Strategy SEMA SDI WebhookPurpose of the Code:

The strategy utilizes Exponential Moving Averages (EMA) and Smoothed Directional Indicators (SDI) to generate buy and sell signals. It includes features like leverage, take profit, stop loss, and trailing stops. The strategy is intended for backtesting and automating trades based on the specified indicators and conditions.

Key Components and Functionalities:

1.Strategy Settings:

Overlay: The strategy will overlay on the price chart.

Slippage: Set to 1.

Commission Value: Set to 0.035.

Default Quantity Type: Percent of equity.

Default Quantity Value: 50% of equity.

Initial Capital: Set to 1000 units.

Calculation on Order Fills: Enabled.

Process Orders on Close: Enabled.

2.Date and Time Filters:

Inputs for enabling/disabling start and end dates.

Filters to execute strategy only within specified date range.

3.Leverage and Quantity:

Leverage: Adjustable leverage input (default 3).

USD Percentage: Adjustable percentage of equity to use for trades (default 50%).

Initial Capital: Calculated based on leverage and percentage of equity.

4.Take Profit, Stop Loss, and Trailing Stop:

Inputs for enabling/disabling take profit, stop loss, and trailing stop.

Adjustable parameters for take profit percentage (default 25%), stop loss percentage (default 4.8%), and trailing stop percentage (default 1.9%).

Calculations for take profit, stop loss, trailing price, and maximum profit tracking.

5.EMA Calculations:

Fast and slow EMAs.

Smoothed versions of the fast and slow EMAs.

6.SDI Calculations:

Directional movement calculation for positive and negative directional indicators.

Difference between the positive and negative directional indicators, smoothed.

7.Buy/Sell Conditions:

Long (Buy) Condition: Positive DI is greater than negative DI, and fast EMA is greater than slow EMA.

Short (Sell) Condition: Negative DI is greater than positive DI, and fast EMA is less than slow EMA.

8.Strategy Execution:

If buy conditions are met, close any short positions and enter a long position.

If sell conditions are met, close any long positions and enter a short position.

Exit conditions for long and short positions based on take profit, stop loss, and trailing stop levels.

Close all positions if outside the specified date range.

Usage:

This strategy is used to automate trading based on the specified conditions involving EMAs and SDI. It allows backtesting to evaluate performance based on historical data. The strategy includes risk management through take profit, stop loss, and trailing stops to protect gains and limit losses. Traders can customize the parameters to fit their specific trading preferences and risk tolerance. Differently, it can perform leverage analysis and use it as a template.

By using this strategy, traders can systematically execute trades based on technical indicators, helping to remove emotional bias and improve consistency in trading decisions.

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Educational

Strategic Multi-Step Supertrend - Strategy [presentTrading]The code is mainly developed for me to stimulate the multi-step taking profit function for strategies. The result shows the drawdown can be reduced but at the same time reduced the profit as well. It can be a heuristic for futures leverage traders.

█ Introduction and How it is Different

The "Strategic Multi-Step Supertrend" is a trading strategy designed to leverage the power of multiple steps to optimize trade entries and exits across the Supertrend indicator. Unlike traditional strategies that rely on single entry and exit points, this strategy employs a multi-step approach to take profit, allowing traders to lock in gains incrementally. Additionally, the strategy is adaptable to both long and short trades, providing a comprehensive solution for dynamic market conditions.

This template strategy lies in its dual Supertrend calculation, which enhances the accuracy of trend detection and provides more reliable signals for trade entries and exits. This approach minimizes false signals and increases the overall profitability of trades by ensuring that positions are entered and exited at optimal points.

BTC 6h L/S Performance

█ Strategy, How It Works: Detailed Explanation

The "Strategic Multi-Step Supertrend Trader" strategy utilizes two Supertrend indicators calculated with different parameters to determine the direction and strength of the market trend. This dual approach increases the robustness of the signals, reducing the likelihood of entering trades based on false signals. Here is a detailed breakdown of how the strategy operates:

🔶 Supertrend Indicator Calculation

The Supertrend indicator is a trend-following overlay on the price chart, typically used to identify the direction of the trend. It is calculated using the Average True Range (ATR) to ensure that the indicator adapts to market volatility. The formula for the Supertrend indicator is:

Upper Band = (High + Low) / 2 + (Factor * ATR)

Lower Band = (High + Low) / 2 - (Factor * ATR)

Where:

- High and Low are the highest and lowest prices of the period.

- Factor is a user-defined multiplier.

- ATR is the Average True Range over a specified period.

The Supertrend changes its direction based on the closing price in relation to these bands.

🔶 Entry-Exit Conditions

The strategy enters long positions when both Supertrend indicators signal an uptrend, and short positions when both indicate a downtrend. Specifically:

- Long Condition: Supertrend1 < 0 and Supertrend2 < 0

- Short Condition: Supertrend1 > 0 and Supertrend2 > 0

- Long Exit Condition: Supertrend1 > 0 and Supertrend2 > 0

- Short Exit Condition: Supertrend1 < 0 and Supertrend2 < 0

🔶 Multi-Step Take Profit Mechanism

The strategy features a multi-step take profit mechanism, which allows traders to lock in profits incrementally. This is achieved through four user-configurable take profit levels. For each level, the strategy specifies a percentage increase (for long trades) or decrease (for short trades) in the entry price at which a portion of the position is exited:

- Step 1: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent1 / 100)

- Step 2: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent2 / 100)

- Step 3: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent3 / 100)

- Step 4: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent4 / 100)

This staggered exit strategy helps in locking profits at multiple levels, thereby reducing risk and increasing the likelihood of capturing the maximum possible profit from a trend.

BTC Local

█ Trade Direction

The strategy is highly flexible, allowing users to specify the trade direction. There are three options available:

- Long Only: The strategy will only enter long trades.

- Short Only: The strategy will only enter short trades.

- Both: The strategy will enter both long and short trades based on the Supertrend signals.

This flexibility allows traders to adapt the strategy to various market conditions and their own trading preferences.

█ Usage

1. Add the strategy to your trading platform and apply it to the desired chart.

2. Configure the take profit settings under the "Take Profit Settings" group.

3. Set the trade direction under the "Trade Direction" group.

4. Adjust the Supertrend settings in the "Supertrend Settings" group to fine-tune the indicator calculations.

5. Monitor the chart for entry and exit signals as indicated by the strategy.

█ Default Settings

- Use Take Profit: True

- Take Profit Percentages: Step 1 - 6%, Step 2 - 12%, Step 3 - 18%, Step 4 - 50%

- Take Profit Amounts: Step 1 - 12%, Step 2 - 8%, Step 3 - 4%, Step 4 - 0%

- Number of Take Profit Steps: 3

- Trade Direction: Both

- Supertrend Settings: ATR Length 1 - 10, Factor 1 - 3.0, ATR Length 2 - 11, Factor 2 - 4.0

These settings provide a balanced starting point, which can be customized further based on individual trading preferences and market conditions.

Short Term FS PrivateShort Term FS

Fibonacci levels, derived from the famous Fibonacci sequence, are a powerful tool in technical analysis used to identify potential support and resistance levels in the market. The narrative of using Fibonacci levels involves understanding market psychology, price action, and strategic decision-making. Here’s how this narrative unfolds:

### The Foundation: Fibonacci Sequence

The story begins with Leonardo Fibonacci, an Italian mathematician, who introduced the Fibonacci sequence to the West in the 13th century. The sequence, where each number is the sum of the two preceding ones, generates ratios that traders use to predict price movements in financial markets. The most significant ratios are 23.6%, 38.2%, 50%, 61.8%, and 100%.

### Market Psychology and Fibonacci Retracement

Imagine a stock or a commodity experiencing a significant upward trend. Traders begin to wonder when and where the price will pull back before continuing its upward trajectory. This is where Fibonacci retracement levels come into play. By drawing Fibonacci levels from the recent low to the recent high, traders identify key areas where the price might find support during a pullback.

For example, a trader observes that a stock has risen from $100 to $150. By applying Fibonacci retracement, they identify potential support levels at $138.2 (23.6% retracement), $130.9 (38.2% retracement), $125 (50% retracement), and $119.1 (61.8% retracement). These levels represent areas where buying interest may resurface, based on historical price action and market psychology.

### The Pullback and Support

As the stock begins to pull back from $150, traders watch closely as the price approaches these Fibonacci levels. At the 38.2% retracement level, they notice increased buying activity, causing the price to stabilize and potentially reverse. This indicates that many traders are using the same Fibonacci levels to make their decisions, creating a self-fulfilling prophecy.

