Wedge and Flag Finder (Multi - zigzag)Here is a small attempt to automatically identify wedges and flags.

Tradingview standard wedge checks for only 4 pivots. In this version, I have considered 5 pivots instead - which can help reduce noise as 4 pivots forming wedge can be quite common. In future, will also try to add more pivots in pattern recognition to make the signal more accurate.

If wedge comes with a tail, then it is marked as flag :)

Settings are quite simple and they are as shown below

Göstergeler ve stratejiler

DebugConsoleLibrary "DebugConsole"

Methods for debuging/output into a table, console like style.

init(size) initiate property variables.

Parameters:

size : int, console line size.

Returns: tuple, table and string array.

queue(console_id, new_line) Regular Queue, will be called once every bar its called.

Parameters:

console_id : string array, console configuration array.

new_line : string, with contents for new line.

Returns: void.

queue_one(console_id, new_line) Queue only one time, will not repeat itself.

Parameters:

console_id : string array, console configuration array.

new_line : string, with contents for new line.

Returns: void.

update(table_id, console_id) Update method for the console screen.

Parameters:

table_id : table, table to update console text.

console_id : string array, console configuration array.

Returns: void.

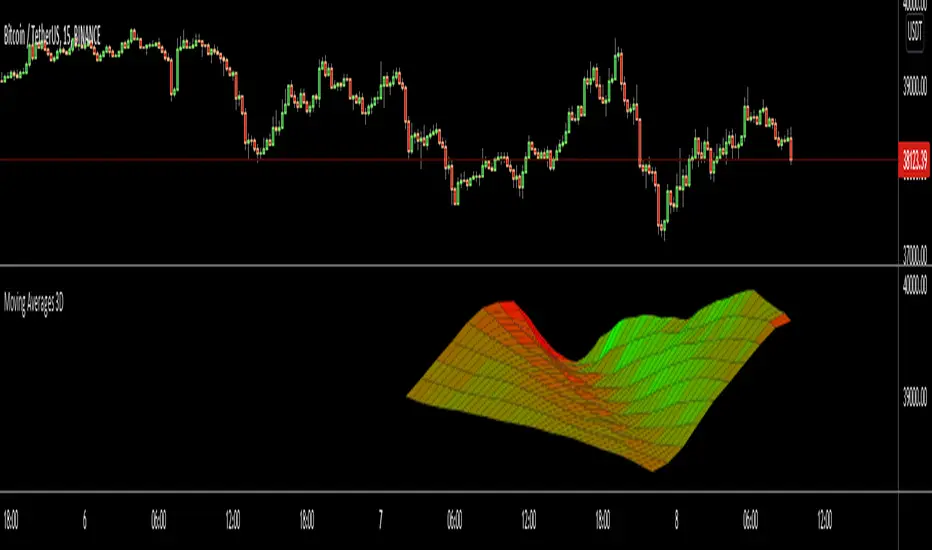

Moving Averages 3DHello All,

This is an experimental work to show 10 moving averages in 3D by using linefill.new() feature of the Pine language.

You can set moving average type as Simple (SMA) or Exponential (EMA)

You can set "Starting Length" and set the "Step" to calculate other lengths. For example; if "Starting Length" is 10 and "step" is 5 then the lengths are 10, 15, 20, 25...

You can set the colors as Red, Green, Blue for each direction. And you can change the width. you can see the examples below

In following example Green and Blue used:

In following example Blue and Red is used and Width is set as 5:

Enjoy!

Zigzag Volume BarsBack to my favourite topic - Zigzags.

Here is an indicator which can help you visualise volume data on Zigzag swing highs and lows.

Settings are pretty simple and provides variety of display options

Display options are as demonstrated in the chart has following main types.

Regular

Plus/Minus - Stacked

Plus/Minus - Overlapping

Plus/Minus - Opposite Sides

Apart from the main display types, stacked display has several sub-types which determine whether to place green bar below red or the other way around.

Snapshot below shows example of each type.

MACD-X Overlay, More Than MACD by DGTMoving Average Convergence Divergence – MACD

The most popular indicator used in technical analysis , the moving average convergence divergence ( MACD ), created by Gerald Appel. MACD is a trend-following momentum indicator , designed to reveal changes in the strength, direction, momentum, and duration of a trend in a financial instrument’s price

Historical evolution of MACD ,

- Gerald Appel created the MACD line,

- Thomas Aspray added the histogram feature to MACD

- Giorgos E. Siligardos created a leader of MACD

MACD employs two Moving Averages of varying lengths (which are lagging indicators) to identify trend direction and duration. Then, MACD takes the difference in values between those two Moving Averages (MACD Line) and an EMA of those Moving Averages (Signal Line) and plots that difference between the two lines as a histogram which oscillates above and below a center Zero Line. The histogram is used as a good indication of a security's momentum.

The MACD indicator is typically good for identifying three types of basic signals;

Signal Line Crossovers

A Signal Line Crossover is the most common signal produced by the MACD . On the occasions where the MACD Line crosses above or below the Signal Line, that can signify a potentially strong move. The standard interpretation of such an event is a recommendation to buy if the MACD line crosses up through the Signal Line (a "bullish" crossover), or to sell if it crosses down through the Signal Line (a "bearish" crossover). These events are taken as indications that the trend in the financial instrument is about to accelerate in the direction of the crossover.

Zero Line Crossovers

Zero Line Crossovers occur when the MACD Line crossed the Zero Line and either becomes positive (above 0) or negative (below 0). A change from positive to negative MACD is interpreted as "bearish", and from negative to positive as "bullish". Zero crossovers provide evidence of a change in the direction of a trend but less confirmation of its momentum than a signal line crossover

Divergence

Divergence is another signal created by the MACD . Simply, divergence occurs when the MACD and actual price are not in agreement. A "positive divergence" or "bullish divergence" occurs when the price makes a new low but the MACD does not confirm with a new low of its own. A "negative divergence" or "bearish divergence" occurs when the price makes a new high but the MACD does not confirm with a new high of its own. A divergence with respect to price may occur on the MACD line and/or the MACD Histogram

Moving Average Crossovers , another hidden signal that MACD Indicator identifies

Many traders will watch for a short-term moving average to cross above a longer-term moving average and use this to signal increasing upward momentum. This bullish crossover suggests that the price has recently been rising at a faster rate than it has in the past, so it is a common technical buy sign. Conversely, a short-term moving average crossing below a longer-term average is used to illustrate that the asset's price has been moving downward at a faster rate and that it may be a good time to sell.

Moving Average Crossovers in reality is Zero Line Crossovers, the value of the MACD indicator is equal to zero each time the two moving averages cross over each other. For easy interpretation by trades, Zero Line Crossovers are simply described as positive or negative MACD

False signals

Like any forecasting algorithm, the MACD can generate false signals. A false positive, for example, would be a bullish crossover followed by a sudden decline in a financial instrument. A false negative would be a situation where there is bearish crossover, yet the financial instrument accelerated suddenly upwards

What is “MACD-X” and Why it is “More Than MACD”

In its simples form, MACD-X implements variety of different calculation techniques applied to obtain MACD Line. Different calculation techniques lead to different values for MACD Line, as will further discuss below, and as a consequence the signal line and the histogram values will differentiate accordingly.

