher tfs.

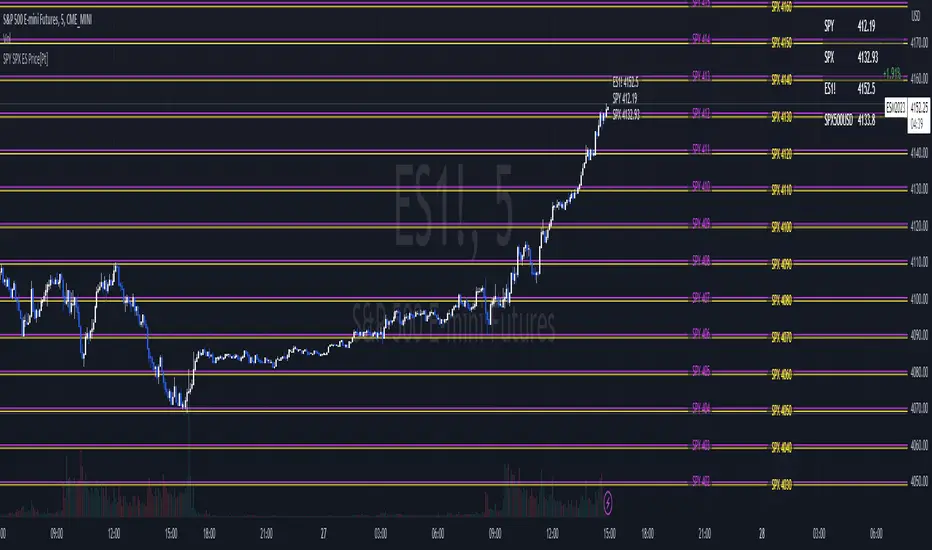

SPX ES SpreadA very simple indicator to display the spread between ES and SPX. The table by default displays in the upper right corner of the chart. If you are on the chart for SPX, it will show the current price of ES, as well as the difference in points between the two. Similarly, if on the chart for ES, it will show the price for SPX as well as the difference in points between the two. The table does not appear at all if the chart symbol is anything other than ES or SPX. The specific symbols used can be defined by the user.

[TT] Sectors Dist % From MA- The script shows the distance in percentages from the 200 MA (or any other MA period) , for the 11 SP500 sectors.

- It works based on the current time frames.

Could be useful when working with mean reversion strategies to detect extremes zones and overbought/oversold conditions in the given sectors compared others.

SPY SPX ES Price Converter+ [Pt]This is a + version of my original SPY SPX ES Price Converter indicator

Description

The SPY SPX ES Price Converter is a powerful and easy-to-use tool that allows traders to view corresponding price levels for linked instruments in real-time. This includes SPY, SPX, ES, and SPX500USD. Although these instruments often move in sync, differences in price movements, volume, and trading hours can create unique key levels and support/resistance areas for each. By mapping these levels on the same chart, traders can more easily spot trading opportunities and improve their chances of success.

Customizable features

- multiplier from the closest whole number price level

- line color

- line style

- label position / size

- # of levels to display

- toggle current price display table

|| ------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------||

This script includes the following premium unique features.

SPY / SPX Gaps detector

A gap is an area on a chart where the price between two bars changes significantly without any trades happening between them. Such gaps often occur when a strong shift in sentiment happens during the hours when markets are usually closed. This indicator highlights these gaps on the chart and extends them further until they have been covered (i.e., when a newer bar has crossed that gap).

Overnight gaps from SPY or SPX can be mapped directly onto ES chart

VWAPs

VWAPs of these linked instruments can be mapped onto the chart. For example, ES VWAP mapped onto SPY chart, or vise versa. This allows for clear visualization of the price action near these VWAP levels.

Custom Cross Instruments Price Targets

Want to trade SPY options while watching ES chart or vise versa? You can setup to 8 price targets and see the corresponding converted price level. No need to switch between charts to try to figure out which price level corresponds to which.

SPY SPX ES Price Converter [Pt]A must have tool for SPY SPX ES traders~!!!