### Fibonacci Extensions: Predicting Future Movements

Fibonacci levels are not only used to predict retracements but also to anticipate future price extensions. When the price resumes its upward movement, traders use Fibonacci extension levels to identify potential resistance points. These levels, such as 161.8%, 200%, and 261.8%, help traders set profit targets and plan their exit strategies.

Continuing the narrative, the stock recovers from the 38.2% retracement level and begins to rise again. Traders use Fibonacci extension levels drawn from the pullback low to the previous high to project potential targets. The 161.8% extension level, for instance, provides a target of $175, giving traders a clear goal for their positions.

### Combining Fibonacci with Other Indicators

To strengthen their analysis, traders often combine Fibonacci levels with other technical indicators, such as moving averages, trend lines, and oscillators. This confluence of signals increases the probability of successful trades.

In our narrative, the trader notices that the 61.8% retracement level coincides with a 200-day moving average, adding further weight to this support level. This confluence gives the trader more confidence to enter a buy position at this level.

### Real-Life Scenario

Consider a real-life example of a trader using Fibonacci levels on a major index like the S&P 500. After a significant rally from 3,000 to 4,000, the index begins to pull back. By applying Fibonacci retracement, the trader identifies key levels at 3,764 (23.6%), 3,618 (38.2%), and 3,500 (50%).

As the S&P 500 approaches the 3,618 level, the trader sees increased buying activity, signaling a potential reversal. They decide to enter a long position, setting a stop-loss just below the 38.2% retracement level and a take-profit at the 161.8% extension level at 4,300.

### Conclusion: Mastering Fibonacci

The narrative of using Fibonacci levels is one of blending mathematical precision with market psychology. By understanding and applying these levels, traders gain insights into potential support and resistance areas, improving their chances of making profitable trades. Like any tool, Fibonacci levels are most effective when combined with other forms of analysis and a thorough understanding of market dynamics.

Bitcoin Futures vs. Spot Tri-Frame - Strategy [presentTrading]Prove idea with a backtest is always true for trading.

I developed and open-sourced it as an educational material for crypto traders to understand that the futures and spot spread may be effective but not be as effective as they might think. It serves as an indicator of sentiment rather than a reliable predictor of market trends over certain periods. It is better suited for specific trading environments, which require further research.

█ Introduction and How it is Different

The "Bitcoin Futures vs. Spot Tri-Frame Strategy" utilizes three different timeframes to calculate the Z-Score of the spread between BTC futures and spot prices on Binance and OKX exchanges. The strategy executes long or short trades based on composite Z-Score conditions across the three timeframes.

The spread refers to the difference in price between BTC futures and BTC spot prices, calculated by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges.

BTCUSD 1D L/S Performance

█ Strategy, How It Works: Detailed Explanation

🔶 Calculation of the Spread

The spread is the difference in price between BTC futures and BTC spot prices. The strategy calculates the spread by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges. This spread serves as the primary metric for identifying trading opportunities.

Spread = Weighted Average Futures Price - Weighted Average Spot Price

🔶 Z-Score Calculation

The Z-Score measures how many standard deviations the current spread is from its historical mean. This is calculated for each timeframe as follows:

Spread Mean_tf = SMA(Spread_tf, longTermSMA)

Spread StdDev_tf = STDEV(Spread_tf, longTermSMA)

Z-Score_tf = (Spread_tf - Spread Mean_tf) / Spread StdDev_tf

Local performance

🔶 Composite Entry Conditions

The strategy triggers long and short entries based on composite Z-Score conditions across all three timeframes:

- Long Condition: All three Z-Scores must be greater than the long entry threshold.

Long Condition = (Z-Score_tf1 > zScoreLongEntryThreshold) and (Z-Score_tf2 > zScoreLongEntryThreshold) and (Z-Score_tf3 > zScoreLongEntryThreshold)

- Short Condition: All three Z-Scores must be less than the short entry threshold.

Short Condition = (Z-Score_tf1 < zScoreShortEntryThreshold) and (Z-Score_tf2 < zScoreShortEntryThreshold) and (Z-Score_tf3 < zScoreShortEntryThreshold)

█ Trade Direction

The strategy allows the user to specify the trading direction:

- Long: Only long trades are executed.

- Short: Only short trades are executed.

- Both: Both long and short trades are executed based on the Z-Score conditions.

█ Usage

The strategy can be applied to BTC or Crypto trading on major exchanges like Binance and OKX. By leveraging discrepancies between futures and spot prices, traders can exploit market inefficiencies. This strategy is suitable for traders who prefer a statistical approach and want to diversify their timeframes to validate signals.

█ Default Settings

- Input TF 1 (60 minutes): Sets the first timeframe for Z-Score calculation.

- Input TF 2 (120 minutes): Sets the second timeframe for Z-Score calculation.

- Input TF 3 (180 minutes): Sets the third timeframe for Z-Score calculation.

- Long Entry Z-Score Threshold (3): Defines the threshold above which a long trade is triggered.

- Short Entry Z-Score Threshold (-3): Defines the threshold below which a short trade is triggered.

- Long-Term SMA Period (100): The period used to calculate the simple moving average for the spread.

- Use Hold Days (true): Enables holding trades for a specified number of days.

- Hold Days (5): Number of days to hold the trade before exiting.

- TPSL Condition (None): Defines the conditions for taking profit and stop loss.

- Take Profit (%) (30.0): The percentage at which the trade will take profit.

- Stop Loss (%) (20.0): The percentage at which the trade will stop loss.

By fine-tuning these settings, traders can optimize the strategy to suit their risk tolerance and trading style, enhancing overall performance.

Dual RSI Differential - Strategy [presentTrading]█ Introduction and How it is Different

The Dual RSI Differential Strategy introduces a nuanced approach to market analysis and trading decisions by utilizing two Relative Strength Index (RSI) indicators calculated over different time periods. Unlike traditional strategies that employ a single RSI and may signal premature or delayed entries, this method leverages the differential between a shorter and a longer RSI. This approach pinpoints more precise entry and exit points, providing a refined tool for traders to exploit market conditions effectively, particularly in overbought and oversold scenarios.

Most important: it is a good eductional code for swing trading.

For beginners, this Pine Script provides a complete function that includes crucial elements such as holding days and the option to configure take profit/stop loss settings:

- Hold Days: This feature ensures that trades are not exited too hastily, helping traders to ride out short-term market volatility. It's particularly valuable for swing trading where maintaining positions slightly longer can lead to capturing significant trends.

- TPSL Condition (None by default): This setting allows traders to focus solely on the strategy's robust entry and exit signals without being constrained by preset profit or loss limits. This flexibility is crucial for learning to adjust strategy settings based on personal risk tolerance and market observations.

BTCUSD 6h LS Performance

█ Strategy, How It Works: Detailed Explanation

🔶 RSI Calculation:

The RSI is a momentum oscillator that measures the speed and change of price movements. It is calculated using the formula:

RSI = 100 - (100 / (1 + RS))

Where RS (Relative Strength) = Average Gain of up periods / Average Loss of down periods.

🔶 Dual RSI Setup:

This strategy involves two RSI indicators:

RSI_Short (RSI_21): Calculated over a short period (21 days).

RSI_Long (RSI_42): Calculated over a longer period (42 days).

Differential Calculation:

The strategy focuses on the differential between these two RSIs:

RSI Differential = RSI_Long - RSI_Short

This differential helps to identify when the shorter-term sentiment diverges from longer-term trends, signaling potential trading opportunities.

BTCUSD Local picuture

🔶 Signal Triggers:

Entry Signal: A buy (long) signal is triggered when the RSI Differential exceeds -5, suggesting strengthening short-term momentum. Conversely, a sell (short) signal occurs when the RSI Differential falls below +5, indicating weakening short-term momentum.

Exit Signal: Trades are generally exited when the RSI Differential reverses past these thresholds, indicating a potential momentum shift.

█ Trade Direction

This strategy accommodates various trading preferences by allowing selections among long, short, or both directions, thus enabling traders to capitalize on diverse market movements and volatility.

█ Usage

The Dual RSI Differential Strategy is particularly suited for:

Traders who prefer a systematic approach to capture market trends.

Those who seek to minimize risks associated with rapid and unexpected market movements.

Traders who value strategies that can be finely tuned to different market conditions.

█ Default Settings

- Trading Direction: Both — allows capturing of upward and downward market movements.

- Short RSI Period: 21 days — balances sensitivity to market movements.

