Kalman Gain Parameter MechanicsFrequently asked question is to explain how Gain parameter works in kalman funtion. This script serves as a visual representation of Gain parameter of Kalman function used in HMA-Kalman & Trendlines script. (The function creator's name was misspeled in that script as Kahlman)

To see better results set your Chart's timeframe to Daily.

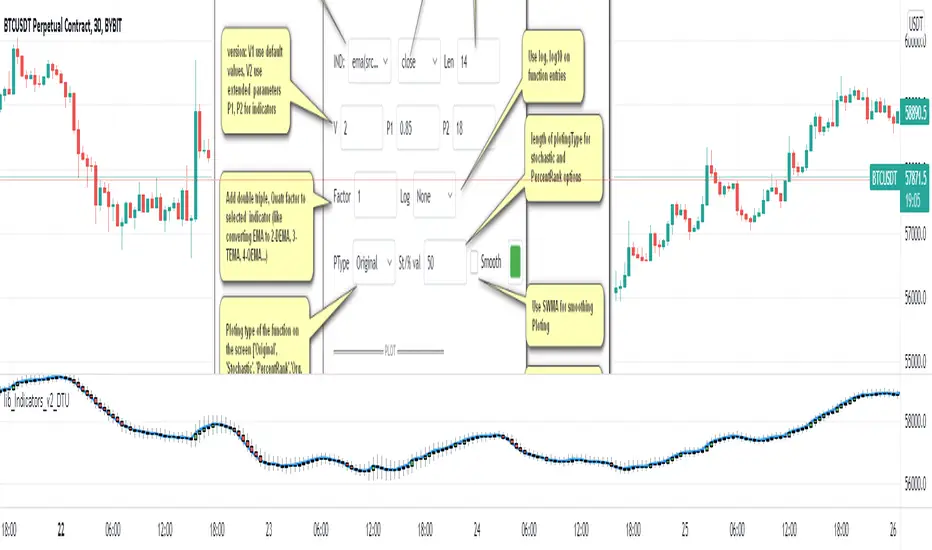

Factor

Indicator Functions with Factor and HeikinAshiHello all,

This indicator returns below selected indicators values with entered parameters.

Also you can add factorization, functions candles, function HeikinAshi and more to the plot.

VERSION:

Version 1: returns series only source and Length with already defined default values

Version 2: returns series with source, Length, p1 and p2 parameters according to the indicator definition (ex: )

PARAMETERS p1 p2

for defining multi arguments (See indicators list) indicator input value usable with verison=V2 selected.. ex: for alma( src , len ,offset=0.85,sigma=6), set source=source, len=length, p1=0.85 an p2=6

FACTOR:

Add double triple, Quadruple factors to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

1-Original

2-Double

3-Triple

4-Quadruple

LOG

Log: Use log, log10 on function entries

PLOTTING:

PType: Plotting type of the function on the screen

Original :use original values

Org. Range (-1,1): usable for indicators between range -1 and 1

Stochastic: Convert indicator values by using stochastic calculation between -1 & 1. (use AT/% length to better view)

PercentRank: Convert indicator values by using Percent Rank calculation between -1 & 1. (use AT/% length to better view)

ST/%: length for plotting Type for stochastic and Percent Rank options

Smooth: Use SWMA for smoothing the function

DISPLAY TYPES

Plot Candles: Display the selected indicator as candle by implementing values

Plot Ind: Display result of indicator with selected source

HeikinAshi: Display Selected indicator candles with Heikin Ashi calculation

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma( src , len ,offset=0.85,sigma=6)', // Arnaud Legoux Moving Average

ama = 'ama( src , len ,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', // Accumulation/distribution index.

cma = 'cma( src , len )', //Corrective Moving average

dema = 'dema( src , len )', // Double EMA (Same as EMA with 2 factor)

ema = 'ema( src , len )', // Exponential Moving Average

gmma = 'gmma( src , len )', //Geometric Mean Moving Average

hghst = 'highest( src , len )', //Highest value for a given number of bars back.

hl2ma = 'hl2ma( src , len )', //higest lowest moving average

hma = 'hma( src , len )', // Hull Moving Average .

lgAdt = 'lagAdapt( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre( src , len )', //Ehler's Laguerre filter

lsrcp = 'lesrcp( src , len )', //lowest exponential esrcpanding moving line

lexp = 'lexp( src , len )', //lowest exponential expanding moving line

linrg = 'linreg( src , len ,loffset=1)', // Linear regression

lowst = 'lowest( src , len )', //Lovest value for a given number of bars back.

pcnl = 'percntl( src , len )', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli( src , len )', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema( src , len )', //Range EMA (REMA)

rma = 'rma( src , len )', //Moving average used in RSI . It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma( src , len )', // Smoothed Moving Average

smma = 'smma( src , len )', // Smoothed Moving Average

supr2 = 'super2( src , len )', //Ehler's super smoother, 2 pole

supr3 = 'super3( src , len )', //Ehler's super smoother, 3 pole

strnd = 'supertrend( src , len ,period=3)', //Supertrend indicator

swma = 'swma( src , len )', //Sine-Weighted Moving Average

tema = 'tema( src , len )', // Triple EMA (Same as EMA with 3 factor)

tma = 'tma( src , len )', //Triangular Moving Average

vida = 'vida( src , len )', // Variable Index Dynamic Average

vwma = 'vwma( src , len )', // Volume Weigted Moving Average

wma = 'wma( src , len )', //Weigted Moving Average

angle = 'angle( src , len )', //angle of the series (Use its Input as another indicator output)

atr = 'atr( src , len )', // average true range . RMA of true range.