Main features of MACD-X ;

1- Plotting of the Oscillator presented on top of the price chart (main chart) and applicable on both log and linear scale. Maximum plotting length is limited to 250 bars

2- Introduces different proven techniques applied on MACD calculation, such as MACD-AS (Histogram), MACD-Leader and MACD-Source, besides the traditional MACD (MACD-TRADITIONAL)

• MACD-Traditional, by Gerald Appel

It is the MACD that we know, stated as traditional just to avoid confusion with other techniques used with this study

• MACD-Histogram, by Thomas Aspray

The MACD-Histogram measures the distance between MACD and its signal line (the 9-day EMA of MACD ). Aspray developed the MACD-Histogram to anticipate signal line crossovers in MACD . Because MACD uses moving averages and moving averages lag price, signal line crossovers can come late and affect the reward-to-risk ratio of a trade. Bullish or bearish divergences in the MACD-Histogram can alert chartists to an imminent signal line crossover in MACD

Aspray's contribution served as a way to anticipate (and therefore cut down on lag) possible MACD crossovers which are a fundamental part of the indicator.

• MACD-Leader, by Giorgos E. Siligardos, PhD

MACD Leader has the ability to lead MACD at critical situations. Almost all smoothing methods encounter in technical analysis are based on a relative-weighted sum of past prices, and the Leader is no exception. The concealed weights of MACD Leader are such that more relative weight is used in the more recent prices than the respective weights used by the components of MACD . In effect, the Leader expresses more changes in average price dynamics for the recent price movement than MACD , thus eventually leading MACD , especially when significant trend changes are about to take place.

• MACD-Source, a custom experimental interpretation of mine,

MACD Source, presents an application of MACD that evaluates Source/MA Ratio, relatively with less lag, as a basis for MACD Line, also can be expressed as source convergence/divergence to its moving average. Among the various techniques for removing the lag between price and moving average (MA) of the price, one in particular stands out: the addition to the moving average of a portion of the difference between the price and MA. MACD Source, is based on signal length mean of the difference between Source and average value of shot length and long length moving average of the source (Source/MA Ratio), where the source is actual value and hence no lag and relatively less lag with the average value of moving average of the source .

MACD Source provides relatively early crossovers comparing to MACD and better momentum direction indications, assuming the lengths are set to same values

3- Alerts presented for MACD and Signal Line Crosses both for Early Warning and Confirmed Crossovers

For more, You are kindly invited to have a look to other MACD or similar studies presented on separate pane

MACD-X, More Than MACD by DGT , P-MACD by DGT and Price Distance to its MA by DGT

Disclaimer : Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitutes professional and/or financial advice. You alone the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

BjCandlePatternsLibrary "BjCandlePatterns"

Patterns is a Japanese candlestick pattern recognition Library for developers. Functions here within detect viable setups in a variety of popular patterns. Please note some patterns are without filters such as comparisons to average candle sizing, or trend detection to allow the author more freedom.

doji(dojiSize, dojiWickSize) Detects "Doji" candle patterns

Parameters:

dojiSize : (float) The relationship of body to candle size (ie. body is 5% of total candle size). Default is 5.0 (5%)

dojiWickSize : (float) Maximum wick size comparative to the opposite wick. (eg. 2 = bottom wick must be less than or equal to 2x the top wick). Default is 2

Returns: (series bool) True when pattern detected

dLab(showLabel, labelColor, textColor) Produces "Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bullEngulf(maxRejectWick, mustEngulfWick) Detects "Bullish Engulfing" candle patterns

Parameters:

maxRejectWick : (float) Maximum rejection wick size.

The maximum wick size as a percentge of body size allowable for a top wick on the resolution candle of the pattern. 0.0 disables the filter.

eg. 50 allows a top wick half the size of the body. Default is 0% (Disables wick detection).

mustEngulfWick : (bool) input to only detect setups that close above the high prior effectively engulfing the candle in its entirety. Default is false

Returns: (series bool) True when pattern detected

bewLab(showLabel, labelColor, textColor) Produces "Bullish Engulfing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bearEngulf(maxRejectWick, mustEngulfWick) Detects "Bearish Engulfing" candle patterns

Parameters:

maxRejectWick : (float) Maximum rejection wick size.

The maximum wick size as a percentge of body size allowable for a bottom wick on the resolution candle of the pattern. 0.0 disables the filter.

eg. 50 allows a botom wick half the size of the body. Default is 0% (Disables wick detection).

mustEngulfWick : (bool) Input to only detect setups that close below the low prior effectively engulfing the candle in its entirety. Default is false

Returns: (series bool) True when pattern detected

bebLab(showLabel, labelColor, textColor) Produces "Bearish Engulfing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

hammer(ratio, shadowPercent) Detects "Hammer" candle patterns

Parameters:

ratio : (float) The relationship of body to candle size (ie. body is 33% of total candle size). Default is 33%.

shadowPercent : (float) The maximum allowable top wick size as a percentage of body size. Default is 5%.

Returns: (series bool) True when pattern detected

hLab(showLabel, labelColor, textColor) Produces "Hammer" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

star(ratio, shadowPercent) Detects "Star" candle patterns

Parameters:

ratio : (float) The relationship of body to candle size (ie. body is 33% of total candle size). Default is 33%.

shadowPercent : (float) The maximum allowable bottom wick size as a percentage of body size. Default is 5%.

Returns: (series bool) True when pattern detected

ssLab(showLabel, labelColor, textColor) Produces "Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

dragonflyDoji() Detects "Dragonfly Doji" candle patterns

Returns: (series bool) True when pattern detected

ddLab(showLabel, labelColor) Produces "Dragonfly Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

Returns: (series label) A label visible at the chart level intended for the title pattern

gravestoneDoji() Detects "Gravestone Doji" candle patterns

Returns: (series bool) True when pattern detected

gdLab(showLabel, labelColor, textColor) Produces "Gravestone Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tweezerBottom(closeUpperHalf) Detects "Tweezer Bottom" candle patterns

Parameters:

closeUpperHalf : (bool) input to only detect setups that close above the mid-point of the candle prior increasing its bullish tendancy. Default is false

Returns: (series bool) True when pattern detected

tbLab(showLabel, labelColor, textColor) Produces "Tweezer Bottom" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tweezerTop(closeLowerHalf) Detects "TweezerTop" candle patterns

Parameters:

closeLowerHalf : (bool) input to only detect setups that close below the mid-point of the candle prior increasing its bearish tendancy. Default is false

Returns: (series bool) True when pattern detected

ttLab(showLabel, labelColor, textColor) Produces "TweezerTop" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTopBull(wickSize) Detects "Bullish Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stwLab(showLabel, labelColor, textColor) Produces "Bullish Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTopBear(wickSize) Detects "Bearish Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stbLab(showLabel, labelColor, textColor) Produces "Bearish Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTop(wickSize) Detects "Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stLab(showLabel, labelColor, textColor) Produces "Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

morningStar() Detects "Bullish Morning Star" candle patterns

Returns: (series bool) True when pattern detected

msLab(showLabel, labelColor, textColor) Produces "Bullish Morning Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

eveningStar() Detects "Bearish Evening Star" candle patterns

Returns: (series bool) True when pattern detected

esLab(showLabel, labelColor, textColor) Produces "Bearish Evening Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBull() Detects "Bullish Harami" candle patterns