- Long RSI Period: 42 days — smoothens out longer-term fluctuations to provide a clearer market trend.

- RSI Difference Level: 5 — minimizes false signals by setting a moderate threshold for action.

Use Hold Days: True — introduces a temporal element to trading strategy, holding positions to potentially enhance outcomes.

- Hold Days: 5 — ensures that trades are not exited too hastily, helping to ride out short-term volatility.

- TPSL Condition: None — enables traders to focus solely on the strategy's entry and exit signals without preset profit or loss limits.

- Take Profit Percentage: 15% — aims for significant market moves to lock in profits.

- Stop Loss Percentage: 10% — safeguards against large losses, essential for long-term capital preservation.

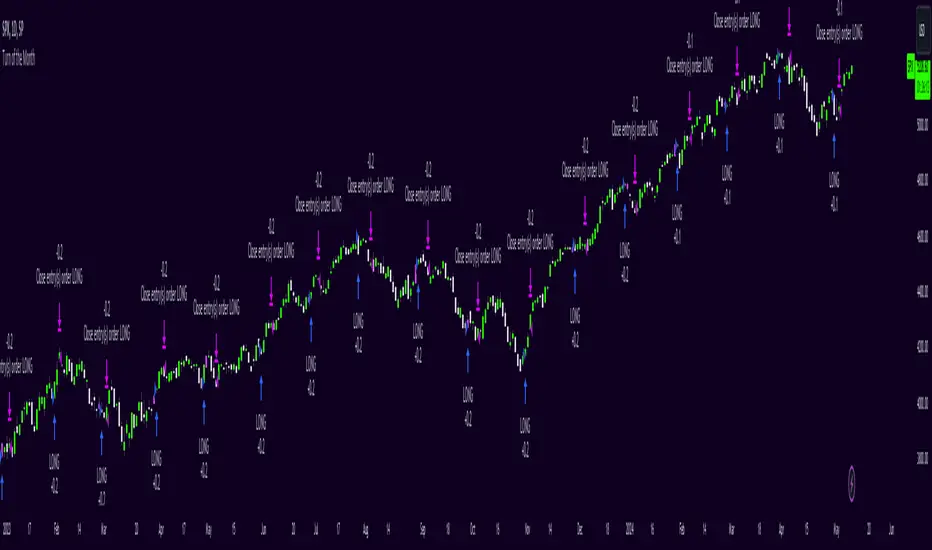

Turn of the Month Strategy [Honestcowboy]The end of month effect is a well known trading strategy in the stock market. Quite simply, most stocks go up at the end of the month. What's even better is that this effect spills over to the next phew days of the next month.

In this script we backtest this theory which should work especially well on SP500 pair.

By default the strategy buys 2 days before the end of each month and exits the position 3 days into the next month.

The strategy is a long only strategy and is extremely simple. The SP500 is one of the #1 assets people use for long term investing due to it's "9.8%" annualised return. However as a trader you want the best deal possible. This strategy is only inside the market for about 25% of the time while delivering a similar return per exposure with a lower drawdown.

Here are some hypothesis why turn of the month effect happens in the stock markets:

Increased inflow from savings accounts to stocks at end of month

Rebalancing of portfolios by fund managers at end of month

The timing of monthly cash flows received by pension funds, which are reinvested in the stock market.

The script also has some inputs to define how many days before end of the month you want to buy the asset and how long you want to hold it into the next month.

It is not possible to buy the asset exactly on this day every month as the market closes on the weekend. I've added some logic where it will check if that day is a friday, saturdady or sunday. If that is the case it will send the buy signal on the end of thursday, this way we enter on the friday and don't lose that months trading opportunity.

The backtest below uses 4% exposure per trade as to show the equity curve more clearly and because of publishing rules. However, most fund managers and investors use 100% exposure. This way you actually risk money to earn money. Feel free to adjust the settings to your risk profile to get a clearer picture of risks and rewards before implementing in your portfolio.

Alligator + MA Trend Catcher [TradeDots]The "Alligator + MA Trend Catcher" is a trading strategy that integrates the William Alligator indicator with a Moving Average (MA) to establish robust entry and exit conditions, optimized for capturing trends.

HOW IT WORKS

This strategy combines the traditional William Alligator set up with an additional Moving Average indicator for enhanced trend confirmation, creating a user-friendly backtesting tool for traders who prefer the Alligator method.

The original Alligator strategy can frequently present fluctuations, even in well-established trends, leading to potentially premature exits. To mitigate this, we incorporate a Moving Average as a secondary confirmation measure to ensure the market trend has indeed shifted.

Here’s the operational flow for long orders:

Entry Signal: When the price rises above the Moving Average, it confirms a bullish market state. Enter if Alligator spread in an upward direction. The trade remains active even if the Alligator indicator suggests a trend reversal.

Exit Signal: The position is closed when the price falls below the Moving Average, and the Alligator spreads in the downward direction. This setup helps traders to maintain positions through the entirety of the trend for maximum gain.

APPLICATION

This strategy is tailored for assets with significant, well-defined trends, such as Bitcoin and Ethereum, which are known for their high volatility and substantial price movements.

This strategy offers a low win-rate but high reward configuration, making asset selection critical for long-term profitability. If you choose assets that lack strong price momentum, there's a high chance that this strategy may not be effective.

For traders seeking to maximize gains from large trends without exiting prematurely, this strategy provides an aggressive yet controlled approach to riding out substantial market waves.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Khaled Tamim's Avellaneda-Stoikov StrategyDescription:

This strategy applies the Avellaneda-Stoikov (A-S) model to generate buy and sell signals for underlying assets based on option pricing theory. The A-S model estimates bid and ask quotes for options contracts considering factors like volatility (sigma), time to expiration (T), and risk aversion (gamma).

Key Concepts:

Avellaneda-Stoikov Model: A mathematical framework for option pricing that incorporates volatility, time decay, and risk tolerance.

Bid-Ask Quotes: The theoretical buy and sell prices for an option contract.

Inventory Management: The strategy tracks its long or short position based on signals.

How it Works:

A-S Model Calculation: The avellanedaStoikov function calculates bid and ask quotes using the underlying asset's closing price, user-defined parameters (gamma, sigma, T, k, and M), and a small fee (adjustable).

Signal Generation: The strategy generates long signals when the closing price falls below the adjusted bid quote and short signals when it exceeds the adjusted ask quote.

Trade Execution: Buy and sell orders are triggered based on the generated signals (long for buy, short for sell).

Inventory Tracking: The strategy's net profit reflects the current inventory level (long or short position).

Customization:

Gamma (γ): Controls risk aversion in the A-S model (higher values imply lower risk tolerance).

Sigma (σ): Represents the underlying asset's expected volatility.

T: Time to expiration for the hypothetical option (defaults to a short-term option).

k: A constant factor in the A-S model calculations.

M: Minimum price buffer for buy/sell signals (prevents excessive churn).

Important Note:

This strategy simulates option pricing behavior for a theoretical option and does not directly trade options contracts. Backtesting results may not reflect actual market conditions.

Further Considerations:

The 0.1% fee is a placeholder and may need adjustment based on real-world trading costs.

Consider using realistic timeframes for T (e.g., expiry for a real option)

Disclaimer: This strategy is for educational purposes only and does not constitute financial advice.

Volume-Supported Linear Regression Trend Modified StrategyHi everyone, this will be my first published script on Tradingview, maybe more to come.

For quite some time I have been looking for a script that performs no matter if price goes up or down or sideways. I believe this strategy comes pretty close to that. Although nowhere near the so called "buy&hold equity" of BTC, it has produced consistent profits even when price goes down.

It is a strategy which seems to work best on the 1H timeframe for cryptocurrencies.

Just by testing different settings for SL and TP you can customize it for each pair.

THE STRATEGY:

Basically, I used the Volume Supported Linear Regression Trend Model that LonesomeTheBlue has created and modified a few things such as entry and exit conditions. So all credits go to him!

LONG ENTRY: When there is a bullish cross of the short term trend (the histogram/columns), while the long term trend is above 0 and rising.

SHORT ENTRY: When there is a bearish cross (green to red) of the short-term trend (the histogram/columns), while the long term trend is beneath 0 and decreasing.

LONG EXIT: Bearish crossover of short-term trend while long term trend is below 0

SHORT EXIT: Bullish crossover of short-term trend while long term trend is above 0

Combining this with e.g. a SL of 2% and a TP of 20% (as used in my backtesting), combined with pyramiding and correct risk management, it gives pretty consistent results.