Description

The SPY SPX ES Price Converter is a powerful and easy-to-use tool that allows traders to view corresponding price levels for linked instruments in real-time. This includes SPY, SPX, ES, and SPX500USD. Although these instruments often move in sync, differences in price movements, volume, and trading hours can create unique key levels and support/resistance areas for each. By mapping these levels on the same chart, traders can more easily spot trading opportunities and improve their chances of success.

Customizable features

- multiplier from the closest whole number price level

- line color

- line style

- label position / size

- # of levels to display

- toggle current price display table

Market Relative Candle Ratio ComparatorIntroducing the Market Relative Candle Ratio Comparator, a visually captivating script that eases the way you compare two financial assets, such as cryptocurrencies and market indices. Leveraging a distinctive calculation method based on percentage changes and their averages, this tool presents a crystal-clear view of how your chosen assets perform in relation to each other, both for individual candles and over a range of previous candles.

Tailoring the script to your preferences is a walk in the park, as it allows you to easily adjust input symbols, moving average lengths, and other parameters to match your analytical approach. The visually arresting column chart it creates employs vivid red and green colors to underscore the differences between the two assets on each candle. Simultaneously, the lower-opacity columns depict the accumulated differences over a specified lookback period. This vibrant blend of colors and opacities results in a dynamic visual experience, enabling you to better grasp market trends relative to each other.

The reverse bool input is a handy feature that lets you invert the effect of the input symbol (DXY by default) in the comparison. When you set the reverse input to true, the script multiplies the calculated DXY percentage change by -1, effectively reversing the comparison. This is particularly useful when examining assets with an inverse relationship or when you'd like to analyze the input symbol's impact in the opposite direction.

For instance, if the input symbol represents a market index that generally moves in the opposite direction of the selected cryptocurrency, enabling the reverse input will help you better visualize and understand the relationship between the two assets by inverting the input symbol's effect on the comparison.

In the accompanying chart, you can observe the comparison of Bitcoin's movement relative to the Dollar, Gold, Bonds, and the S&P 500. The indicator reveals that in the last day, Bitcoin outperformed Bonds, Gold, and the Dollar but not the S&P 500!

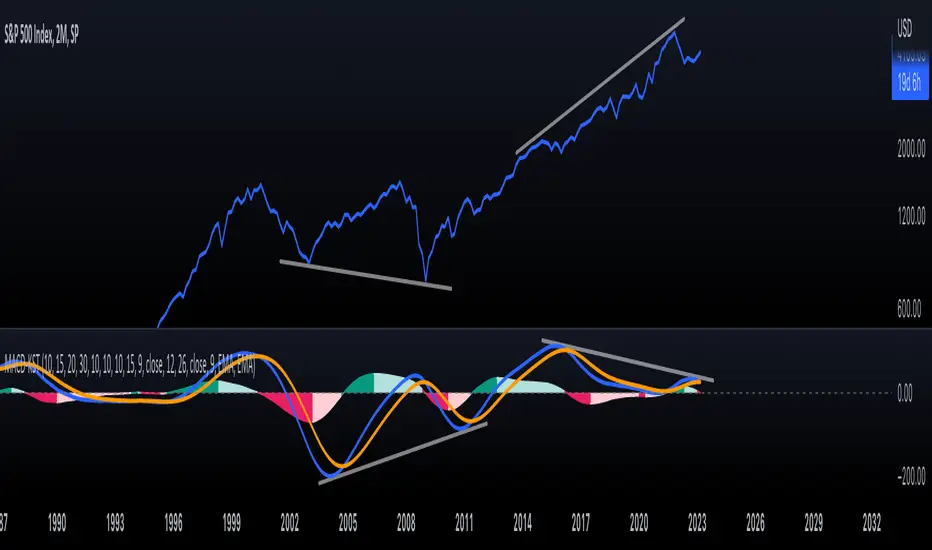

KST-Based MACDAs a follow-up to my previous script:

I am posting a stand-alone KST-based MACD.

Note that this indicator is highly laggy. Specific care must be taken when using it.

The MACD-Signal crossing is quite delayed but it is a definite confirmation.