Returns: (series bool) True when pattern detected

hwLab(showLabel, labelColor, textColor) Produces "Bullish Harami" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBear() Detects "Bearish Harami" candle patterns

Returns: (series bool) True when pattern detected

hbLab(showLabel, labelColor, textColor) Produces "Bearish Harami" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBullCross() Detects "Bullish Harami Cross" candle patterns

Returns: (series bool) True when pattern detected

hcwLab(showLabel, labelColor, textColor) Produces "Bullish Harami Cross" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBearCross() Detects "Bearish Harami Cross" candle patterns

Returns: (series bool) True when pattern detected

hcbLab(showLabel, labelColor) Produces "Bearish Harami Cross" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

Returns: (series label) A label visible at the chart level intended for the title pattern

marubullzu() Detects "Bullish Marubozu" candle patterns

Returns: (series bool) True when pattern detected

mwLab(showLabel, labelColor, textColor) Produces "Bullish Marubozu" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

marubearzu() Detects "Bearish Marubozu" candle patterns

Returns: (series bool) True when pattern detected

mbLab(showLabel, labelColor, textColor) Produces "Bearish Marubozu" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

abandonedBull() Detects "Bullish Abandoned Baby" candle patterns

Returns: (series bool) True when pattern detected

abwLab(showLabel, labelColor, textColor) Produces "Bullish Abandoned Baby" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

abandonedBear() Detects "Bearish Abandoned Baby" candle patterns

Returns: (series bool) True when pattern detected

abbLab(showLabel, labelColor, textColor) Produces "Bearish Abandoned Baby" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

piercing() Detects "Piercing" candle patterns

Returns: (series bool) True when pattern detected

pLab(showLabel, labelColor, textColor) Produces "Piercing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

darkCloudCover() Detects "Dark Cloud Cover" candle patterns

Returns: (series bool) True when pattern detected

dccLab(showLabel, labelColor, textColor) Produces "Dark Cloud Cover" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tasukiBull() Detects "Upside Tasuki Gap" candle patterns

Returns: (series bool) True when pattern detected

utgLab(showLabel, labelColor, textColor) Produces "Upside Tasuki Gap" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tasukiBear() Detects "Downside Tasuki Gap" candle patterns

Returns: (series bool) True when pattern detected

dtgLab(showLabel, labelColor, textColor) Produces "Downside Tasuki Gap" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

risingThree() Detects "Rising Three Methods" candle patterns

Returns: (series bool) True when pattern detected

rtmLab(showLabel, labelColor, textColor) Produces "Rising Three Methods" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

fallingThree() Detects "Falling Three Methods" candle patterns

Returns: (series bool) True when pattern detected

ftmLab(showLabel, labelColor, textColor) Produces "Falling Three Methods" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

risingWindow() Detects "Rising Window" candle patterns

Returns: (series bool) True when pattern detected

rwLab(showLabel, labelColor, textColor) Produces "Rising Window" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

fallingWindow() Detects "Falling Window" candle patterns

Returns: (series bool) True when pattern detected

fwLab(showLabel, labelColor, textColor) Produces "Falling Window" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

kickingBull() Detects "Bullish Kicking" candle patterns

Returns: (series bool) True when pattern detected

kwLab(showLabel, labelColor, textColor) Produces "Bullish Kicking" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

kickingBear() Detects "Bearish Kicking" candle patterns

Returns: (series bool) True when pattern detected

kbLab(showLabel, labelColor, textColor) Produces "Bearish Kicking" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

lls(ratio) Detects "Long Lower Shadow" candle patterns

Parameters:

ratio : (float) A relationship of the lower wick to the overall candle size expressed as a percent. Default is 75%

Returns: (series bool) True when pattern detected

llsLab(showLabel, labelColor, textColor) Produces "Long Lower Shadow" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

lus(ratio) Detects "Long Upper Shadow" candle patterns

Parameters:

ratio : (float) A relationship of the upper wick to the overall candle size expressed as a percent. Default is 75%

Returns: (series bool) True when pattern detected

lusLab(showLabel, labelColor, textColor) Produces "Long Upper Shadow" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bullNeck() Detects "Bullish On Neck" candle patterns

Returns: (series bool) True when pattern detected

nwLab(showLabel, labelColor, textColor) Produces "Bullish On Neck" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bearNeck() Detects "Bearish On Neck" candle patterns

Returns: (series bool) True when pattern detected

nbLab(showLabel, labelColor, textColor) Produces "Bearish On Neck" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

soldiers(wickSize) Detects "Three White Soldiers" candle patterns

Parameters:

wickSize : (float) Maximum allowable top wick size throughout pattern expressed as a percent of total candle height. Default is 5%

Returns: (series bool) True when pattern detected

wsLab(showLabel, labelColor, textColor) Produces "Three White Soldiers" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

crows(wickSize) Detects "Three Black Crows" candle patterns

Parameters:

wickSize : (float) Maximum allowable bottom wick size throughout pattern expressed as a percent of total candle height. Default is 5%

Returns: (series bool) True when pattern detected

bcLab(showLabel, labelColor, textColor) Produces "Three Black Crows" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

triStarBull() Detects "Bullish Tri-Star" candle patterns

Returns: (series bool) True when pattern detected

tswLab(showLabel, labelColor, textColor) Produces "Bullish Tri-Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

triStarBear() Detects "Bearish Tri-Star" candle patterns

Returns: (series bool) True when pattern detected

tsbLab(showLabel, labelColor, textColor) Produces "Bearish Tri-Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

wrap(cond, barsBack, borderColor, bgcolor) Produces a box wrapping the highs and lows over the look back.

Parameters:

cond : (series bool) Condition under which to draw the box.

barsBack : (series int) the number of bars back to begin drawing the box.

borderColor : (series color) Color of the four borders. Optional. The default is color.gray.

bgcolor : (series color) Background color of the box. Optional. The default is color.gray.

Returns: (series box) A box who's top and bottom are above and below the highest and lowest points over the lookback

topWick() returns the top wick size of the current candle

Returns: (series float) A value equivelent to the distance from the top of the candle body to its high

bottomWick() returns the bottom wick size of the current candle

Returns: (series float) A value equivelent to the distance from the bottom of the candle body to its low

body() returns the body size of the current candle

Returns: (series float) A value equivelent to the distance between the top and the bottom of the candle body

highestBody() returns the highest body of the current candle

Returns: (series float) A value equivelent to the highest body, whether it is the open or the close

lowestBody() returns the lowest body of the current candle

Returns: (series float) A value equivelent to the highest body, whether it is the open or the close

barRange() returns the height of the current candle

Returns: (series float) A value equivelent to the distance between the high and the low of the candle

bodyPct() returns the body size as a percent

Returns: (series float) A value equivelent to the percentage of body size to the overall candle size

midBody() returns the price of the mid-point of the candle body

Returns: (series float) A value equivelent to the center point of the distance bewteen the body low and the body high

bodyupGap() returns true if there is a gap up between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap up and no overlap in the real bodies of the current candle and the preceding candle

bodydwnGap() returns true if there is a gap down between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap down and no overlap in the real bodies of the current candle and the preceding candle

gapUp() returns true if there is a gap down between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap down and no overlap in the real bodies of the current candle and the preceding candle

gapDwn() returns true if there is a gap down between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap down and no overlap in the real bodies of the current candle and the preceding candle

dojiBody() returns true if the candle body is a doji

Returns: (series bool) true if the candle body is a doji. Defined by a body that is 5% of total candle size

RedK Momentum Bars (RedK Mo_Bars)Momentum Bars (Mo_Bars) offers a different way to visualize (relative) momentum - and uses some simple TA concepts to provide a different perspective into how we read momentum changes and incorporate that in our trading.