Be aware, this is only for educational purpose and in no means financial advise. Past results do not guarantee future results. This strategy can lose money!

Enjoy :)

PS: It works not only on BTC of course, works even better on some other major crypto pairs. I'll leave it to you to find out which ones ;)

Fibonacci Trend Reversal StrategyIntroduction

This publication introduces the " Fibonacci Retracement Trend Reversal Strategy, " tailored for traders aiming to leverage shifts in market momentum through advanced trend analysis and risk management techniques. This strategy is designed to pinpoint potential reversal points, optimizing trading opportunities.

Overview

The strategy leverages Fibonacci retracement levels derived from @IMBA_TRADER's lance Algo to identify potential trend reversals. It's further enhanced by a method called " Trend Strength Over Time " (TSOT) (by @federalTacos5392b), which utilizes percentile rankings of price action to measure trend strength. This also has implemented Dynamic SL finder by utilizing @veryfid's ATR Stoploss Finder which works pretty well

Indicators:

Fibonacci Retracement Levels : Identifies critical reversal zones at 23.6%, 50%, and 78.6% levels.

TSOT (Trend Strength Over Time) : Employs percentile rankings across various timeframes to gauge the strength and direction of trends, aiding in the confirmation of Fibonacci-based signals.

ATR (Average True Range) : Implements dynamic stop-loss settings for both long and short positions, enhancing trade security.

Strategy Settings :

- Sensitivity: Set default at 18, adjustable for more frequent or sparse signals based on market volatility.

- ATR Stop Loss Finder: Multiplier set at 3.5, applying the ATR value to determine stop losses dynamically.

- ATR Length: Default set to 14 with RMA smoothing.

- TSOT Settings: Hard-coded to identify percentile ranks, with no user-adjustable inputs due to its intrinsic calculation method.

Trade Direction Options : Configurable to support long, short, or both directions, adaptable to the trader's market assessment.

Entry Conditions :

- Long Entry: Triggered when the price surpasses the mid Fibonacci level (50%) with a bullish TSOT signal.

- Short Entry: Activated when the price falls below the mid Fibonacci level with a bearish TSOT indication.

Exit Conditions :

- Employs ATR-based dynamic stop losses, calibrated according to current market volatility, ensuring effective risk management.

Strategy Execution :

- Risk Management: Features adjustable risk-reward settings and enables partial take profits by default to systematically secure gains.

- Position Reversal: Includes an option to reverse positions based on new TSOT signals, improving the strategy's responsiveness to evolving market conditions.

The strategy is optimized for the BYBIT:WIFUSDT.P market on a scalping (5-minute) timeframe, using the default settings outlined above.

I spent a lot of time creating the dynamic exit strategies for partially taking profits and reversing positions so please make use of those and feel free to adjust the settings, tool tips are also provided.

For Developers: this is published as open-sourced code so that developers can learn something especially on dynamic exits and partial take profits!

Good Luck!

Disclaimer

This strategy is shared for educational purposes and must be thoroughly tested under diverse market conditions. Past performance does not guarantee future results. Traders are advised to integrate this strategy with other analytical tools and tailor it to specific market scenarios. I was only sharing what I've crafted while strategizing over a Solana Meme Coin.

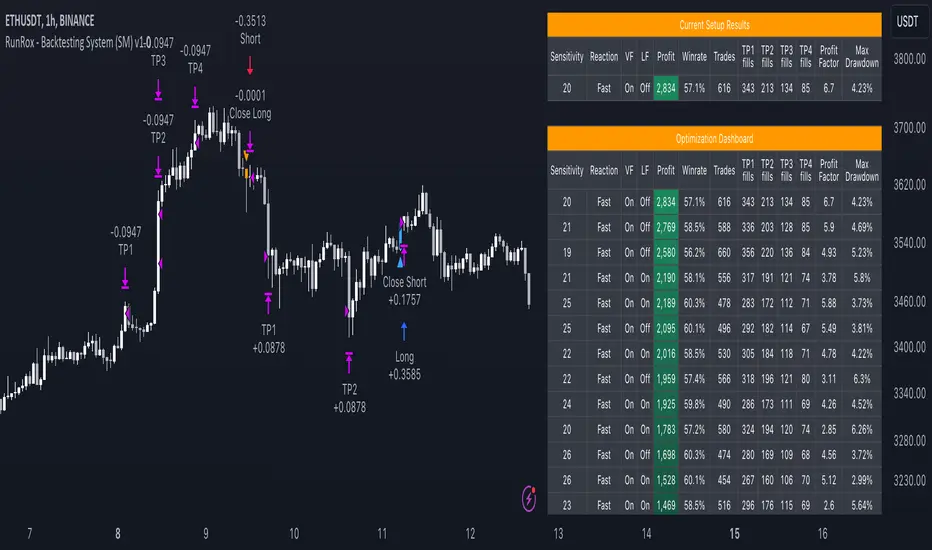

RunRox - Backtesting System (SM)RunRox - Backtesting System (SM) is designed for flexible and comprehensive testing of trading strategies, closely integrated with our RunRox - Signals Master indicator. This combination enhances your ability to refine strategies efficiently, providing you with insights to adapt and optimize your trading tactics seamlessly.

The Backtesting System (SM) excels in pinpointing the optimal settings for the RunRox - Signals Master indicator, efficiently highlighting the most effective configurations.

Capabilities of the Backtesting System (SM)

Optimal Settings Determination: Identifies the best configurations for the Signals Master indicator to enhance its effectiveness.

Timeframe-Specific Strategy Testing: Allows strategies to be tested over specific historical time periods to assess their viability.

Customizable Initial Conditions: Enables setting of initial deposit, risk per trade, and commission rates to mirror real-world trading conditions.

Flexible Money Management: Provides options to set take profits and stop losses, optimizing potential returns and risk management.

Intuitive Dashboard: Features a user-friendly dashboard that visually displays all pertinent information, making it easy to analyze and adjust strategies.

Trading Flexibility Across Three Modes:

Dual-Direction Trading: Engage in both buying and selling with this mode. Our dashboard optimizes and identifies the best settings for trading in two directions, streamlining the process to maximize effectiveness for both buy and sell orders.

Buy-Only Mode: Tailored for traders focusing exclusively on purchasing assets. In this mode, our backtester pinpoints the most advantageous sensitivity, speed reaction, and filter settings specifically for buying. Optimal settings in this mode may differ from those used in dual-direction trading, providing a customized approach to single-direction strategies.

Sell-Only Mode: Perfect for strategies primarily based on selling. This setting allows you to discover the ideal configurations for asset sales, which can be particularly useful if you are looking for optimal exit points in long-term transactions or under specific market conditions.

Here's an example of how profits can differ on the same asset when trading using two distinct strategies: exclusively buying or trading in both directions.

Above in the image, you can see how one-directional trading influences the results of backtests on historical data. While this does not guarantee future outcomes, it provides insight into how the strategy's performance can vary with different trading directions.

As you can also see from the image, one-directional trading has affected the optimal combination of settings for Sensitivity, Speed Reaction, and Filters.

Stop Loss and Take Profit

Our backtesting system, as you might have gathered, includes flexible settings for take profits and stop losses. Here are the main features:

Multiple Take Profits: Ability to set from 1 to 4 take profit levels.

Fixed Percentage: Option to assign a fixed percentage for each take profit.

Trade Proportion Fixation: Ability to set a fixed size from the trade for securing profits.

Stop Loss Installation: Option to establish a stop loss.

Break-Even Stop Loss: Ability to move the stop loss to a break-even point upon reaching a specified take profit level.

These settings offer extensive flexibility and can be customized according to your preferences and trading style. They are suitable for both novice and professional traders looking to test their trading strategies on historical data.

As illustrated in the image above, we have implemented money management by setting fixed take profits and stop losses. Utilizing money management has improved indicators such as profit, maximum drawdown, and profit factor, turning even historically unprofitable strategies into profitable ones. Although this does not guarantee future results, it serves as a valuable tool for understanding the effectiveness of money management.

Additionally, as you can see, the optimal settings for Signals Master have been adjusted, highlighting the best configurations for the most favorable outcomes.

Disclaimer:

Historical data is not indicative of future results. All indicators and strategies provided by RunRox are intended for integration with traders' strategies and should be used as tools for analysis rather than standalone solutions. Traders should use their own discretion and understand that all trading involves risk.

