Ehlers Detrending Filter [CC]The Detrending Filter was created by John Ehlers and this is a complementary indicator to one of my previous scripts:

This indicator builds upon his previous work by attempting to detrend the underlying source data that is used to calculate the final result. He was able to create a leading indicator by removing the trend data and by using his previous calculations to turn the source data into a leading indicator.

There are two ways to understand this indicator. First if the indicator is below the midline then it is in a mid to longterm downtrend and if it is above the midline then it is in a mid to longterm uptrend. Also this indicator shows great promise in predicting future trends so because of that aspect, it may give some false signals from time to time.

I have color coded everything to account for both strong signals and normal signals. Strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other scripts you would like to see me publish!

Detrending

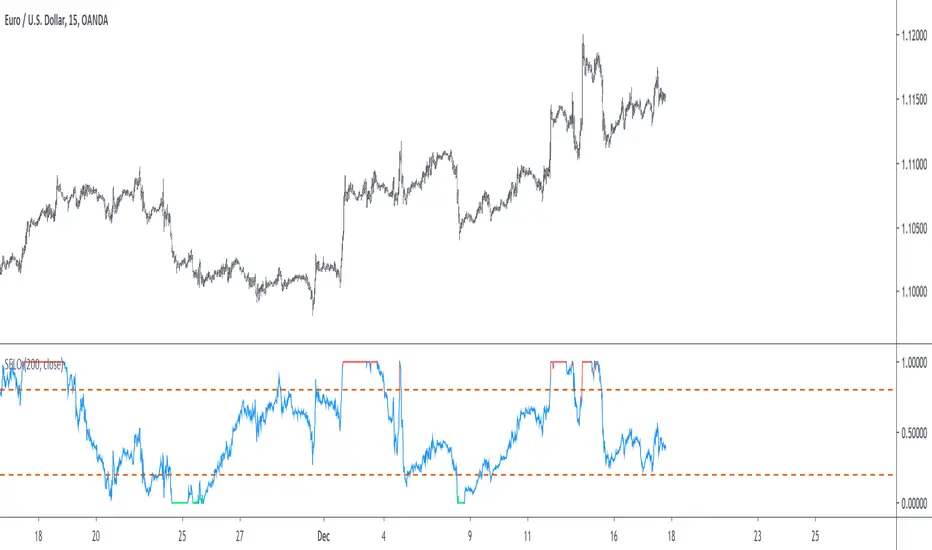

Detrended Ehlers Leading Indicator [CC]The Detrended Ehlers Leading Indicator was created by Bill Mars based off of Ehlers work and this is his attempt to create a leading indicator based on the previous Detrended Synthetic Price . I will be honest that this is a bit of a strange script because it is an indicator based off of the detrended synthetic price which is based off of Ehlers work so I haven't found clear buy and sell signals so I'm open to suggestions. His suggestion for buy and sell signals is to only buy and sell at the indicator crossings but haven't found buy and sell logic that I'm sure about. I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

Detrended Rhythm Oscillator (DRO)How to detect the current "market beat" or market cycle?

A common way to capture the current dominant cycle length is to detrend the price and look for common rhythms in the detrended series. A common approach is to use a Detrended Price Oscillator (DPO). This is done in order to identify and isolate short-term cycles.

A basic DPO description can be found here:

www.tradingview.com

Improvements to the standard DPO

The main purpose of the standard DPO is to analyze historical data in order to observe cycle's in a market's movement. DPO can give the technical analyst a better sense of a cycle's typical high/low range as well as its duration. However, you need to manually try to "see" tops and bottoms on the detrended price and measure manually the distance from low-low or high-high in order to derive a possible cycle length.

Therefore, I added the following improvements:

1) Using a DPO to detrend the price

2) Indicate the turns of the detrended price with a ZigZag lines to better see the tops/bottoms

3) Detrend the ZigZag to remove price amplitude between turns to even better see the cyclic turns ("rhythm")

4) Measure the distance from last detrended zigzag pivot (high-high / low-low) and plot the distance in bars above/below the turn

Now, you can clearly see the rhythm of the dataset indicated by the Detrended Rhythm Oscillator including the exact length between the turns. This makes the procedure to "spot" turns and "measure" distance more simple for the trader.

How to use this information

The purpose is to check if there is a common rhythm or beat in the underlying dataset. To check that, look for recurring pattern in the numbers. E.g. if you often see the same measured distance, you can conclude that there is a major dominant cycle in this market. Also watch for harmonic relations between the numbers. So in the example above you see the highlighted cluster of detected length of around 40,80 and 120. There three numbers all have a harmonic relation to 40.