For earlier signs, the Histogram must be analyzed. A shift from Green-White signals the 1st Bear Signal.

A MACD-Signal crossing signals the 2nd Bear SIgnal.

The same applies for bull-signs.

This indicator is useful for long-term charts on which one might want to pinpoint clear, longterm divergences.

Standard RSI, Stochastic RSI and MACD are notoriously problematic when trying to pinpoint long-term divergences.

Finally, this indicator is not meant for pinpointing entry-exit positions. I find it useful for macro analysis. In my experience, the decreased sensitivity of this indicator can show very strong signs, that can be quite laggy.

Inside the indicator there is a setting for "exotic calculations". This is an attempt to make this chart work in both linear/ negative charts (T10Y2Y) and log charts (SPX)

Tread lightly, for this is hallowed ground.

-Father Grigori

SPX Fair Value Bands WSHOSHOThis is a variation of the SPX Fair Value Bands indicator which uses WSHOSHO instead of WALCL.

WSHOSHO only includes the 'Securities Held Outright' portion of the Fed balance sheet. This effectively eliminates the portions related to BTFP (Bank Term Funding Program).

4C Options Expected Move (Weekly + 0DTE)This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) Daily options, for a quick visual reference.

Please Note: This indicator is different from our original "4C Expected Move (Weekly Options)" indicator, as it now packages the ability to ALSO plot 0DTE options expected moves along with Weekly expected moves. Many other newer features have also been implemented.

Background Information

The Expected Move (EM) is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of options pricing and implied volatility.

This range can be viewed as possible support and resistance, or, once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

About the Indicator

This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) options, for a quick visual reference.

For the weekly EM, the range is based on the Weekly close of the prior week.

For the Daily EM based on 0DTE options, the range is based on the Daily close of the prior day.

The indicator will automatically start a new weekly EM plot at the beginning of the week, and a new daily EM at the beginning of each day.

The EM values must be updated weekly and/or daily.

Features

Plots the EM for the week

Plots the EM for the day, for symbols that offer daily expiration options

Plots the 2 Standard Deviation EM for both the weekly and daily EM

Labels with calculated values are plotted near the levels for quick visual aid

Settings

Can toggle weekly EM on/off

Can toggle Daily EM on/off

Can toggle 2 Standard Deviation lines on/off

Can toggle labels for all EM on/off

Robust line settings

Can adjust label location left/right based on personal preference

Can enter symbol into settings as a reference

Handy instructions in the settings

How To Set Up The Indicator

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Usually, you can look at the stock's option chain to find the weekly expected move.

You will have to do your own research to find where this information is displayed depending on your broker. You may also need to find the information elsewhere if your broker does not have this information.

You can also do your calculation of the EM using the following formula (please do your own research):

Expected Move = Option Price x Implied Volatility x Square Root of Time

See screenshot example below

This is the Thinkorswim platform's option chain, and the Implied Volatility % and the calculated EM are on the right side of the option chain.

The Expected Move is circled in blue. Use the +- number in parentheses, NOT the % value.

For the weekly EM, input the number that corresponds to the weekly option into the indicator. This must be done on a weekly basis, and It is typically best to use the EM for the next week expiration that is generated AFTER the Friday close and/or before the Monday open of the upcoming week.

For the daily EM, input the number that corresponds to the daily 0DTE option into the indicator. This must be done on a daily basis, and it is typically best to use the EM value for the 0DTE option that is generated the night before (after market close), or before the market opens for that 0DTE. .

Pin Candle DetectionPin candles are a variation of hammer candles that are useful in technical analysis . In particular, when combined with volume profile studies, they can be a powerful set up for long entries or other decision making.

For example, when looking at volume profiles, a long entry would be a fair value area (i.e. 40%) below the close of a pin candle. When combined with a support level , the set up is stronger.

While most scripts look for hammer candles, pin candles are somewhat different in that the length of the wick is significant.

This script and its parameters was built for ES futures 15 min chart in mind.