Strategy - Plus / Connectable [Azullian]Discover the advanced capabilities of Strategy Plus, an essential component of the connectable indicator system designed for fast-paced strategy testing, visualization, and building within TradingView. This enhanced version of our foundational connectable strategy indicator seamlessly integrates with all connectable indicators . By utilizing the TradingView input source as a signal connector , it facilitates the linking of indicators to form a cohesive strategy. Each connectable indicator within the system sends signal weight to the next node, culminating in a comprehensive strategy that incorporates advanced customization options, sophisticated signal interpretation, and elaborate backtest labeling. Strategy Plus stands out by offering improved position management and extensive alert messaging capabilities, ensuring effective strategy refinement and backend integration.

█ DISTINCTIVE FEATURES

The Connectable Strategy Plus enhances risk mitigation within the connectable system through its advanced features and capabilities:

• Refined Signal Input Management: Tailor and precisely connect up to two signal filters with enhanced input flexibility, gain control, and strategic direction settings.

• Strategic Position Investment Control: Optimize positioning with versatile investment bases, custom investment percentages, and direction-specific investments for effective risk management.

• Advanced Exit Stop Loss Configuration: Implement custom stop loss tactics with diverse base modes and trailing options for tailored risk management.

• Strategic Exit Take Profit Settings: Apply precision-driven take profit strategies with various calculation modes and dynamic trailing functionality.

• Calibrated Entry Position Allocation: Optimize investment distribution for entry positions, including DCA and BRO trades, for strategic market response.

• Refined Order Setting Customization: Ensure exchange compliance with adjustable order settings, enhancing backtest accuracy and strategy reliability.

• Comprehensive Condition Settings: Define precise conditions for strategy execution, including date range filtering and order/loss limitations.

• Intuitive Visualization: Enhance strategy clarity with customizable visual elements and trade visualization features.

• Advanced Alert Configurations: Stay informed with comprehensive and customizable alerts for effective backend integration.

• Backend Integration With JSON Format: Leverage elaborate and structured data in JSON format for advanced analytics, enhancing decision-making and strategy optimization outside TradingView.

Let's review the separate parts of this indicator.

█ STRATEGY INPUTS

We've provided 2 inputs for connecting a signal filter or indicators or chains (1→, 2→) which are all set to 'Close' by default.

An input has several controls:

• Enable disable: Toggle the entire input on or off

• Input: Connect indicators or signal filter here, choose indicators with a compatible : Signal connector.

• G - Gain: Increase or reduce the strength of the incoming signal by a factor.

• SM - Signal Mode: Choose a trading direction compatible with the settings in your signal filter

• XM - Exit Mode: Determine when to allow to exit your open trade

○ Always: Doesn't take the restrictions into account, this ignores all the settings chosen in ML or MP

○ Restricted: Use both ML and MP conditions

○ Loss: Use the ML condition only, for example: Position will be exited and the exit signal will be allowed only when the loss exceeds the ML parameter

○ Profit: Use the MP condition only for example: Exits will only be allowed when the profit of the position exceeds the condition of the MP parameter

█ POSITION INVESTMENT

Determine the percentage of your trading budget you would like to use in each position based on the strategy's profit or loss.

• LINVB - Loss Investment Base: Choose which base to use to determine the investment percentage when the strategy is in a loss.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• LINV% - Loss Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in loss, and a initial capital of $100, and the investment base is set to equity with a percentage of 50%, your investment will be 50% of $90, $45.

• PINVB - Profit Investment Base: Choose which base to use to determine the investment percentage when the strategy is in profit.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• PINV% - Profit Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in profit, and an initial capital of $100, and the investment base is set to equity with a percentage of 100%, your investment will be 100% of $110, $110.

• XINVB - Custom Profit Investment Base: Choose which base to use to determine the investment percentage when the strategy is above a custom profit threshold (XT).

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• XINV% - Custom Profit Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 100% in profit, exceeding the XT threshold of 50%, and an initial capital of $100, and the investment base is set to equity with a percentage of 50%, your investment will be 50% of $200, $100.

• XT% - Custom Profit Threshold: Determine how much profit triggers these custom profit investment settings.

• ELIB% - Entry Long Investment Base: Following previous settings, you can further restrict the investment according to the long trading direction.

○ For instance, if the previous calculation resulted in $45 to be used as an investment, and you've set the ELIB% to 50%, your long position will use 50% of $45, which is $22.5.

• ESIB% - Entry Short Investment Base: Following previous settings, you can further restrict the investment according to the short trading direction.

○ For example, if the previous calculation resulted in $45 to be used as an investment, and you've set the ESIB% to 50%, your short position will use 50% of $45, which is $22.5.

• RISK% - Risk Percentage:

○ Determine how much of the calculated position investment is at risk when the stop-loss is hit.

- For example, 1% of $45 represents a maximum loss of $0.45.

○ Risk percentage works together with the stop loss and the max leverage.

• MXLVG - Maximum Leverage:

○ Investigate the trading rules for your trading pair and use the maximum allowed amount of leverage.

○ To determine the number of contracts to be bought or sold, considering the stop loss and the specified risk percentage, the maximum leverage available will constrain the amount of leverage utilized to ensure that the maximum risk threshold is not exceeded. For instance, suppose the stop loss is set at 1%, and the risk percentage is defined as 10%. Initially, the calculated leverage to be used would be 10. However, if there is a maximum leverage cap set at 5, it would constrain the calculated leverage of 10 to adhere to the maximum limit of 5.

█ EXIT STOP LOSS

Determine the Stop Loss price based on your selected configuration.

As the stop loss is an integral part of the ordered contracts calculation used in conjunction with the Risk and Max leverage, you'll always need to provide a stop loss price.

• SLLB - Stop Loss Long Base: Choose a stop loss mode for calculating stop loss prices in long positions.

○ Risk: Determines the price using the Risk parameter (RISK%) and maximum leverage (MXLVG). In this case, SLLB% will not have any impact.

○ Price Entry + Offset: Calculates the stop loss price based on a offset percentage (SLLB%) from the entry price of the position.

○ Source: Computes the stop loss price based on an external indicator defined in SLLSRC.

- If this results in an invalid price, the calculation will revert to using the price entry + offset.

○ Source + Offset: Determines the stop loss price based on a positive or negative offset percentage (SLLB%) from an external indicator defined in SLLSRC.

- If this results in an invalid price, the calculation will fall back to using the price entry + offset.

• SLLB% - Stop Loss Long Base Percentage: Define an offset percentage that will be applied in the price entry + offset and source + offset stop loss modes.

• SLLSRC - Stop Loss Long Source: Connect an external indicator as the source for stop loss (only those providing price values eg: bollinger bands, moving averages...).

• SLLT - Stop Loss Long Trailing:

○ Fixed: The initial stop loss will be kept and no trailing stop loss will be applied.

○ Trail Stop: Takes into account all settings defined in SLLB and SLLB% and recalculates them with each candle.

- If a better stop loss is computed, it replaces the existing stop loss. In this mode SLLT% will be disregarded.

○ Trail Stop till BE: Similar to trailing stop mode, but it stops trailing when the stop loss reaches the break-even point.

○ Trail Stop from BE: Similar to trailing stop mode, but it starts trailing when the stop loss reaches the break-even point.

○ Trail Price: Computes the trailing stop loss price based on an offset percentage (SLLT%) from the closing price of the current candle.

- If a better stop loss price is calculated, it will be set as the new stop loss price.

○ Trail Price till BE: Similar to the Trail Price mode, but it stops trailing when the stop loss reaches the break-even point.

○ Trail Price from BE: Similar to Trail Price mode, but it starts trailing when the stop loss reaches the break-even point.

○ Trail Incr: Adapts the trailing stop loss price based on the offset percentage (SLLT%).

- Each price change in favor of your position will incrementally adapt the trailing stop loss with SLLT%.

○ Trail Incr till BE: Similar to the Trail Incr mode, but it stops trailing when the stop loss reaches the break-even point.

• SLLT% - Stop Loss Long Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

• SLSB - Stop Loss Short Base: Functions similarly to SLLB but for short positions.

• SLSB% - Stop Loss Short Base Percentage: Functions similarly to SLLB% but for short positions.

• SLSSRC - Stop Loss Short Source: Functions similarly to SLLSRC but for short positions.

• SLST - Stop Loss Short Trailing: Functions similarly to SLLT but for short positions.

• SLST% - Stop Loss Short Trailing Percentage: Functions similarly to SLLT% but for short positions.

█ EXIT TAKE PROFIT

Determine the Take Profit price based on your selected configuration.

• TPLB - Take Profit Long Base: Choose a take profit mode for calculating take profit prices in long positions.