The idea here (and the script itself) is really super simple, and is (very loosely) inspired by Elder's Impulse System (EIS) - then evolved to leverage some other concepts, and to become less cluttering and "easier to read".

The construction of the Mo_Bars

---------------------------------------------

The base concept utilizes 3 moving average lines :

the first line is a relatively fast MA with a short length - acts as the main price tracking line

the second line is slightly slower than the main line - 2 to 3 bars longer length - and will by default use the open value as source - this works better to identify when the closing price starts to move faster than the open (as in, bars more frequently close higher than they open) - this line acts as the signal line - there's an added setting for an additional delay that utilizes regular WMA smoothing - the delay acts to magnify the relative displacement between the 2 MAs

for both these MA's, i choose to use the RSS MA (Lazy Line) - other MA types can be used, but the reason i used that MA type specifically is that it moves "gracefully" - and 2 Lazy Lines moving together minimizes whipsaws from small price swings - i tested with other MA types and found that the RSS has an advantage there.

the third line is a much slower MA (length 5 to 6 x the fast line) - and acts as a filter or a baseline. When we're above that line, we should favor long positions - we're in bull territory. When we're below that line we favor short positions, and we're in bear territory. Adjust this line as it suits your trading style and time frame.

(I choose to use WMA as the MA type for the filter line .. and there's a good reason for that - which i'll skip for now - but in future versions, we can add other selectable MA types. )

Using Mo_Bars

----------------------------

at a very broad level, we can use Mo_Bars similar to how we use a MACD - both are centered and unrestricted oscillators - note the difference that Mo_Bars is based on 3 MA's rather than 2.

the Mo_Bar bar length reflects the distance between the main MA and the signal MA - plotted relative to the baseline (filter line) - that means that the length of the bar represents the relative momentum between the 2 MA's - The Mo_Bars are then colored in a way that reflects increase or decrease in the value of that momentum (the visual here may have been inspired by another indicator recently published by one of our esteemed wizards - it worked perfectly - so due credits here :)

-- in simple terms, if the main MA is below the signal MA, the bar is red - and when the main MA is above the signal MA, the bar is green - a white bar usually shows up when there's a detected change of relative momentum direction (note that this is not the same as the trend direction - and that's what helps show and exploit convergence and divergence - similar to a MACD)

* in the chart above, i noted few examples of how visualizing relative momentum in this way exposes areas of chop (Mo_Bars above zero but are in red or moving down, or when Mo_Bars are below zero and green or moving up) - convergence / divergence with price - and how this can act to expose the possibility of potential changes in price action or trend.

* there's so much more to play around with this setup - and maybe if there's enough interest there can be future dedicated posts on how utilize or even to evolve it further - there's a lot of potential here, to add more filters (maybe volume based), alerts, signals...etc - so let's see the interest :)

Here's the detailed (top chart) setup that Mo_Bars is based on -- The settings for the MA's on the price charts have been matched / sync'ed with the Mo_Bars settings on the lower panel to demonstrate how the script works and how it translate the MA action on the price chart to what we see below.

As always, please play around with the indicator to get used to how it works - use it in tandem with other indicators to get proper confirmations and adjust settings to suit your own trading style, time frame, and instruments

Feedback and thoughts are always welcome --- good luck!

Short Volume StamperHello!

BE SURE TO RUN THE SCRIPT WITH BAR REPLAY TO SEE WHAT IT DOES! I hope you like it!

This script calculates the total short volume, total volume, and the short volume / total volume ratio since the 2-year high price. In addition, the approximate dollar value of all short volume since the 2-year high, and the approximate dollar value of all non-short sell volume since the 2-year high is calculated using VWAP. A red line (short interest ratio >= 20%) connects the 2-year high to current session’s high price; a green line (short interest ratio < 20%) connects the 2-year high to the current session’s high.

The script also “stamps” sessions in which a NEW 1-year high in SHORT volume is achieved, and when a PIVOT POINT high is achieved (highest high over 51 sessions). When a new high in short volume is achieved the script aggregates the total volume and short volume for the 5 sessions prior to the new high, the session of the new high, and the 4 sessions after the new high (10 sessions). Additional volume calculations are performed for the 10 session period!

When a pivot point high is achieved the script aggregates the total volume and short volume for the 3 sessions prior to the pivot high, the session of the pivot high, and the 2 sessions after the new high (6 sessions). Additional volume calculations are performed for the 6 session period!

Red labels, red boxes, and red lines indicate a short volume ratio greater than or equal to 20% over the corresponding period!

Green labels, green boxes, and green lines indicate a short volume ratio less than 20% over the corresponding period!

Financial GrowthThis indicator will acquire the financial data provided by Tradview.

the data is compare between Quarter, Annual and TTM in term of percent of growth.

YoY, QoQ and CAGR is also available by this script (The minimum is 4).

in addition, ploting of data, label and table also available (you can check the mark to toggle on / off).

Data : Revenue, Net Income, EBITDA, EPS, DVPS, Free Cash Flow and Forward PE .

How to use it.

just select the financial data, period and size of data to compare.

you can check the box to toggle the plotting line, label and table.

Enjoy.

KCGmut“KCGmut” stands for “Mutations Of Keltner Center Of Gravity Channel”.

After adding the ‘KeltCOG Width’ label to the KeltCOG, I got the idea of creating a subpanel indicator to show the development of the width-percent in previous periods. After some more thinking, I decided that the development of the COG-width-percent should also be reported and somehow the indicator should report whether the close is over (momentum is up), in (momentum is sideways) or under (momentum is down) the COG ( This is the gray area in the channel).

Borrowing from other scripts:

I tweeked the script of the KeltCOG (published) to calculate the columns and of REVE (also published) to calculate the volume spikes. Because the KeltCOG script had the default option to let the script chose lookback and adapt the width, I decided to not provide inputs to tweek lookback or channel width. Thus, if you use a KeltCOG in default setting, REVE and KCGmut together in the same chart, these will provide consistent complementary information about the candle. This layout has this combination:

I added actual volume to show where volume spikes occur.

Columns

For the channel-width-percent half of the value is used and for the COG-width-percent the whole to get a better image

By plotting the columns of the full width before those of the COG, in two series of positive and negative values, I created the illusion of a column with a different colored patch representing the COG (most are black) at the bottom where it points up (showing momentum is up), in the middle when the close is in the COG (no momentum) or at the top when the close is below the COG (showing momentum is down)

coloring drama

When nothing much happens, i.e. the channels keep the same width of shrink a bit, the columns get an unobtrusive color, black for the small COG patches and bluish gray for the channel columns pointing up or sideways, reddish gray when pointing down. If the COG increases (drama) the patches get colored lime (up), red (down) or orange (sideways, very seldom). If the channel increases, the columns get colored gold (up), maroon (down) or orange (sideways). Because the COG is derived from a Donchian channel, drama means a new high or low in the lookback period. Drama in the KeltCOG channel just means increase in volatility.

histogram showing volume spikes

Blue spikes indicate more then twice as much volume then recently normal, Maroon spikes indicate clear increases less then twice. To prevent the histogram from disappearing behind a column it is plotted first, spikes made longer then the column and also plotted both positive and negative. Single volume spikes don’t mean much, however if these occur in consecutive series and also come together with drama like new highs or increase in volatility, volume is worth noting. I regard such events as ‘voting’, the market ‘votes’ up or down. The REVE analyses these events to asses whether the volume stems from huge institutional traders (‘whales’) or large numbers of small traders (‘muppets’). This might be interesting too.