This script is unique in that it allows for the below parameters to be adjusted to suit other instruments and timeframes:

1. Fib level: Candle must close within a certain retracement level). My preference is 0.55. Some traders like 0.5, while others prefer 0.33

2. Wick length: Pin candles differ from pure hammers in that the length of the wick must be significant. My preference is 7 points on ES (as in $ and not ticks)

Add this script to your alerts to no longer miss these set ups.

Failed Breakdown Detection'Failed Breakdowns' are a popular set up for long entries.

In short, the set up requires:

1) A significant low is made ('initial low')

2) Initial low is undercut with a new low

3) Price action then 'reclaims' the initial low by moving +8-10 points from the initial low

This script aims at detecting such set ups. It was coded with the ES Futures 15 minute chart in mind but may be useful on other instruments and time frames.

Business Logic:

1) Uses pivot lows to detect 'significant' initial lows

2) Uses amplitude threshold to detect a new low beneath the initial low; used /u/ben_zen script for this

3) Looks for a valid reclaim - a green candle that occurs within 10 bars of the new low

4) Price must reclaim at least 8 points for the set up to be valid

5) If a signal is detected, the initial low value (pivot low) is stored in array that prevents duplicate signals from being generated.

6) FBD Signal is plotted on the chart with "X"

7) Pivot low detection is plotted on the chart with "P" and a label

8) New lows are plotted on the chart with a blue triangle

Notes:

User input

- My preference is to use the defaults as is, but as always feel free to experiment

- Can modify pivot length but in my experience 10/10 work best for pivot lows

- New low detection - 55 bars and 0.05 amplitude work well based on visual checks of signals

- Can modify the number of points needed to reclaim a low, and the # of bars limit under which this must occur.

Alerts:

- Alerts are available for detection of new lows and detection of failed breakdowns

- Alerts are also available for these signals but only during 7:30PM-4PM EST - 'prime time' US trading hours

Limitations:

- Current version of the script only compares new lows to the most recent pivot low, does not look at anything prior to that

- Best used as a discretionary signal

Visit /u/ben_zen's Profile:

www.tradingview.com

Profile Link www.tradingview.com

Global Net Liquidity - SPX Fair ValueThis is similar to the SPX Fair Value Bands indicator.

It currently only displays the fair value.

The original SPX Fair Value formula only includes the Fed balance sheet data.

This indicator incorporates the following central bank assets:

Fed

Japan

China

UK

ECB

This is currently experimental. Feel free to explore using different formula constants.

Price Distance RatioThis study plots the ratio between current price and the price N days ago.

With N input that is configurable, users can find optimal long/short entries when price is in an established trend and price has diverge far from a given local peak or all time high.

With many years of stock trading the analysis indicates a connection between the distance of price and subsequent returns.

Portfolios of stocks with lower price to local highes ratios generally underperformed portfolios of stocks with higher prices to peaks reached similar N days ago.

The highest returns to previous peak are recorded when buying at the biggest dip.

For example, the purchase at 20% drawdown could generate 25% when price returns to the peak. The purchase at 50% drawdown could generate bigger, i.e. 100% return, when price returns to the peak. And the purchase at 90% drawdown could generate much bigger, i.e. 900% return, in a case the price returns to the peak.

However, buying very far below local peaks on almost all holding periods produces lower CAGR returns because of "timing adjustment". In simple words, typically the drawdown takes less time vs. further recovery.

For example:

👉 The largest BTC drawdown in 2013-2015 took 410 days (Peak-to-Valley) . And the recovery of BTC to new highs took 771 days (Valley-to-Peak) after that.

👉 The 3rd longest drawdown in BTC took 363 days (observed from December 17, 2017 to December 15, 2018). And further recovery in BTC to its new high took almost two years - 716 days .

👉The 4th longest drawdown in BTC took 162 days (observed from June 08, 2011 to November 17, 2011). And further recovery in BTC to its new high took more than a year - 469 days .

The concept of this study could recognizes at least 4 different modes of action.

👉 In a clearly established upward trend traders should be buying (following the trend) when Ratio is above 100% and reducing the size when Ratio turns below 100%.