○ Reward: Determines the take profit price using the Risk parameter (RISK%) and the calculated Stop Loss price and the set reward percentage (TPLB%).

- For example: Risk 1%, Calculated Stop loss price: $90, Entry price: $100, Reward (TPLB%): 2%, will result in a take profit price on $120.

○ Price Entry + Offset: Calculates the take profit price based on a offset percentage (TPLB%) from the entry price of the position.

- For example: Entry price: $100, Offset (TPLB%): 2%, will result in a take profit price on $102.

○ Source: Computes the take profit price based on an external input from another indicator defined in TPLSRC.

- If this results in an invalid price, the calculation will revert to using the price entry + offset.

○ Source + Offset: Determines the take profit price based on a positive or negative offset percentage (TPLB%) from an external indicator inpuy defined in TPLSRC.

- If this results in an invalid price, the calculation will fall back to using the price entry + offset.

• TPLB% - Take Profit Long Base Percentage: Define an offset percentage that will be applied in the price entry + offset and source + offset take profit modes.

• TPLSRC - Take Profit Long Source: Choose to connect an external indicator as the source for take profit (of course only those which provide price values eg: bollinger bands, moving averages... but not oscillators).

• TPLT - Take Profit Long Trailing:

○ Fixed: The initial take profit will be kept and no trailing take profit will be applied.

○ Trail Profit: Takes into account all settings defined in TPLB and TPLB% and recalculates them with each candle.

- If an applicable take profit is computed, it replaces the existing take profit. In this mode TPLT% will be disregarded.

○ Trail Profit till BE: Similar to trailing profit mode, but it stops trailing when the take profit reaches the break-even point.

○ Trail Profit from BE: Similar to trailing profit mode, but it starts trailing when the take profit reaches the break-even point.

○ Trail Price: Computes the trailing take profit price based on an offset percentage (TPLT%) from the closing price of the current candle.

- If an applicable take profit price is calculated, it will be set as the new take profit price.

○ Trail Price till BE: Similar to the Trail Price mode, but it stops trailing when the take profit reaches the break-even point.

○ Trail Price from BE: Similar to Trail Price mode, but it starts trailing when the take profit reaches the break-even point.

○ Trail Incr: Adapts the trailing take profit price based on the offset percentage (TPLT%). Each price change against your position will incrementally adapt the trailing take profit with TPLT%.

○ Trail Incr till BE: Similar to the Trail Incr mode, but it stops trailing when the take profit reaches the break-even point.

• TPLT% - Take Profit Long Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

• TPSB - Take Profit Short Base: Functions similarly to TPLB but for short positions.

• TPSB% - Take Profit Short Base Percentage: Functions similarly to TPLB% but for short positions.

• TPSSRC - Take Profit Short Source: Functions similarly to TPLSRC but for short positions.

• TPST - Take Profit Short Trailing: Functions similarly to TPLT but for short positions.

• TPST% - Take Profit Short Trailing Percentage: Functions similarly to TPLT% but for short positions.

█ ENTRY INVESTMENT DISTRIBUTION

Based on your position investment calculation you can distribute the position investment accross the initial opening trade of the position (SIG%) or the follow up Dollar Cost Averaging (DCA%) or Break Out (BRO%) trades.

For example: SIG%: 10%, DCA%: 45%, BRO%: 45% and the calculated Position Investment is $100, then the initial trade will receive $10, DCA will receive $45, and BRO will receive $45 to work with. Disable BRO and or DCA by setting them to 0%. Keep in mind that the sum of SIG, BRO and DCA may not exceed 100%.

• SIG% - Initial order investment percentage based on the signal: The percentage of the position investment distributed over normal trades.

• DCA% - Dollar Cost Averaging investment percentage: The percentage of the position investment distributed to DCA trades.

• BRO% - Break Out investment percentage: The percentage of the position investment distributed to BRO trades.

█ ENTRY DCA

DCA (Dollar-Cost Averaging) is a risk mitigation strategy where the allocated DCA% budget from the Entry Investment Distribution is distributed among x levels (DCA#) based on calculated prices (DPLM) and order sizes (DOSM), when prices move against your position.

• DCA# - Maximum DCA levels: Set the maximum number of DCA levels.

• DPLM - DCA Price Level Mode: Choose a price level mode that determines at which prices the additional purchases are distributed:

○ Linear: Entry prices are evenly spaced at regular intervals.

○ QuadIn: Entry prices are front-loaded, with more at the beginning and fewer later.

○ QuadOut: Entry prices are back-loaded, with fewer at the beginning and more later.

○ QuadInOut: Entry prices start front-loaded, then become back-loaded.

○ CubicIn: Similar to QuadIn but with a smoother front-loaded distribution.

○ CubicOut: Similar to QuadOut but with a smoother back-loaded distribution.

○ ExpoIn: Entry prices are exponentially increasing, starting small and growing.

○ ExpoOut: Entry prices are exponentially decreasing, starting large and reducing.

○ ExpoInOut: Entry prices start exponentially increasing, then decrease exponentially.

• DOSM - DCA Order Size Mode: Choose a DCA budget distribution mode for order sizes:

○ Linear: Order sizes are evenly spaced at regular intervals.

○ QuadIn: Order sizes are front-loaded, with larger orders at the beginning and smaller ones later.

○ QuadOut: Order sizes are back-loaded, with smaller orders at the beginning and larger ones later.

○ QuadInOut: Order sizes start front-loaded and transition to back-loaded.

○ CubicIn: Similar to QuadIn but with a smoother front-loaded distribution of order sizes.

○ CubicOut: Similar to QuadOut but with a smoother back-loaded distribution of order sizes.

○ ExpoIn: Order sizes exponentially increase, starting small and growing.

○ ExpoOut: Order sizes exponentially decrease, starting large and reducing.

○ ExpoInOut: Order sizes start exponentially increasing, then decrease exponentially.

For a visual representation of the price or order size distribution modes, refer to online easing curves.

█ ENTRY BRO

BRO (Break Out) is a risk mitigation strategy where the allocated BRO% budget from the Entry Investment Distribution is distributed among x levels (BRO#) based on calculated prices (BPLM) and order sizes (BOSM), when prices move in favor of your position.

• BRO# - Maximum BRO levels: Set the maximum number of BRO levels.

• BPLM - BRO Price Level Mode: Choose a price level mode that determines at which prices the additional purchases are distributed:

○ Distribution easing modes work similar as the DCA easing modes.

• BOSM - BRO Order Size Mode: Choose a BRO budget distribution mode for order sizes:

○ Distribution easing modes work similar as the DCA easing modes.

█ ORDER SETTINGS

Fine-tune accuracy to match your exchange's trading constraints, enhancing backtest precision with these settings, default settings are least restrictive for crypto trading pairs.

• MINP - Mininmum Position Notional Value: Exchange-defined minimum notional value for positions:

○ Calculated based on your exchange's rules and is the minimum total value your position must hold to meet their requirements It is calculated by multiplying Quantity with price and leverage.

○ It helps ensure your trades align with your exchange's standards.

• MAXP - Maximum Position Notional Value: Exchange-defined maximum notional value for positions:

○ Similar to MINP, this value is calculated based on your exchange's rules and represents the maximum total value allowed for your position.

• MINQ - Mininmum Order Quantity: Least permissible order quantity based on exchange rules:

○ This is the smallest quantity of an asset that your exchange allows you to trade in a single order.

• MAXQ - Maximum Order Quantity: Highest permissible order quantity according to exchange rules:

○ Opposite of MINQ, this is the largest quantity of an asset you can trade in a single order as defined by your exchange.

• DECP - Decimals in Order Price: Allowed decimal places in order prices as per exchange specifications:

○ This value specifies the number of decimal places you can use when specifying the price of an order.

• DECQ - Decimals in Order Quantity: Permitted decimal places in order quantities according to exchange specifications:

○ Similar to DECP, this value indicates the number of decimal places you can use when specifying the quantity of an asset in an order.

█ STRATEGY CONDITIONS

Specify when the strategy is permitted to execute trades.

• DATE: Enable the Date Range filter to restrict entries to a specific date range.

○ START: Set a start date and hour to commence trading.

○ END: Set an end date and hour to conclude trading within the defined range.

• IDO - Maximum Intraday Orders: Limit the number of orders the strategy can place within a single trading day. Upon reaching this limit, the strategy temporarily halts further entries for the day.

• DL% - Maximum Intraday Loss%: Set a threshold for the maximum allowable intraday loss as a percentage of equity. When exceeded, the strategy temporarily suspends trading for the day.

• CLD - Maximum Consecutive Loss Days: Define the maximum number of consecutive days the strategy can incur losses. Upon reaching this limit, the strategy halts trading and avoids new entries.

• DD% - Maximum Drawdown: Specify the maximum permissible drawdown as a percentage of equity. If this limit is met, the strategy halts trading and refrains from placing additional entries.

• TP% - Total Profit %: Establish a target for the total profit percentage the strategy aims to achieve. Once this target is attained, the strategy halts trading and refrains from initiating new entries.

• TL% - Total Loss %: Define a limit for the total loss percentage relative to the initial capital. If this limit is exceeded, the strategy discontinues trading and refrains from placing further entries.

■ VISUALS

• LINE: Activate a colored dashed diagonal line to visually connect the entry and exit points of positions.

• SLTP: Enable visualization of stop loss, take profit, and break-even levels.

• PNL: Enable Break-Even and Close Lines along with a colored area in between to visualize profit and loss.

• ☼: Brightness % : Adjust the opacity of the plotted trading visuals.

• P - Profit Color : Choose the color for profit-related elements.

• L - Loss Color: Choose the color for loss-related elements.

• B - Breakeven Color : Select the color for break-even points.

• EL - Long Color: Specify the color for long positions.

• ES - Short Color: Specify the color for short positions.

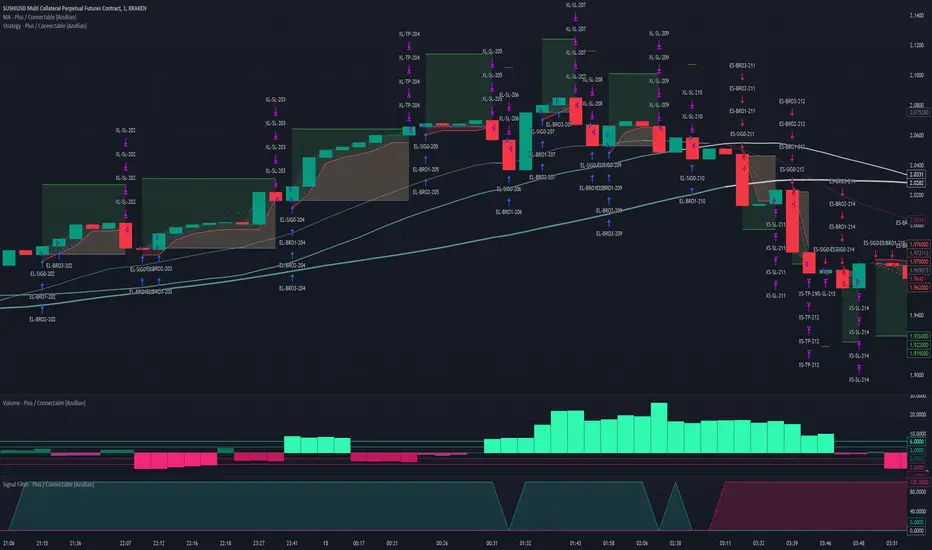

• TRADE LABELING: For better analysis we've labeled all entries and exits conform with the type of order your strategy has executed, some examples:

○ EL-SIG0-124: Enter Long - Signal 0 - Position 124

○ EL-BRO1-130: Enter Long - BRO1 - Position 130

○ EL-BRO2-130: Enter Long - BRO2 - Position 130

○ ES-DCA1-140: Enter Short - DCA1 - Position 140

○ XS-DCA2-140: Exit Short - DCA2 - Position 140

○ XL-TP-150: Exit Long - Take Profit - Position 150

○ XS-TP-154: Exit Short - Take Profit - Position 154

○ XL-SL-160: Exit Long - Stop Loss - Position 160

○ XS-SL-164: Exit Short - Stop Loss - Position 164

○ XS-CND-165: Exit Short - Strategy Condition - Max intraday loss - Position 165

■ ALERT SETTINGS

For developers and those who wish to integrate TradingView alerts into their backend systems, we offer comprehensive labeling options.

• ALID: A unique identifier you've assigned to your alert.

• NAME: A structured name you've given to this strategy.

• LAYOUT: The layout key of the strategy, allowing direct chart linking from your backend.

• SYMBOL: The symbol on which the strategy operates.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• TICK: The ticker for the strategy.

• CHART: The chart parameter containing the timeframe.period and timeframe.multiplier.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• BAR: Includes bar information in the alert message.

• STRATEGY: Adds strategy inputs to the alert message.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• PERFORMANCE: Incorporates strategy performance data into the alert message.

• SIGNAL: Appends received signal weights (EL, XL, ES, XS) to the alert message.

• ORDERS: Includes order details in the alert message.

• TAGS: Adds up to 6 tags and their corresponding values to the alert message.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

Of course we can't neglect letting you in on how this juicy JSON would look (without the // comments):

{

"id": 20726, // Message Id

"t": "2023-11-01T10:35:00Z", // Message Time

"al": { // Alert

"id": "639bfa9a-5f01-4031-8880-7ec01e972055", // Alert Id

"n": "TEST04", // Name

"l": "ABC123" // Layout

},

"sym": { // Symbol

"typ": "crypto", // Type

"r": "DOGEUSD.PM", // Root

"pre": "KRAKEN", // Prefix

"tc": "DOGEUSD.PM", // Ticker

"bc": "DOGE", // BaseCurrency

"c": "USD", // Currency

"d": "DOGEUSD Multi Collateral Perpetual Futures Contract", // Description

"mtc": 0.000001, // MinTick

"pv": 1, // PointValue

"ct": "PF_DOGEUSD" // CustomTicker

},

"ch": { // Chart

"pd": "1", // Period

"mul": 1 // Multiplier

},

"bar": { // Bar

"id": 20725, // Index

"t": "2023-11-01T10:33:00Z", // Time

"o": 0.066799, // Open

"h": 0.066799, // High

"l": 0.066799, // Low

"c": 0.066799, // Close

"v": 2924 // Vol

},

"strat": { // Strategy

"n": "Strategy - Plus / Connectable ", // Name

"sig": { // Signal

"c1e": true, // Connector1Enabled

"c1s": 500500.500501, // Connector1Source

"c1g": 1, // Connector1Gain

"c2e": false, // Connector2Enabled

"c2s": 0.067043, // Connector2Source

"c2g": 1, // Connector2Gain

"sm": "Swing (EL, ES)", // SignalMode

"xm": "Always", // ExitMode

"mlp": 0.01, // ExitModeMinPercLoss

"mpp": 0.01 // ExitModeMinPercProfit

},

"inv": { // Investment

"lb": "Equity", // LossBase

"lp": 50, // LossPerc

"pb": "Equity", // ProfitBase

"pp": 100, // ProfitPerc

"pcb": "Equity", // ProfitCustomBase

"pcp": 100, // ProfitCustomPerc

"pct": 10000, // ProfitCustomThreshold

"elp": 100, // LongPerc

"esp": 100, // ShortPerc

"rsk": 1, // MaxRisk

"lvg": 10 // MaxLeverage

},

"sl": { // StopLoss

"lb": "Price Entry + Offset", // LongBase

"lp": 0.2, // LongPerc

"lsrc": 0.067043, // LongSource

"lt": "Trail Stop", // LongTrailMode

"ltp": 0.2, // LongTrailPerc

"sb": "Price Entry + Offset", // ShortBase

"sp": 0.2, // ShortPerc

"ssrc": 0.067043, // ShortSource

"st": "Trail Stop", // ShortTrailMode

"stp": 0.2 // ShortTrailPerc

},

"tp": { // TakeProfit

"lb": "Price Entry + Offset", // LongBase

"lp": 1, // LongPerc

"lsrc": 0.067043, // LongSource

"lt": "Fixed", // LongTrailMode

"ltp": 1, // LongTrailPerc

"sb": "Price Entry + Offset", // ShortBase

"sp": 1, // ShortPerc

"ssrc": 0.067043, // ShortSource

"st": "Fixed", // ShortTrailMode

"stp": 1 // ShortTrailPerc

},

"dis": { // Distribution

"sigp": 10, // SignalPerc

"dcap": 0, // DCAPerc

"brop": 90 // BROPerc

},

"dca": { // DCA

"lvl": 3, // Levels

"pl": "linear", // ModePriceLevel

"os": "linear" // ModeOrderSize

},

"bro": { // BRO

"lvl": 3, // Levels

"pl": "expoIn", // ModePriceLevel

"os": "cubicOut" // ModeOrderSize

},

"ord": { // OrderSettings

"pmin": 5, // PNVMin

"pmax": 30000000, // PNVMax

"qmin": 0, // QtyMin

"qmax": 1000000000, // QtyMax

"dp": 6, // DecPrice

"dq": 6 // DecQty

},

"cnd": { // Conditions

"de": true, // DateRangeEnabled

"start": "2023-11-01T10:30:00Z", // StartTime

"end": "2024-12-31T23:30:00Z", // EndTime

"idoe": false, // MaxIntradayOrdersEnabled

"ido": 100, // MaxIntradayOrders

"dle": false, // MaxIntradayLossEnabled

"dl": 10, // MaxIntradayLossPerc

"clde": false, // MaxConsLossDaysEnabled

"cld": false, // MaxConsLossDays

"dde": false, // MaxDrawdownEnabled

"dd": 100, // MaxDrawdownPerc

"mpe": false, // MaxProfitEnabled

"mp": 200, // MaxProfitPerc

"mle": false, // MaxLossEnabled

"ml": -50 // MaxLossPerc

}

},

"perf": { // Performance

"ic": 1000, // InitialCapital

"eq": 1000, // Equity

"np": 0, // NetProfit

"op": 0, // OpenProfit

"ct": 0, // ClosedTrades

"ot": 0, // OpenTrades

"p": "FLAT", // MarketPosition

"ps": 0, // MarketPositionSize

"pp": "FLAT", // PreviousMarketPosition

"pps": 0 // PreviousMarketPositionSize

},

"sig": { // Signal

"el": 0, // EL

"xl": 0, // XL

"es": 6, // ES

"xs": 0 // XS

},

"ord": ,

"tag":

}

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with signals and a signal filter

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, monitor, or strategy .

Let's connect the Strategy - Plus to a connectable signal filter and connectable indicators :

1. Load all relevant indicators

• Load MA - Plus / Connectable

• Load Signal filter - Plus / Connectable

• Load Strategy - Plus / Connectable

2. Signal Filter Plus: Connect the MA - Plus to the Signal Filter

• Open the signal filter settings

• Choose one of the five input dropdowns (1→, 2→, 3→, 4→, 5→) and choose : MA - Plus / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter settings if needed

• The default filter mode for the trading direction is SWING, and is compatible with the default settings in the strategy and indicators.

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold is 'ABOVE' Threshold 1 (TH1) and Threshold 2 (TH2), both set at 5. This allows each occurrence to score, as the default score is 1 point above the threshold.

5. Strategy Plus: Connect one of the strategy plus inputs to the signal filters signal connector in the strategy settings

• Select a strategy input → and select the Signal filter - Plus: Signal connector

6. Strateg Plus: Enable filter compatible directions

• As the default setting of the filter is SWING, we should also set the SM (Strategy mode) to SWING.

7. Strateg Plus: You're ready to start optimizing

• Dive into all parameters and start optimizing your backtesting results.

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

• Layout and Abbreviations: Abbreviations streamline structure and input identification. Although they may seem complex initially, inline tooltips provide explanations, facilitating quick acclimatization.

• Total Trade Limit Error & Date-Time Filter: For deep backtesting, be mindful of the total trade limit. Utilize the date-time filter to narrow the test scope and avoid TradingView order limits.

• Calculation Timeout: Encounter a timeout? Adjust any parameter slightly to restart the calculation process.

• Message Character Limit: To stay within message character limits, consider turning off certain features or setting some to 'once'.

• Direct Indicator-to-Strategy Connection: When connecting an indicator directly to a strategy without thresholds, the strategy will default to long if weights are equally assigned.

• Pyramid Enabling with DCA and BRO: Activate pyramid orders, enabling you to optimize your strategy during Dollar Cost Averaging and Break Out trades.

• Recalculate & Fill Orders Properties: Adjusting these default settings in strategy properties tab may lead to unexpected behavior when backtesting. Approach with caution.

• Optimized for Crypto: Our indicators have been optimized and tested primarily on cryptocurrency markets. Results in other markets may vary.

• Inline Tooltips Documentation: Detailed documentation and guidance are available via inline tooltips for immediate assistance.

• Strategy Settings Margin: Set margin to 1 to be able to apply leverage.

• Styling Panel: Explore the styling panel to disable labels or any other visual cues to reduce clutter on busy charts, enhancing visual clarity and personalization.

• Applying Leverage on Spot Markets: Ensure that maximum leverage on spot markets is configured to 1.

• Unrealistic Order Sizes: Verify that the order book can accommodate your backtested order sizes.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

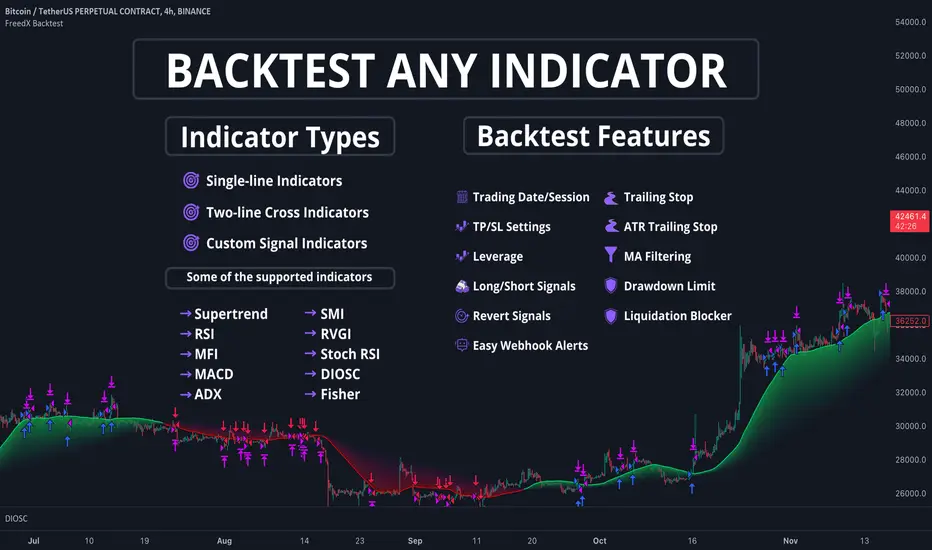

FreedX Grid Backtest█ FreedX Grid Backtest is an open-source tool that offers accurate GRID calculations for GRID trading strategies. This advanced tool allows users to backtest GRID trading parameters with precision, accurately reflecting exchange functionalities. We are committed to enhancing trading strategies through precise backtesting solutions and address the issue of unreliable backtesting practices observed on GRID trading strategies. FreedX Grid Backtest is designed for optimal calculation speed and plotting efficiency, ensuring users to achieve fastest calculations during their analysis.

█ GRID TRADING STRATEGY SETTINGS

The core of the FreedX Grid Backtest tool lies in its ability to simulate grid trading strategies. Grid trading involves placing orders at regular intervals within a predefined price range, creating a grid of orders that capitalize on market volatility.

Features:

⚙️ Backtest Range:

→ Purpose: Allows users to specify the backtesting range of GRID strategy. Closes all positions at the end of this range.

→ How to Use: Drag the dates to fit the desired backtesting range.

⚙️ Investment & Compounding:

→ Purpose: Allows users to specify the total investment amount and select between fixed and compound investment strategies. Compounding adjusts trade quantities based on performance, enhancing the grid strategy's adaptability to market changes.

→ How to Use: Set the desired investment amount and choose between "Fixed" or "Compound" for the investment method.

⚙️ Leverage & Grid Levels:

→ Purpose: Leverage amplifies the investment amount, increasing potential returns (and risks). Users can define the number of grid levels, which determines how the investment is distributed across the grid.

→ How to Use: Input the desired leverage and number of grids. The tool automatically calculates the distribution of funds across each grid level.

⚙️ Distribution Type & Mode:

→ Purpose: Users can select the distribution type (Arithmetic or Geometric) to set how grid levels are determined. The mode (Neutral, Long, Short) dictates the direction of trades within the grid.

→ How to Use: Choose the distribution type and mode based on the desired trading strategy and market outlook.

⚙️ Enable LONG/SHORT Grids exclusively:

█ MANUAL LEVELS AND STOP TRIGGERS

Beyond automated settings, the tool offers manual adjustments for traders seeking finer control over their grid strategies.

Features:

⚙️ Manual Level Adjustment:

→ Purpose: Enables traders to manually set the top, reference, and bottom levels of the grid, offering precision control over the trading range.

→ How to Use: Activate manual levels and adjust the top, reference, and bottom levels as needed to define the grid's scope.