Remarks about momentum

Like in MACD, momentum has a direction. The difference is that in KCGmut momentum is a choise of the market to move above the COG (uptrend) or in (sideways) or under (downtrend), whereas in MACD the indicator shows the energy with which the market moves up or down. How does the market ‘choose’? The market doesn’t ‘think’, but still it comes to decisions. I see an analogy with the way a swarm of birds decides to go here or there, up or down, or land in a tree. All birds seem to agree but I guess a single bird has not much say in what the swarm does.

RedK Volume-Accelerated Directional Energy Ratio (RedK VADER)The Volume-Accelerated Directional Energy Ratio (VADER) makes use of price moves (displacement) and the associated volume (effort) to estimate the positive (buying) and negative (selling) "energy" behind the scenes, enabling traders to "read the market action" in more details and adjust their trading decisions accordingly.

How does VADER work?

------------------------------------

I have always been a fan of technical analysis concepts that are simple, and that integrate both price action and volume together - The concept behind VADER is really a simple one.

Let's walk though it as we avoid getting too technical:

Large price moves that are associated with large volume means buyers (if the move is up) or sellers (when the move is down) are serious and are "in control" of the action

On the other hand, when the price moves are small but with large volume, it means there's a fight, or more of a balance of energy, between buying and selling.

Also when large price moves are associated with relatively limited volume, there's a lack of "energy" from either buyers or sellers - and moves likes these are usually short-lived.

The analogy with VADER, is that we look at price moves (change of close between 2 bars) as the displacement (or action result) and the associated volume as the "effort" behind this action -- Combining these 2 values together, the displacement and the effort, gives us a representation or a proxy of the underlying energy (in a specific direction).

when both values (displacement and effort) are high, then the resulting energy is high - and if one of these values are low, the resulting energy is low.

we then take an average of that relative energy in each direction (positive = buying and negative = selling) and calculate the net energy.

note that we're approaching the analogy here from a trading perspective and not from physics perspective :) -- we can be forgiven if the energy calculation in physics is different ..

VADER Plots

---------------------

the blue line with crosses represents the positive energy - or the buying strength

the orange line with circles represents the negative energy - or the selling strength

the thick Green / Red main line plot represents the net energy - and generally the main signal to be looking out for is when that line crosses 0 up or down - but i find it also very valuable to keep an eye on the individual energy lines as they sometimes "tell a story" like we see in the chart above,

Volume Calculation:

----------------------------

- VADER by default is a volume-weighted indicator - it uses the volume associated with change in bar close value (Full mode) as an accelerator in the calculation of the directional energy

- VADER introduces another method of integrating volume, by considering "relative" or "differential" volume (Relative mode) - in this mode, we consider the ratio of volume above the minimum volume observed within a "lookback" length - so practically, ignoring the minimum volume. in other words, if a price move is associated with very low volume, it gets very low "volume accelerator" (close to 0) and if the move is associated with very large volume, it gets the maximum volume accelerator (1 or close to 1) - The relative mode of volume calculation magnifies volume effect and ignores the low volume values that may just act as noise. test both modes and find which one works better for you.

- VADER also has the ability to work without volume (volume calculation = None) - and will revert to that mode when used with instruments that have no volume data. In that mode, VADER will behave similar to an RSI (but not exactly like it given the underlying calculation is different)

- We can also setup VADER at a specific resolution / timeframe that is different than the chart.

Using VADER & Other Thoughts

----------------------------------------

The main signal to look out for, is when VADER's Green / Red line crosses the zero line.

Green (above zero) represents that the net energy is with the buyers and we should favor long positions

Red (below zero) reflects that the sellers have control and we should favor short positions (or consider to close longs)

*** However, VADER should be used as a *secondary indicator* - given the big influence of volume on the calculation - VADER doesn't directly track price trend or momentum - VADER needs to be used in the context of other indicators that show trend and momentum - i would suggest you combine VADER with Moving Averages or other trend tracking indicators on the price chart, MACD, RSI and / or other trend and momentum indicators you're already familiar with.

Suggested setup:

There's more to add to VADER in future versions - alerts, control level, maybe improve visuals... etc - please share your feedback as you start experimenting with VADER.. good luck! (and of course, May the Force be with you :) )

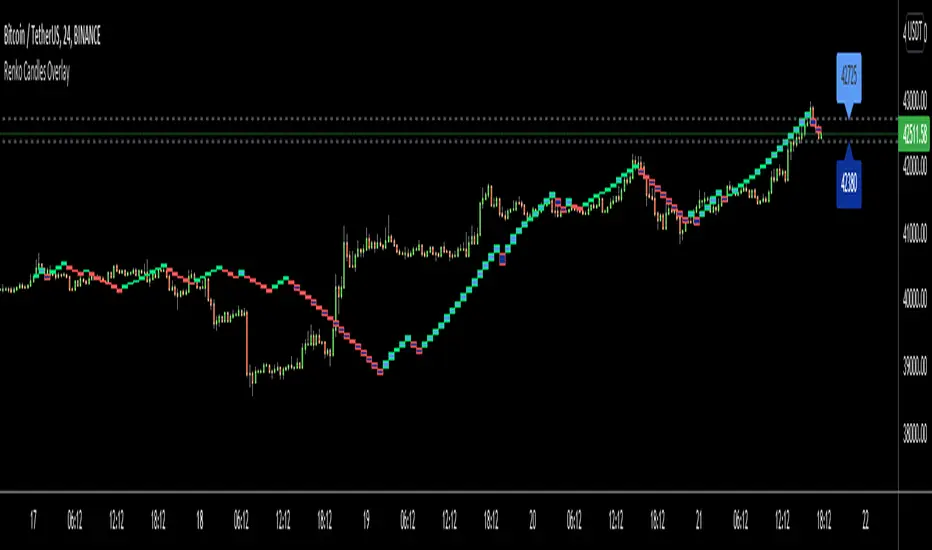

Renko Candles OverlayHello All,

For long time I got many request for Renko Candles and now here it's, Renko Candles Overlay . I tried to make almost everything optional, so you can play with the options as you want.

Let see the options:

Method: the option for brick scaling method: ATR, ATR/2, ATR/4, Percent, Traditional

- ATR Period: period for Average True Range and it's valid if the method is ATR

- ATR/2 Period: period for Average True Range and it's valid if the method is ATR/2

- ATR/4 Period: period for Average True Range and it's valid if the method is ATR/4

- Traditional: User-defined brick size, it's valid if the method is Traditional

- Percent: Percent of Close price, it's valid if the method is Percent

if the method is not Traditional (fixed brick size) then Brick size is calculated/updated when new bricks added. so The box sizes may be different because of the calculation is dynamic.