👉 Conversely, in a clearly established downward trend traders should be shorted when Ratio is below 100% and covering when the Ratio turns back to 100%.

👉 In a sideways movement traders are advised to wait carefully if the Ratio near 100% for a long time, and take a position the trend is clear.

👉 Chartists can analyze the dynamic of the indicator - both in terms of trends and overall level. For example as it shown at the chart.

The understading of the study and rules of "timing adjustments" could genarate the awesome opportunities for stock options traders also, with strategies of selling uncovered call options and vertical call spreads.

// Many thanks to @HPotter and @Wheeelman wizards for their continious support and assistance.

SPX IC Intraday & StatsThis indicator was designed for traders who make intraday Iron Condors with the SPX.

It basically has 2 main parts:

Part 1:

The indicator shows the distance, in real time, between the current SPX price and the IC selling wings (calls and puts wings) that have been selected. This result is displayed in percentages and in points. In the upper right corner (for calls) and lower right corner (for puts). The label will change color as the price moves closer to or further away from the sell strike. Darker red color as it approaches the wings, lighter green color as the price approaches the center of the Iron Condor.

Part 2:

Statistical dashboard showing the number of times in the past that from a certain hour (the current time) to the market close (4pm US East Time) the SPX moved outside or inside the width of the selected wings. The position of the table is configurable. By default, it's in the upper right corner.

Dashboard:

First Date: the first day of the sample (this varies depending on the timeframe, the higher the timeframe the larger the sample is, as TradingView counts more bars backwards, by default TV offers 10000 bars for the PRO version). Recommended 5 minutes.

Range Time: refers to the time range of the sample. From the current time to 4pm (US East Time).

Deviation Wing (%): It's the deviation (in percentage) based on the current time, from the current SPX price to the wing strikes. It takes the smaller value, either call or put wing.

Total Days: the number of days in the sample.

In range Days: the number of days that the price remained in that range from the current time to the market close.

Out of Range Days: the number of days the price ended outside that range from the current time to the market close.

Configuration:

Open Time (Hour): IC opening hour.

Open time (Minute): IC opening minutes.

Width Wings: width of the wings from the SPX price at the configured time.

Mini Rectangles: Refers to include within the IC 4 deviations (mini rectangles) to better visualize where the SPX price is with reference to the wings. Darker red color as it gets closer to the wings, lighter green color as the price gets closer to the center of the Iron Condor.

Add SMAs: Add SMAs 8, 20 and 50 to the IC chart.

Include Fundamental Days: Include or not in the sample important news days. They are considered: FED Meetings, CPI Reports, Unemployment Reports, Powell Speech.

Include Days: (Monday, Tuesday, Wednesday, Thursday, Friday). Include (or not) in the sample the chosen days.

Apply Filters Since: Sampling start date. Per default: False.

Table Position: Dashboard position.

Note 1: It's recommended to use the Dark Theme Color of TradingView.

Note 2: this indicator will only work in intraday timeframes less than 30 minutes (1m, 2m, 5m, 10m, 15m, 30m) and will only show results while the market is open.

************************************

Spanish Version:

Este indicador fue diseñado para los traders que hacen intradías de Iron Condors con el SPX.

Básicamente cuenta con 2 partes principales:

Parte 1:

El indicador muestra la distancia, en tiempo real, entre el actual precio del SPX y las alas vendedoras (alas calls y puts) que se hayan seleccionado. Este resultado se muestra en porcentajes y en puntos. En la esquina superior derecha (para los calls) e inferior derecha (para los puts). El label cambiará de color a medida que el precio se acerque o aleje del precio de las alas. Color rojo más oscuro a medida que se acerque a las alas, color verde claro cuando el precio se acerque al centro del Iron Condor.

Parte 2:

Dashboard estadístico que muestra la cantidad de veces que desde una determinada hora (el tiempo actual) hasta el cierre del mercado (4pm US East Time) el SPX se movió fuera o dentro del ancho de las alas seleccionadas. La posición de la tabla es configurable. Por defecto esta en la esquina superior derecha.