bbr = 'bbr( src , len ,mult=1)', // bollinger %%

bbw = 'bbw( src , len ,mult=2)', // Bollinger Bands Width . The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci( src , len )', // commodity channel index

cctbb = 'cctbbo( src , len )', // CCT Bollinger Band Oscilator

chng = 'change( src , len )', //Difference between current value and previous, source - source.

cmo = 'cmo( src , len )', // Chande Momentum Oscillator . Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog( src , len )', //The cog (center of gravity ) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve( src , len )', // Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl( src , len )', // Correlation coefficient . Describes the degree to which two series tend to deviate from their ta. sma values.

count = 'count( src , len )', //green avg - red avg

dev = 'dev( src , len )', //ta.dev() Measure of difference between the series and it's ta. sma

fall = 'falling( src , len )', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr( src , len ,mult=2)', // Keltner Channels Range

kcw = 'kcw( src , len ,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd( src , len )', // macd

mfi = 'mfi( src , len )', // Money Flow Index

nvi = 'nvi()', // Negative Volume Index

obv = 'obv()', // On Balance Volume

pvi = 'pvi()', // Positive Volume Index

pvt = 'pvt()', // Price Volume Trend

rise = 'rising( src , len )', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc( src , len )', // Rate of Change

rsi = 'rsi( src , len )', // Relative strength Index

smosc = 'smi_osc( src , len ,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig( src , len ,fast=5, slow=34)', //smi Signal

stdev = 'stdev( src , len )', //Standart deviation

trix = 'trix( src , len )' , //the rate of change of a triple exponentially smoothed moving average .

tsi = 'tsi( src , len )', //True Strength Index

vari = 'variance( src , len )', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta. sma ), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc( src , len )', // Williams %R

wad = 'wad()', // Williams Accumulation/Distribution .

wvad = 'wvad()' //Williams Variable Accumulation/Distribution

I will update the indicator list when I will update the library

Thanks to tradingview, @RodrigoKazuma for their open source indicators

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change

rsi = 'rsi(src,len)', //Relative strength Index

smosc = 'smi_osc(src,len,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig(src,len,fast=5, slow=34)', //smi Signal

stdev = 'stdev(src,len)', //Standart deviation

trix = 'trix(src,len)' , //the rate of change of a triple exponentially smoothed moving average.

tsi = 'tsi(src,len)', //True Strength Index

vari = 'variance(src,len)', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc(src,len)', //Williams %R

wad = 'wad()', //Williams Accumulation/Distribution.

wvad = 'wvad()' //Williams Variable Accumulation/Distribution.

}

f_func(string, float, simple, float, float, float, simple) f_func Return selected indicator value with different parameters. New version. Use extra parameters for available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

Returns: float Return calculated indicator value

fn_heikin(float, float, float, float) fn_heikin Return given src data (open, high,low,close) as heikin ashi candle values

Parameters:

float : o_ open value

float : h_ high value

float : l_ low value

float : c_ close value

Returns: float heikin ashi open, high,low,close vlues that will be used with plotcandle

fn_plotFunction(float, string, simple, bool) fn_plotFunction Return input src data with different plotting options

Parameters:

float : src_ indicator src_data or any other series.....

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

Returns: float

fn_funcPlotV2(string, float, simple, float, float, float, simple, string, simple, bool, bool) fn_funcPlotV2 Return selected indicator value with different parameters. New version. Use extra parameters fora available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return calculated indicator value

fn_factor(string, float, simple, float, float, float, simple, simple, string, simple, bool, bool) fn_factor Return selected indicator's factorization with given arguments

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

simple : int fact_ Add double triple, Quatr factor to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return result of the function

fn_plotCandles(string, simple, float, float, float, simple, string, simple, bool, bool, bool) fn_plotCandles Return selected indicator's candle values with different parameters also heikinashi is available

Parameters:

string : FuncType_ indicator from the indicator list

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

bool : plotheikin_ Use Heikin Ashi on Plot

Returns: float

Dow Factor Stoch RSIThe indicator was generated by adding the Dow Factor to the Stochastic Relative Strength Index.( Stoch RSI )

The Dow factor is the effect of the correlation coefficient, which determines the relationship between volume and price, on the existing indicators.

With these codes we are able to integrate them numerically into the indicators.

For more information on the Dow factor, please see my indicator:

This code is open source under the MIT license. ( github.com )

My dow factor updates will continue.We adapted the indicators and saw successful results, now it is time to examine and develop the factor itself.

Stay tuned , best regards.

Trend Continuation FactorTrend Continuation Factor indicator script.

This indicator was originally developed by M.H. Pee (Stocks & Commodities V. 20:3 (58-64): Trend Continuation Factor).

Trend Trigger FactorTrend Trigger Factor indicator script. This indicator was originally developed by M. H. Pee (Stocks & Commodities V.22:12 (28-36): Trend Trigger Factor).

Trend continuation factor, by M.H. PeeTrend continuation factor, by M.H. Pee

The related article is copyrighted material from Stocks & Commodities.