Levels & Lines for new Bricks: if you enable this option then the script shows the levels for new brick

Change Bar Color: optionally the script changes the bar color by using direction of the bricks

and some other options for coloring.

The script shows the bricks for visible area, which is approximately 280 candles. so if you change the width and number of the bricks then number of bricks that is shown is adjusted automatically to fit the screen. you can see the examples below:

The script shows the levels to new brick as a line and label:

Because of real-time bar is not confirmed until the candle close, the script shows the bricks as Unconfirmed , and unconfirmed bricks shown in different color:

You can change the width of the bricks (width is 10 in following example):

Optionally candle colors are changde by the direction of the bricks:

If you have any recommendation then please drop a comment under the script ;)

Enjoy!

FINRA Daily Short Sale Volume█ OVERVIEW

This indicator displays the Daily Short Sale Volume data reported by FINRA for US Stocks markets, namely NASDAQ, NYSE and NYSE ARCA.

█ CONCEPTS

Daily Short Sale Volume data is different from the bi-monthly Short Interest data also reported by FINRA. Whereas Short Interest represents open positions, Short Sale Volume represents transactions, some of which are executed to offset other trades that will not necessarily result in an open short position reported in Short Interest data. This explains why Short Sale Volume values are always greater than Short Interest ones.

Daily Short Sale Volume provides aggregated volume by security for all short trades executed and reported to FINRA during normal market hours, i.e., media-reported trades. It's important to note that Short Sale Volume is not consolidated with exchange data and excludes trading activity that is not publicly disseminated.

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

If the chart's symbol is traded on one of the exchanges for which FINRA provides Daily Short Sale Volume, it will be displayed in columns. The columns are a brighter red when their value is above average.

You can display Short Sale Volume for another symbol by checking the "Other symbol" checkbox of the script settings' "Inputs" tab and selecting the symbol.

The moving average's length is in days, as Short Volume is daily data. You can hide the average in the script's settings "Style" tab.

█ NOTES

You will find more information on the Short Sale Volume Data and Understanding Short Sale Volume Data pages of the FINRA website.

Short Interest data reported by FINRA is not yet available on our platform.

On TradingView, Short Sale Volume data is accessible through tickers using special names. For example, NASDAQ:AAPL's Short Sale Volume data can be loaded on your chart via the FINRA:AAPL_SHORT_VOLUME ticker. The indicator displays the name of the ticker used to fetch data in the bottom left. It can be hidden by unchecking the "Tables" item in the "Style" tab of the script's settings.

Look first. Then leap.

HTF Candles & PivotsThis indicator displays HTF candles and pivot points.

The candles are displayed in a box and you can select Open-Close, High-Low or both.

You can show all of the past, or just "today only" or "previous day only".

You can also shift one previous candle to the current one.

The pivot point is the normal one.

There is an option to display CPR (Central pivot range).

Example: Shift previous to current

McDonald's Pattern [LuxAlgo]Tradingview asked, we delivered. This script fits a cubic Bezier curve using tops/bottoms in order to approximate a McDonalds pattern, a popular meme pattern in the crypto trading community.

Traditionally the McDonalds pattern is described by an M pattern with deep retracement (> 50%), forming a McDonalds logo.

Please note that this indicator is a meme & should not be taken seriously. Some aspects of this indicator are not real-time and meant for descriptive analysis alongside other components of this script, in this case, for entertainment purposes. We suggest looking through our other open-source scripts if you’re looking for more serious tools.

🔶 USAGE

The script fits Bezier curves using specific tops/bottoms as control points. When the distance between tops and bottoms values is relatively small, the user can more easily identify the pattern.

A score is shown on the top right of the chart, aiming to return how close the returned pattern is to the original logo.

A regular Mcdonalds pattern would return a red background, while an inverted pattern would return a green one.

🔶 SETTINGS

Length: Sensitivity of tops/bottoms detection. The method does not make use of pivot points, using rolling maximums/minimums instead.

Use First Bar As Vertex: Use the price and bar index of the last bar as vertex.

Weekly Volume HeatmapThis tool is designed to visualize how the trading volume of each asset changes during the week.

How to use

This tool can help us better understand the market and answer many questions, such as:

◽ How to avoid getting stop hunted?

Typically, trading volume decreases at certain times of the week, which is the best time for large holders to manipulate the market. Low volume means there is less liquidity in the market. Large transactions in an illiquid market can cause large price changes.

Large holders (whales) have enough capital to push the price in the desired direction to trigger a cascade of stop-loss orders which can move the price further.

After a stop hunt, the market typically reverses, leaving stop hunted traders behind.

It is best to avoid using stop-loss orders and leveraged trading during these hours of the week.

◽ When’s the best time to make decisions

During some hours of the week the trading volume usually decreases; at these times, most traders are inactive and do not participate in transactions.

Therefore, the price changes that occur during these times lack conviction.

It is better to make decisions when there are more active traders in the market. At these periods, a relatively high trading volume is usually observed.

How it works

First, it calculates the average traded volume of each period (for example Monday 9:00 AM) from the first bar to the last bar. It then calculates the ratio of the average traded volume in each period to the average traded volume per week. Finally, the result is displayed as a percentage in each cell.

Different values are distinguished by different background colors. Light colors are used for low values and dark colors are used for high values.

Limits

It only works in the 1 hour time frame.

Samples

Stock => AAPL

Futures => ES1!

Forex => EURUSD

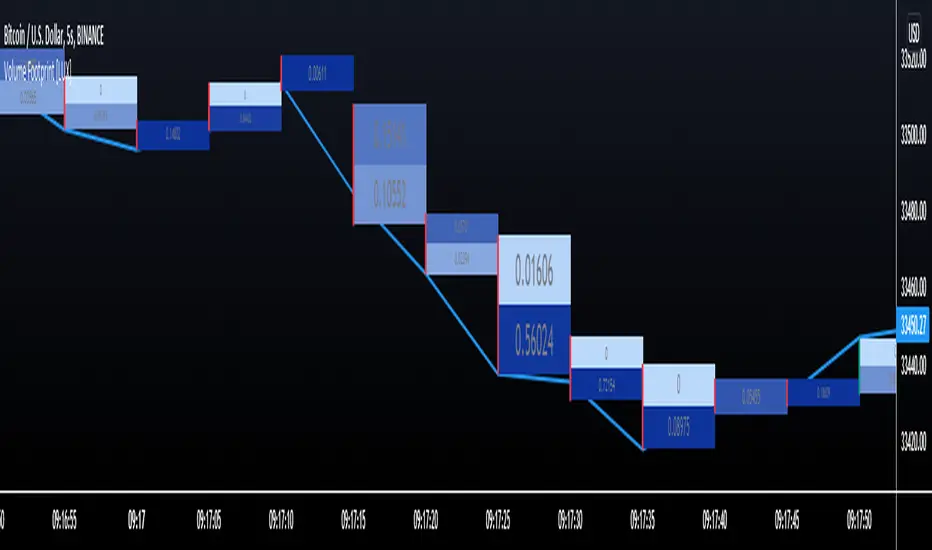

Volume Footprint [LuxAlgo]This indicator estimates a volume footprint using tick data. The script automatically separates a candle into equidistant intervals with a width obtained from the average true range or a user-given width.