Dashboard:

First Date: el primer día de la muestra (esto varía dependiendo el timeframe, a mayor timeframe la muestra es mayor, ya que TradingView contará más barras para atrás (por default TV ofrece 10000 barras para la versión PRO). Recomendado 5 minutos.

Range Time: se refiere al rango horario de la muestra. Desde la hora actual hasta las 4pm (US East Time)

Deviation Wing (%): Es la desviación en porcentaje en base a la hora actual, desde el precio actual del SPX hasta el ancho de las alas. Toma el menor valor, sea al ala call o al ala put.

Total Days: la cantidad de días de la muestra.

In range Days: la cantidad de días que el precio se mantuvo en ese rango desde la hora actual hasta el cierre del mercado

Out of Range Days: la cantidad de días que el precio terminó fuera de ese rango desde la hora actual hasta el cierre del mercado.

Configuración:

Open Time (Hour): Hora de apertura del IC.

Open time (Minute): Minutos de apertura del IC.

Width Wings: ancho de las alas desde el precio del SPX a la hora configurada.

MiniRectangles: Se refiere a incluir dentro del IC 4 desviaciones (mini rectángulos) para visualizar de mejor manera donde se encuentra el precio del SPX con referencia a las alas. Color rojo más oscuro a medida que se acerque a las alas, color verde claro cuando el precio se acerque al centro del Iron Condor.

Add SMAs: Agrega al cuadro las SMA 8, 20 y 50.

Include Fundamental Days: Incluye o no en la muestra días de noticias importantes. Son considerados: FED Meetings, CPI Reports, Unemployment Reports, Powell Speech.

Include Days: (Monday, Tuesday, Wednesday, Thursday, Friday). Incluye (o no) en la muestra los días elegidos.

Apply Filters Since: Fecha de comienzo del muestreo.

Table Position: Posición del dashboard.

Nota 1: se recomienda usar el Dark Theme Color de TradingView.

Nota 2: este indicador solo funcionará en temporalidades intradías menores a 30 minutos (1m,2m,5m,10m,15m,30m) y Solo mostrará resultados mientras el mercado esté abierto, o sea en tiempo real.

SPX Implied Probability of closing above/belowThis is a recreation of the work done by Michael Rechenthin aka "Dr.Data" from Tastytrade back in 2016 (this indicator is for SP:SPX only)

You can watch the episode where "Dr.Data", Tom and Tony go over this concept on the following link:

www.tastytrade.com

The following are my personal additions:

- ability to choose between TVC:VIX and NASDAQ:VOLI as the IV input

- ability to choose between 252 and 365 for the number of days

Note that I’m displaying 4 decimal places (#.####) to be as accurate as possible but sometimes you will see 0% or 100% displayed which means that more decimal places are needed (0% could be 0.00005% or 100% could be 99.99995%).

SPX Expected MoveThis indicator plots the "expected move" of SPX for today's trading session. Expected move is the amount that SPX is predicted to increase or decrease from its current price, based on the current level of implied volatility. The implied volatility in this indicator is computed from the current value of the VIX (or one of several volatility symbols available on Trading view). The computation is done using standard formula. The resulting plots are labeled as 1 and 2 standard deviations. The default values are to use VIX as well as 252 trading days in the years.

Use the square root of (days to expiration, or in this case a fraction of the day remaining) divided but the square root of (252, or number of trading days in a year).

timeRemaining = math.sqrt(DTE) / math.sqrt(252)

Standard deviation move = SPX bar closing price * (VIX/100) * timeRemaining

ILM CFTC COT Legacy PlotUse this indicator on Daily Timeframe

Please refer to the below link for CFTC Disaggregated COT

www.cftc.gov

This script is very similar to COT Financial Plot indicator except that it plots the data for Futures in Legacy buckets Commercial vs. Non-Commercial

Volatility Inverse Correlation CandleThis is an educational tool that can help you find direct or inverse relations between two assets.

In this case I am using VIX and SPX .

The way it works is the next one :

So I am looking at the current open value of VIX in comparison with the previous close ( if it either above or below) and after on the SPX I am looking into the history and see for example which type of candle we had in respect with the opening value from VIX .