Once you have this cyclic information, you can use this number to optimize or tune technical indicators based on the current dominant cycle length. E.g. set the length parameter of a technical indicator to the detected harmonic length with the DRO indicator.

Example Use-Case

You can use this information to set the input for the following free public open-source script:

Disclaimer

This is not meant to be a technical indicator on its own and the derived cyclic length should not be used to forecast the next turn per se. The indicator should give you an indication of the current market beat or dominant beats which can be use to further optimize other oscillator or trading related settings.

Options & settings

The indicator allows to plot different versions. It allows to plot the original DPO, the DRO with ZigZag lines, the DRO with detrended ZigZag lines and length labels on/off. You can turn on or off these version in the indicator settings. So you can tweak it visually to your own needs.

[RS]Detrended Percent Price Over Average on RangeExperimental:

Detrended Price oscillator from price against the average inside the range.

Varadi OscillatorThe Varadi Oscillator (VDO) is a leading indicator first proposed by David Varadi and originally aim to reduce the influence of the trend component in oscillators. The DVO can be described as a rolling percent rank of detrended prices over a certain lookback period. The detrending process used for the calculation of the indicator is based on the simple moving average of the ratio between the closing price and median (hl2) price.

Both the length of the percent rank and the moving average used for detrending can be adjusted by the user. We can see that the VDO can lead price movements.

Don't have time to post anything else, if the indicator is too simple, moderators can feel free to remove it and ban me for some time, won't complain.

M waves Mk3 'Magical M's v1

V2

V3

So I forgot this existed so here is the Opened sourced code (pm me for older sorce code there are 600+ Saves)(pm me for other scrips course code too lazy to republish everything)

Changes: Simplified and annotated code/upgraded to v4 format

as always adjust before using

i use this indicator combined with the other frequency one to help me identify time and direction of next move.

Pair with rsi

Pair with detrended tsi (have unpublished script might share later)

‘Redraw’ safe

Slightly detrented(adjustable) to avoid traps

quick how to use:

Meant as and adjustable indicator to “tune" to personal risk/reward preference

Green means buy red means sell

arrow indicators for long term sell and buy

Highly customizable (candles too)

Check out my profile for previous versions they are less customizable but also easier to get started with

similar to rsi you want to buy/sell when the indicator turns green/red and lines are as pinched as posible (the lines that are being filled).

keep an eye on the other line that moves around ;) if its not matching the other 2 moving averages and the main color indicator chances are its a trap(works both ways)

use the candles to help you keep your eye on the indicator when scalping (look at the original post for some color ideas)

Stationary Extrapolated Levels OscillatorIntroduction

The oscillator version of the stationary extrapolated levels indicator. The methodology behind the extrapolated levels where to minimize the risk of making a decision based only on a forecast, therefore the indicator plotted levels in order to determine possible reversal points, signals where generated when the detrended series crossed over/under those levels.

The Indicator

First we detrend the price, this is because forecasting the trend is often harder than a series without trend (stationarity > non-stationarity) , then we forecast the detrended price with a linear extrapolation over a period of length and apply a max/min filter twice to the forecast, the max/min filters are just the highest and lowest function in pine. So the max/min filter have lag length/2 , by applying it two times we have a lag of length which is the period of the forecast. Because we use highest and lowest we can apply min-max normalization in the form of :

x' = (x - min(x, min'))/(max(x,max') - min(x, min'))

where x is the detrended price, max' the highest of the forecast of x and min' the lowest of the forecast of x . This result in a scaled oscillator in a range of (1,0),

When the indicator is equal to 1 or 0 there are high chances of reversals, more in depth this mean that the detrended price have crossed the highest/lowest of the forecast, when the indicator is equal to 0 or 1 for a long time this mean that the forecast was quite inaccurate, you can minimize risk by focusing on the cross between the detrended price and the 0.8/0.2 levels.

Conclusion

I've shown an oscillator version of my previous "Stationary extrapolated levels" indicator, the method involving taking the highest and lowest of the forecast is a great way to minimize the risk involved by time-series forecasting driven decisions. So i hope you find an use to it.

Thanks for reading !

Ehlers Triple Delay-Line DetrenderThis indicator was originally developed by John F. Ehlers (Stocks & Commodities , V.18:7 (July, 2000): "Optimal Detrending").

Mr. Ehlers applied the ideas of the radar systems for the financial time series detrending.

Mr. Ehlers constructed the Triple Delay-Line Canceller first, then smoothed it with the Modified Optimum Elliptic Filter with minimal lag. The smoothed detrended signal is smoothed again with the Modified Optimum Elliptic Filter to obtain signal line.

As result, the crossings of the two indicator lines catch every major cyclic move and the detrender itself can be used as the first step in more sophisticated analyses.