Z-Score Financial Market Conditions | JeffreyTimmermansZ-Score Financial Market Conditions

The Z-Score Financial Market Conditions indicator is a cutting-edge tool for measuring financial market stress and relaxation by combining eight critical financial metrics into a single composite Z-score. This dynamic indicator provides traders and analysts with actionable insights into the overall state of the financial markets, enabling informed decision-making across various trading and investment systems.

Purpose of the Indicator

This indicator serves as a comprehensive gauge of financial market conditions, offering a clear visualization of whether the markets are in a state of stress (elevated risks) or relaxation (normalized conditions). The Z-Score Financial Market Conditions tool is particularly effective for:

Macro-Level Risk Assessment: Identifying periods of high market stress or calmness.

Trend Following Systems: Gauging the market's underlying conditions to validate trends.

Mean Reversion Strategies: Using extreme Z-score levels to detect potential reversals.

Portfolio Risk Management: Adjusting asset exposure based on market-wide financial conditions.

This indicator works exclusively on the 1-day timeframe, as it is calibrated to analyze daily changes in the financial metrics that drive market behavior.

The Eight Key Components and Their Importance

The composite Z-score integrates the Z-scores of the following eight financial metrics. These metrics have been selected for their complementary insights into various aspects of financial market conditions:

VIX (S&P 500 Volatility Index)

Reflects implied volatility in the U.S. equity market.

High VIX values indicate increased uncertainty and risk aversion among market participants.

MOVE (US Treasury Bond Volatility Index)

Captures volatility in U.S. Treasury bonds.

Essential for understanding risk in fixed-income markets, which significantly impact broader economic conditions.

ICE BofA High Yield Option Adjusted Spread (BAMLH0A0HYM2)

Measures the risk premium for high-yield corporate bonds.

Rising spreads suggest increased credit risk and potential economic stress.

ICE BofA Corporate Index Option Adjusted Spread (BAMLC0A0CM)

Tracks credit spreads in the investment-grade bond market.

Helps evaluate the health of higher-quality corporate debt, a key indicator of financial stability.

ICE BofA US High Yield Index Spread (BAMLH0A0HYM2)

Focuses on high-yield U.S. corporate bonds.

Provides localized insights into U.S. credit conditions and risk levels.

CDS (Credit Default Swap Spreads)

Measures the cost of insuring against bond defaults.

Rising CDS spreads signal growing concern over creditworthiness, often a leading indicator of financial stress.

Global Bond Spread (AGG)

Represents global fixed-income spreads.

Offers a broader perspective on international financial conditions beyond the U.S. market.

TED Spread (Treasury-EuroDollar Spread)

The difference between interbank lending rates and short-term U.S. Treasury yields.

Widely regarded as an indicator of systemic risk in the banking sector.

Features and Improvements

This script builds upon the original concept by introducing advanced features to enhance its precision and usability:

Lookback Period Adjustment

A customizable lookback period for Z-score calculations (default: 160 days).

Allows for greater flexibility in adapting to different market conditions.

Moving Average (MA) Smoothing

Optional smoothing of Z-scores using an exponential moving average (EMA) for enhanced clarity.

Default smoothing length: 8 days.

Individual Component Visibility

Plots for individual Z-scores can be enabled or disabled to focus on specific metrics.

Dynamic Background Coloring

Visual cues to indicate bullish (green) or bearish (red) financial conditions based on the composite Z-score.

Custom Inputs

Toggle on/off for each financial metric to tailor the indicator to specific use cases.

Customizable parameters for smoothing and moving averages.

Applications

This indicator is versatile and can be effectively used in various trading systems and strategies:

Long-Term Investment Decision-Making: Assess macroeconomic trends for portfolio rebalancing.

Systematic Trading: Incorporate market conditions into algorithmic models to enhance robustness.

Volatility-Based Strategies: Use Z-score fluctuations to anticipate periods of market turbulence or calm.

Credits

This indicator was inspired by and builds upon the work of TomasOnMarkets . While incorporating significant enhancements, it acknowledges the foundational concepts provided by this original source. Thank you for sharing your input on this important indicator. We are honored to use it and to further improve upon it.