Settings

Method: Interval width calculation method. This ultimately determines the number of intervals separating one candle.

Width (At the right of Method): Atr period or user given width depending on the selected method. A lower user-given width would divide a candle into a higher number of intervals.

As Percent: Returns the accumulated volume within each interval as a percentage of the total candle volume.

Style

Display Type: Determines the appearance of the returned volume footprint.

Trend Color: Color to use based on whether a candle is bullish or bearish.

Usage

When applied to a chart, the user will be asked to select the settings to use for the volume footprint. Note that changing the settings afterward will reset the volume footprint, removing previously generated footprints.

A new footprint will appear on the confirmation of a new bar, as such this version might only be useful in lower timeframes.

A volume footprint allows users to see the number of contracts exchanged within a candle interval. It can as such be seen as some kind of intrabar volume profile.

This can be useful to see areas of interest within a candle.

Different Appearance

By default, the volume footprint makes use of colored boxes with a color based on whether the candle was bullish or bearish.

Another appearance that gives additional information is the gradient type, which uses intervals color based on the number of contracts exchanged within an interval relative to the total volume of the candle. A higher number of contracts within an interval would return a darker color by default.

The regular display type makes use of boxes with a single color, with lines on the side indicating whether the candle was bullish or bearish.

FunctionLinearRegressionLibrary "FunctionLinearRegression"

Method for Linear Regression using array sample points.

linreg(sample_x, sample_y) Performs Linear Regression over the provided sample points.

Parameters:

sample_x : float array, sample points X value.

sample_y : float array, sample points Y value.

Returns: tuple with:

_predictions: Array with adjusted Y values.

_max_dev: Max deviation from the mean.

_min_dev: Min deviation from the mean.

_stdev/_sizeX: Average deviation from the mean.

draw(sample_x, sample_y, extend, mid_color, mid_style, mid_width, std_color, std_style, std_width, max_color, max_style, max_width) Method for drawing the Linear Regression into chart.

Parameters:

sample_x : float array, sample point X value.

sample_y : float array, sample point Y value.

extend : string, default=extend.none, extend lines.

mid_color : color, default=color.blue, middle line color.

mid_style : string, default=line.style_solid, middle line style.

mid_width : int, default=2, middle line width.

std_color : color, default=color.aqua, standard deviation line color.

std_style : string, default=line.style_dashed, standard deviation line style.

std_width : int, default=1, standard deviation line width.

max_color : color, default=color.purple, max range line color.

max_style : string, default=line.style_dotted, max line style.

max_width : int, default=1, max line width.

Returns: line array.

pandas_taLibrary "pandas_ta"

Level: 3

Background

Today is the first day of 2022 and happy new year every tradingviewers! May health and wealth go along with you all the time. I use this chance to publish my 1st PINE v5 lib : pandas_ta

This is not a piece of cake like thing, which cost me a lot of time and efforts to build this lib. Beyond 300 versions of this script was iterated in draft.

Function

Library "pandas_ta"

PINE v5 Counterpart of Pandas TA - A Technical Analysis Library in Python 3 at github.com

The Original Pandas Technical Analysis (Pandas TA) is an easy to use library that leverages the Pandas package with more than 130 Indicators and Utility functions and more than 60 TA Lib Candlestick Patterns.

I realized most of indicators except Candlestick Patterns because tradingview built-in Candlestick Patterns are even more powerful!

I use this to verify pandas_ta python version indicators for myself, but I realize that maybe many may need similar lib for pine v5 as well.

Function Brief Descriptions (Pls find details in script comments)

bton --> Binary to number

wcp --> Weighted Closing Price (WCP)

counter --> Condition counter

xbt --> Between

ebsw --> Even Better SineWave (EBSW)

ao --> Awesome Oscillator (AO)

apo --> Absolute Price Oscillator (APO)

xrf --> Dynamic shifted values

bias --> Bias (BIAS)

bop --> Balance of Power (BOP)

brar --> BRAR (BRAR)

cci --> Commodity Channel Index (CCI)

cfo --> Chande Forcast Oscillator (CFO)

cg --> Center of Gravity (CG)

cmo --> Chande Momentum Oscillator (CMO)

coppock --> Coppock Curve (COPC)

cti --> Correlation Trend Indicator (CTI)

dmi --> Directional Movement Index(DMI)

er --> Efficiency Ratio (ER)

eri --> Elder Ray Index (ERI)

fisher --> Fisher Transform (FISHT)

inertia --> Inertia (INERTIA)

kdj --> KDJ (KDJ)

kst --> 'Know Sure Thing' (KST)

macd --> Moving Average Convergence Divergence (MACD)

mom --> Momentum (MOM)

pgo --> Pretty Good Oscillator (PGO)

ppo --> Percentage Price Oscillator (PPO)

psl --> Psychological Line (PSL)

pvo --> Percentage Volume Oscillator (PVO)

qqe --> Quantitative Qualitative Estimation (QQE)

roc --> Rate of Change (ROC)

rsi --> Relative Strength Index (RSI)

rsx --> Relative Strength Xtra (rsx)

rvgi --> Relative Vigor Index (RVGI)

slope --> Slope

smi --> SMI Ergodic Indicator (SMI)

sqz* --> Squeeze (SQZ) * NOTE: code sufferred from very strange error, code was commented.

sqz_pro --> Squeeze PRO(SQZPRO)

xfl --> Condition filter

stc --> Schaff Trend Cycle (STC)

stoch --> Stochastic (STOCH)

stochrsi --> Stochastic RSI (STOCH RSI)

trix --> Trix (TRIX)

tsi --> True Strength Index (TSI)

uo --> Ultimate Oscillator (UO)

willr --> William's Percent R (WILLR)

alma --> Arnaud Legoux Moving Average (ALMA)

xll --> Dynamic rolling lowest values

dema --> Double Exponential Moving Average (DEMA)

ema --> Exponential Moving Average (EMA)

fwma --> Fibonacci's Weighted Moving Average (FWMA)

hilo --> Gann HiLo Activator(HiLo)

hma --> Hull Moving Average (HMA)

hwma --> HWMA (Holt-Winter Moving Average)

ichimoku --> Ichimoku Kinkō Hyō (ichimoku)

jma --> Jurik Moving Average Average (JMA)

kama --> Kaufman's Adaptive Moving Average (KAMA)

linreg --> Linear Regression Moving Average (linreg)

mgcd --> McGinley Dynamic Indicator

rma --> wildeR's Moving Average (RMA)

sinwma --> Sine Weighted Moving Average (SWMA)

ssf --> Ehler's Super Smoother Filter (SSF) © 2013

supertrend --> Supertrend (supertrend)

xsa --> X simple moving average

swma --> Symmetric Weighted Moving Average (SWMA)

t3 --> Tim Tillson's T3 Moving Average (T3)

tema --> Triple Exponential Moving Average (TEMA)

trima --> Triangular Moving Average (TRIMA)

vidya --> Variable Index Dynamic Average (VIDYA)

vwap --> Volume Weighted Average Price (VWAP)

vwma --> Volume Weighted Moving Average (VWMA)

wma --> Weighted Moving Average (WMA)

zlma --> Zero Lag Moving Average (ZLMA)