So for example, lets imagine that today is monday, and the weekly open value from VIX was higher than previous friday close value. Now I am going to see with the inverse correlation , if based on this idea, the current weekly candle from SPX finished in a bear candle.

The same can be applied for the bearish situation, so if we had an open from VIX lower than previous close, we are looking to check the SPX bull candle accuracy.

At the same time, for a different type of calculation I have added an internal lookup into heikin ashi values.

If you have any questions please let me know !

Top 40 constituents of S&P 500 IndexDisplays real-time candles of top 40 constituents of S&P 500 Index ( TVC:SPX ) for a given time frame, side-by-side. This gives an overall idea of breadth and depth of market movements in the time-frame.

Please note that, this is not a standard chart rendered bar-wise and may take time to load as it requests multiple securities. You could modify the contents, from settings, to include stocks from your portfolio or indices of different sectors.

ILM COT Financial Table - CFTCUse this indicator on Daily Timeframe

Please refer to the below link for CFTC Financials

www.cftc.gov

This script shows the Financial COT for the respective instrument by deriving the CFTC code.

Option is provided to override the CFTC code

User can also configure the historical CFTC data view

The script calculates the Long% vs Short% for various categories (Dealers/Asset Managers/Leveraged Funds/Other Reportables) and color codes the column appropriately.

The goal of this script is to show all the financial CFTC data on a single page to digest the data better in a tabular form

Fixed the default TradingView Library which has some errors with CFTC code mapping.

For example, SPX CFTC Code #13874+ which is the most important one where big players take positions is not there in the default Library.

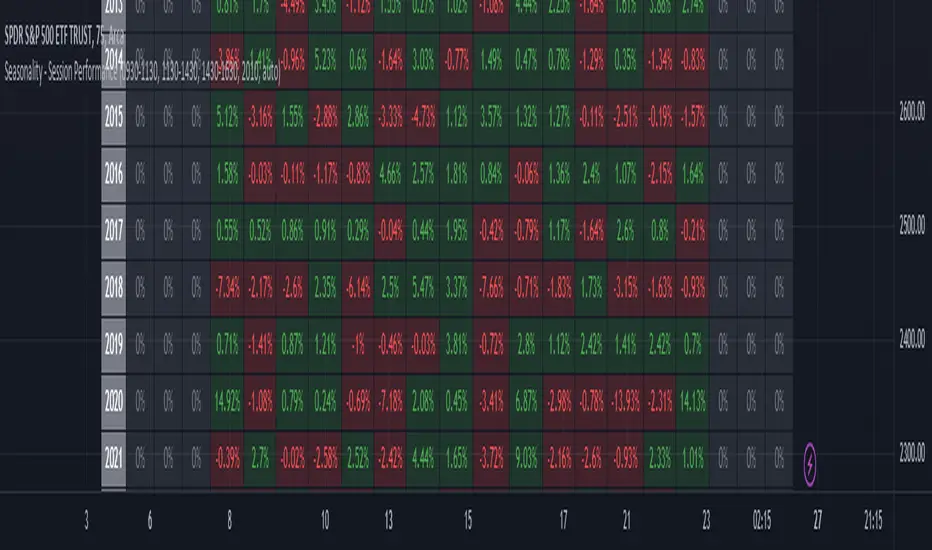

Seasonality - Session Performance - Morning Afternoon EveningUse this indicator on Intraday Timeframe. Higher the timeframe, more the data

This script calculates the performance of an instrument for different sessions.

Session inputs can be updated to study performance of

- Morning vs Afternoon vs Evening

- Pre-Market vs Market vs Post-Market (provided the data feed supports pre and post market)

- Overnight vs Intraday

Three session inputs are provided to tweak the session range

Performance is calculated as session close / session open - 1

Session timeframes can be set for various countries. Make sure the session timeframe aligns with the Candle open/close for the timeframe you choose. Some examples below

US Markets: 0930-1130 1130-1430 1430-1630 Timeframe 1 hour

India Markets: 0915-1030 1030-1415 1415-15:30 Timeframe 75min