-Jeffrey

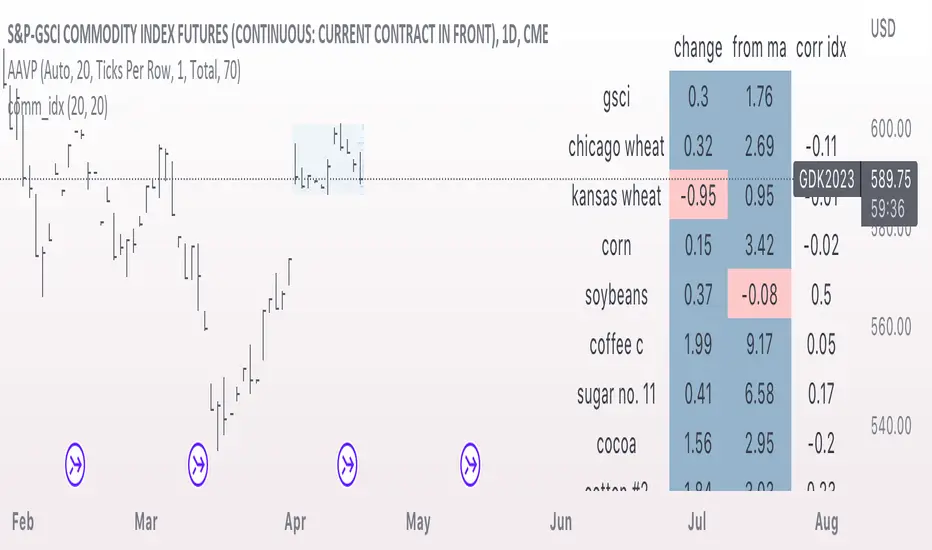

Components

comm_idxThis script displays information about the components of the Goldman Sachs Commodity Index. The index is based on futures contracts in the categories of agricultural products, softs commodities, livestock, energies, industrial metals, and precious metals. The statistics displayed in the table are:

change: 1-day % change

from ma: the % change from a moving average

corr idx: correlation of the contract to the GSCI

The lengths for the moving average and correlation statistic can be set using the inputs.

See the script source for the symbols used for each commodity. Although most of the symbols correspond to the actual futures contract used to compute the index, LME contracts are not available on tradingview. Hence, corresponding HKEX contracts are used for the industrial metals.

Decomposed Average True RangeThis simple script decomposes the value of the Average True Range into a bullish component and a bearish component .

The script supports two plotting methods; Mirrored and Two Lines . If Mirrored is chosen, the indicator plots the bullish component as a positive number, and the bearish component as a negative number. If Two Lines is chosen, the indicator plots two lines, both of positive values. It is the same data, just visualized differently.

Side note: This is very similar to how the strength (average gain) part in the Relative Strength Index calculation works. However, the RSI uses the realized range (close - previous close) rather than true range. If we were to use the bullish component of the ATR as the average bullish gain part in the RSI calculation, and the bearish component of the ATR as the average bearish gain part in the RSI calculation, we would get very similar (but not equal) results to the standard RSI. This shows how the ATR and the RSI are related to each other.

Backtest History Setup 1.0Script of strategy component to setup the backtext lookback. You setup the maximum days back in the history, which will be used for backtest.

Backtesting Period Selector | ComponentDescription

It's nice to quickly be able to set the backtesting period when writing strategies.

To make this process faster I wrote a simple 'component'.

So this is not a strategy but rather code you can plug-into your strategy and use

if you need that specific functionality.

Then it's just a matter of selecting which dates you want to backtest.

You can also chose to color the background to visually show the testing period.

Unfortunately, the background color is fixed at 'blue' for now.

Ps. I like the idea of writing small components to be pluged into other strategies

I'll try to develop this idea a bit further and see how small pieces of code can

easily provide specific functionality to assist and make deving strategies a bit less 'Pineful'.

Usage

First copy the instructed part of the component code over to your strategy.

Next, use the testPeriod() function to limit strategies to the specified backtesting period.

Example usage:

if testPeriod()

strategy.entry("LE", strategy.long)

Todo / Improvements

There are many ways to improve this component and I'm not a very good coder so this is a very crude solutions.

Anyway, here are some things which would be nice to improve:

1. Enable color selection so that the user can choose the background color of his own liking.

2. Improve naming of variables.

3. Test for ilogical choices, such as test period start being at a later date, than test period stop.

4. Account for time zones.

As always, any feedback, corrections or thoughts are very much welcome!

/pbergden