entropy --> Entropy (ENTP)

kurtosis --> Rolling Kurtosis

skew --> Rolling Skew

xev --> Condition all

zscore --> Rolling Z Score

adx --> Average Directional Movement (ADX)

aroon --> Aroon & Aroon Oscillator (AROON)

chop --> Choppiness Index (CHOP)

xex --> Condition any

cksp --> Chande Kroll Stop (CKSP)

dpo --> Detrend Price Oscillator (DPO)

long_run --> Long Run

psar --> Parabolic Stop and Reverse (psar)

short_run --> Short Run

vhf --> Vertical Horizontal Filter (VHF)

vortex --> Vortex

accbands --> Acceleration Bands (ACCBANDS)

atr --> Average True Range (ATR)

bbands --> Bollinger Bands (BBANDS)

donchian --> Donchian Channels (DC)

kc --> Keltner Channels (KC)

massi --> Mass Index (MASSI)

natr --> Normalized Average True Range (NATR)

pdist --> Price Distance (PDIST)

rvi --> Relative Volatility Index (RVI)

thermo --> Elders Thermometer (THERMO)

ui --> Ulcer Index (UI)

ad --> Accumulation/Distribution (AD)

cmf --> Chaikin Money Flow (CMF)

efi --> Elder's Force Index (EFI)

ecm --> Ease of Movement (EOM)

kvo --> Klinger Volume Oscillator (KVO)

mfi --> Money Flow Index (MFI)

nvi --> Negative Volume Index (NVI)

obv --> On Balance Volume (OBV)

pvi --> Positive Volume Index (PVI)

dvdi --> Dual Volume Divergence Index (DVDI)

xhh --> Dynamic rolling highest values

pvt --> Price-Volume Trend (PVT)

Remarks

I also incorporated func descriptions and func test script in commented mode, you can test the functino with the embedded test script and modify them as you wish.

This is a Level 3 free and open source indicator library.

Feedbacks are appreciated.

This is not the end of pandas_ta lib publication, but it is start point with pine v5 lib function and I will add more and more funcs into this lib for my own indicators.

Function Name List:

bton()

wcp()

count()

xbt()

ebsw()

ao()

apo()

xrf()

bias()

bop()

brar()

cci()

cfo()

cg()

cmo()

coppock()

cti()

dmi()

er()

eri()

fisher()

inertia()

kdj()

kst()

macd()

mom()

pgo()

ppo()

psl()

pvo()

qqe()

roc()

rsi()

rsx()

rvgi()

slope()

smi()

sqz_pro()

xfl()

stc()

stoch()

stochrsi()

trix()

tsi()

uo()

willr()

alma()

wcx()

xll()

dema()

ema()

fwma()

hilo()

hma()

hwma()

ichimoku()

jma()

kama()

linreg()

mgcd()

rma()

sinwma()

ssf()

supertrend()

xsa()

swma()

t3()

tema()

trima()

vidya()

vwap()

vwma()

wma()

zlma()

entropy()

kurtosis()

skew()

xev()

zscore()

adx()

aroon()

chop()

xex()

cksp()

dpo()

long_run()

psar()

short_run()

vhf()

vortex()

accbands()

atr()

bbands()

donchian()

kc()

massi()

natr()

pdist()

rvi()

thermo()

ui()

ad()

cmf()

efi()

ecm()

kvo()

mfi()

nvi()

obv()

pvi()

dvdi()

xhh()

pvt()

HarmonicPatternLibrary "HarmonicPattern"

Functions to detect/check harmonic patterns from provided values.

line_price_rate(point_c, point_b, point_a) Compute the price rate of the line AB divided by the the line BC

Parameters:

point_c : float, the price at point C.

point_b : float, the price at point B.

point_a : float, the price at point A.

Returns: float

line_time_rate(_c, _b, _a) Compute the time rate of the line AB divided by the the line BC

Parameters:

_c : float, the time or bar_index at point C.

_b : float, the time or bar_index at point B.

_a : float, the time or bar_index at point A.

Returns: float

is_inrange(value, min, max) Check if value is within min/max range of tolerance.

Parameters:

value : float, value to check tolerance.

min : float, minimum value in range of tolerance.

max : float, maximum value in range of tolerance.

Returns: bool

isHarmonicTriangle(rate_cba, margin_of_error) Check if the rate(s) correspond to pattern ("Harmonic Triangle").

Parameters:

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

is2Tap(rate_cba, margin_of_error) Check if the rate(s) correspond to pattern ("2Tap", 'Double Top / Bottom').

Parameters:

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

is3Tap(rate_edc, rate_cba, margin_of_error) Check if the rate(s) correspond to pattern ("3Tap", "Triple Top / Bottom").

Parameters:

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

is4Tap(rate_gfe, rate_edc, rate_cba, margin_of_error) Check if the rate(s) correspond to pattern ("4Tap", "Quadruple Top / Bottom").

Parameters:

rate_gfe : float, percent rate of the triangle GFE. expects a negative rate.

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

isABCD(rate_cba, rate_dcb, margin_of_error) Check if the rate(s) correspond to pattern ("AB=CD").

Parameters:

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

rate_dcb : float, percent rate of the triangle DCB. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

isBat(rate_edc, rate_dcb, rate_cba, rate_eda, margin_of_error) Check if the rate(s) correspond to pattern ("Bat").

Parameters:

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_dcb : float, percent rate of the triangle DCB. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

rate_eda : float, percent rate of the triangle EDA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

isButterfly(rate_edc, rate_dcb, rate_cba, rate_eda, margin_of_error) Check if the rate(s) correspond to pattern ("Butterfly").

Parameters:

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_dcb : float, percent rate of the triangle DCB. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

rate_eda : float, percent rate of the triangle EDA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

isGartley(rate_edc, rate_dcb, rate_cba, rate_eda, margin_of_error) Check if the rate(s) correspond to pattern ("Gartley").

Parameters:

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_dcb : float, percent rate of the triangle DCB. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

rate_eda : float, percent rate of the triangle EDA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

isCrab(rate_edc, rate_dcb, rate_cba, rate_eda, margin_of_error) Check if the rate(s) correspond to pattern ("Crab").

Parameters:

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_dcb : float, percent rate of the triangle DCB. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

rate_eda : float, percent rate of the triangle EDA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

isShark(rate_edc, rate_dcb, rate_cba, rate_eda, margin_of_error) Check if the rate(s) correspond to pattern ("Shark").

Parameters:

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_dcb : float, percent rate of the triangle DCB. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

rate_eda : float, percent rate of the triangle EDA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

is5o(rate_edc, rate_dcb, rate_cba, rate_eda, margin_of_error) Check if the rate(s) correspond to pattern ("5o").

Parameters:

rate_edc : float, percent rate of the triangle EDC. expects a negative rate.

rate_dcb : float, percent rate of the triangle DCB. expects a negative rate.

rate_cba : float, percent rate of the triangle CBA. expects a negative rate.

rate_eda : float, percent rate of the triangle EDA. expects a negative rate.

margin_of_error : float, percent rate of expected error margin, default 0.05(5%).

Returns: bool

isWolfe(rate_edc, rate_dcb, rate_cba, rate_eda, margin_of_error) Check if the rate(s) correspond to pattern ("Wolfe").

Parameters: