stormytrading orb botshows entries for 15m orb based on 5m break and retest made solely for mnq or nq, works good with smt

shows trades for ldn, nyc, nyc overlap and Asia session, pls follow stormy trading on insta for more

Candlestick analysis

yangwen1.0This script is an initial concept of mine. I attempted to use the 5-minute chart as ticks for catching bottoms and picking tops, but it's unable to avoid whipsaws. I've tested many methods to evade whipsaws, but they ultimately result in poor entry points, causing me to miss the bottoms and tops of price swings. I sincerely hope someone with better approaches can discuss this with me. Thank you.

GraalSTRATEGY DESCRIPTION — “GRAAL”

GRAAL is an advanced algorithmic crypto-trading strategy designed for trend and semi-trend market conditions. It combines ATR-based trend/flat detection, dynamic Stop-Loss and multi-level Take-Profit, break-even (BE) logic, an optional trailing stop, and a “lock-on-trend” mechanism to hold positions until the market structure truly reverses.

The strategy is optimized for Binance, OKX and Bybit (USDT-M and USDC-M futures), but can also be used on spot as an indicator.

Core Logic

Trend Detection — dynamic trend zones built using ATR and local high/low structure.

Entry Logic — positions are opened only after trend confirmation and a momentum-based local trigger.

Exit Logic:

fixed TP levels (TP1/TP2/TP3),

dynamic ATR-based SL,

break-even move after TP1 or TP2,

optional trailing stop.

Lock-on-Trend — positions remain open until an opposite trend signal appears.

Noise Protection — flat filter disables entries during low-volatility conditions.

Key Advantages

Sophisticated and reliable risk-management system.

Minimal false entries due to robust trend filtering.

Optional trailing logic to maximize profit during strong directional moves.

Works well on BTC, ETH and major altcoins.

Easily adaptable for various timeframes (1m–4h).

Supports full automation via OKX / WunderTrading / 3Commas JSON alerts.

Recommended Use Cases

Crypto futures (USDT-M / USDC-M).

Intraday trading (5m–15m–1h).

Swing trading (4h–1D).

Fully automated signal-bot execution.

Important Notes

This is an algorithmic strategy, not financial advice.

Strategy Tester performance may differ from real execution due to liquidity, slippage and fees.

Always backtest and optimize parameters for your specific market and asset.

Recommended Settings: LONG only, no TP, no SL, Flat Policy: Hold, TP3 Mode: Trend, Trailing Stop 1.2%, Fixed size 100 USD, Leverage 10×, ATR=14, HH/LL=36.

Anchor SafeSwing Gold StrategyOverview:

The Anchor SafeSwing Gold Strategy is designed for users who prefer structured, rule-based swing trading on XAUUSD. It focuses on identifying high-quality trade setups rather than frequent entries.

This strategy analyzes the market using multiple technical indicators and methods—including trend analysis, multi-chart confirmation, and support/resistance evaluation—to identify potential swing points. It also incorporates a dynamic approach to risk management through adaptive stop-loss and take-profit logic.

How the Strategy Works

1. Multi-Chart & Trend Analysis:

The strategy evaluates trend direction using several indicators and multiple charts. This helps determine whether the trend favors long or short setups.

2. Buy/Sell Conditions:

a. Buy Conditions: When the broader trend is identified as bullish, the strategy waits for the formation of a strong support zone before considering a long position.

b. Sell Conditions: When the trend is bearish, it waits for a confirmed resistance zone before initiating short positions.

3. Dynamic Take-Profit Logic

The strategy uses adaptive take-profit behavior based on evolving market conditions. It monitors new support/resistance structures and various overbought/oversold signals to dynamically exit trades.

4. Dynamic and Configurable Stop-Loss:

A flexible stop-loss system adjusts according to volatility and market structure.

Users can modify the stop-loss threshold in the settings based on their own risk tolerance and account size.

Trading Frequency :

This strategy focuses on select, high-quality setups. As a result, trade frequency is relatively low and may vary depending on market conditions. Backtesting may show roughly several trades per month, but actual live performance can differ.

Important Notes

All trading involves risk, and users should evaluate the strategy and adjust settings according to their own risk management preferences.

EMA Trend Pro [Hedging & Fixed Risk]

This strategy is a comprehensive trend-following system designed to capture significant market movements while strictly managing risk. It combines multiple Exponential Moving Averages (EMAs) for trend identification, ADX for trend strength filtering, and Volume confirmation to reduce false signals.

Key Features:

Hedging Mode Compatible: The script is designed to handle Long and Short positions independently. This is ideal for markets where trends can reverse quickly or for traders who prefer hedging logic (requires hedging=true in strategy settings).

Professional Risk Management: Unlike standard strategies that use fixed contract sizes, this script calculates Position Size based on Risk. You can define a fixed risk per trade (e.g., 1% of equity or $100 fixed risk). The script automatically adjusts the lot size based on the Stop Loss distance (ATR).

Multi-Stage Take Profit: The strategy scales out positions at 3 different levels (TP1, TP2, TP3) to lock in profits while letting the remaining position ride the trend.

Strategy Logic:

Trend Identification:

Long Entry: EMA 7 > EMA 14 > EMA 21 > EMA 144 (Bullish Alignment).

Short Entry: EMA 7 < EMA 14 < EMA 21 < EMA 144 (Bearish Alignment).

Filters:

ADX Filter: Entries are only taken if ADX (14) > Threshold (default 20) to ensure the market is trending, avoiding chopping ranging markets.

Volume Filter: Current volume must exceed the 20-period SMA volume by 10% to confirm momentum.

Exits & Trade Management:

Stop Loss: Dynamic SL based on ATR (e.g., 1.8x ATR).

Breakeven: Once TP1 is hit, the Stop Loss is automatically moved to Breakeven to protect capital.

Take Profits:

TP1: 1x Risk Distance (30% pos)

TP2: 2x Risk Distance (50% pos)

TP3: 3x Risk Distance (Remaining pos)

Settings Guide:

Risk Type: Choose between "Percent" (of equity) or "Fixed Amount" (USD).

Risk Value: Input your desired risk (e.g., 1.0 for 1% risk).

Fee %: Set your exchange's Taker fee (e.g., 0.05 or 0.06) for accurate backtesting.

ADX Threshold: Adjust to filter out noise (Higher = Stricter trend requirement).

Disclaimer: This script is for educational and backtesting purposes only. Past performance does not guarantee future results. Please use proper risk management.

EMA Trend Pro v5.0 5M ONLY — 策略版(1:1出30%+保本)Here is a clear, professional English description you can copy-paste directly (suitable for sharing with friends, investors, brokers, or posting on TradingView):

EMA Trend Pro v5.0 – Strategy Overview

This is a trend-following strategy designed for 15-minute charts on assets like XAUUSD, NASDAQ, BTC, and ETH.

Entry Rules

Buy when the 7, 14, and 21-period EMAs are aligned upward and the 14-period EMA crosses above the 144-period EMA (with ADX > 20 and volume confirmation).

Sell short when the EMAs are aligned downward and the 14-period EMA crosses below the 144-period EMA.

Risk Management

Initial stop-loss is placed at 1.8 × ATR below (long) or above (short) the entry price.

Position size is calculated to risk a fixed percentage of equity per trade.

Profit-Taking & Trade Management

When price reaches 1:1 reward-to-risk, 30% of the position is closed.

At the same moment, the stop-loss for the remaining 70% is moved to the entry price (breakeven).

The remaining position is split:

50% targets 1:2 reward-to-risk

50% targets 1:3 reward-to-risk (allowing big wins during strong trends)

Visualization

Clean colored bars extend to the right showing entry, stop-loss, and three take-profit levels.

Price labels clearly display "Entry", "SL", "TP1 1:1", "TP2 1:2", and "TP3 1:3".

Only the current trade is displayed for a clean chart.

Key Advantages

High win rate due to breakeven protection after 1R

Excellent reward-to-risk ratio that lets winners run

Fully automated, works on any market with clear trends

Professional look, easy to understand and explain

Perfect for swing traders who want consistent profits with limited downside risk.

Feel free to use this description on TradingView, in your trading journal, or when explaining the strategy to others!

If you want a shorter version (e.g., for TradingView description box) or a Chinese version, just let me know — I’ll give it to you right away! 😊

YCGH Mean Reversion StrategyThis strategy applies a classic mean-reversion framework inspired by the concepts popularized by Ernest P. Chan in his quantitative trading books.

It uses Bollinger Bands and RSI to identify statistically stretched conditions where price has moved too far from its average. When price dips below the lower band with weakening momentum, the strategy accumulates small long positions, expecting reversion toward the mean. As price rebounds above the upper band, it exits positions gradually. Position sizing limits help control risk and avoid excessive exposure.

Special thanks to Ernest P. Chan for his influential work in quantitative trading, which motivated the structure and logic behind this model.

Infinity 26📈 Infinity 26 – Long-Term Investment Signal Indicator

Infinity 26 is a long-term trend-based investment indicator designed to identify high-quality buy and exit points using weekly or monthly candles.

It filters out market noise and focuses only on strong, long-term momentum shifts—making it ideal for wealth creation and slow, steady portfolio growth.

🔹 Key Features

Buy Signals: Automatically highlights strong trend-reversal points where long-term investors can accumulate.

Exit Signals: Shows when the long-term trend weakens, helping protect gains and reduce major drawdowns.

Weekly & Monthly Optimized: Best results when used on 1-week or 1-month timeframe for long-term investing.

Clear Trend Structure: Helps you stay invested during major bull trends and avoid emotional short-term decisions.

Noise-Free: Designed for long-horizon investors—no overtrading, no frequent whipsaws.

🔹 Best For

Long-term investors

Swing-to-position traders

Wealth creation strategies

Portfolio-based investing

🔹 How It Helps You

✔ Avoid wrong entries

✔ Capture major uptrend moves

✔ Reduce risk with timely exits

✔ Build wealth with simple, rule-based signals

Scalping FVG Breakout (3R RR, 時間可調)Scalping

1. Taipei Open Time (time adjustable)

2. First 15mK Bar

3. Risk 1:3

4. Stop Loss

BTC Risk Metric DCA Adapter (3Commas Webhook Strategy)Risk Metric DCA Adapter (3Commas Webhook Strategy) - WORK IN PROGRESS

This Pine Script strategy, originally inspired by the Risk Metric Indicator, is fundamentally engineered as an Adapter to interface with external trading bots like 3Commas via Webhooks. It calculates a dynamic market risk score and translates that score into specific dollar-cost averaging (DCA) entry levels and tiered profit-taking exits.

Key Features & Logic

Risk Metric Calculation (Credit to The Trading Parrot):

The strategy incorporates a complex, multi-timeframe Risk Metric calculation based on daily and weekly moving averages (SMA) and standard deviation (StDev). This metric aims to quantify the current market overextension or compression relative to long-term historical data. The resulting score dictates the level of conviction for a new trade.

Tiered DCA Entry Sizing:

The strategy defines three distinct Buy Levels (L1, L2, L3) corresponding to increasingly favorable (lower) Risk Metric scores.

L1 (Base): Risk is moderate, initiating the minimum defined trade amount.

L2 (Scaled): Risk is low, initiating L1 amount + L2 amount.

L3 (Aggressive): Risk is very low, initiating L1 + L2 + L3 amounts.

Tiered Profit-Taking Exits:

The strategy implements a staggered, partial profit-taking approach based on the Risk Metric rising:

Sell L1 & L2: Closes a percentage of the current position when the Risk Metric reaches defined high thresholds, locking in partial profits.

Sell L3 (Full Exit): Closes the remaining position when the Risk Metric reaches the highest defined threshold.

The Adapter Function (Webhook Integration)

This script is unique because it uses the Pine Script strategy() function to trigger Order Fills, which are necessary to access powerful placeholders in the TradingView alert system.

Trigger Type: The alert must be set to trigger on Any order fill.

Dynamic Webhook Data: Instead of using fixed alert() commands, the strategy generates dynamic labels (e.g., BUY_ENTRY_L3_USD_1000 or SELL_L1_PCT_25) using the strategy.entry and strategy.close commands.

Data Transfer: The alert message then uses the placeholder {{strategy.order.comment}} to pass these dynamic labels to the 3Commas bot, allowing the bot to execute the precise action (e.g., start_deal_with_volume_in_quote_currency or close_deal_at_market_percentage).

Full Strategy Webhook payload

{

"secret": "YOUR_3COMMAS_SECRET_KEY",

"max_lag": "300",

"timestamp": "{{timenow}}",

"trigger_price": "{{close}}",

"tv_exchange": "{{exchange}}",

"tv_instrument": "{{ticker}}",

"action": "{{strategy.order.action}}",

"bot_uuid": "YOUR_BOT_UUID",

"strategy_info": {

"market_position": "{{strategy.market_position}}",

"market_position_size": "{{strategy.market_position_size}}",

"prev_market_position": "{{strategy.prev_market_position}}",

"prev_market_position_size": "{{strategy.prev_market_position_size}}"

},

"order": {

"amount": "{{strategy.order.contracts}}",

"currency_type": "base",

"comment": "{{strategy.order.comment}}"

}

}

Disclaimer: This script is an adapter tool and does not guarantee profit. Trading requires manual configuration of risk settings, bot parameters, and adherence to platform-specific setup instructions.

V15.0 Adaptive Chameleon [Pro]

# **V15.0 Adaptive Chameleon – Strategy Description**

**Adaptive Chameleon** is a fully automated TradingView strategy powered by a signal engine based on multi-timeframe trend analysis, adaptive moving averages, and a volatility filter. The goal is to trade in the direction of a strong and confirmed trend, avoid opening trades in weak or manipulative price zones, and establish positions with a clearly defined risk/reward ratio.

---

## **1. General Logic and Philosophy**

The strategy divides tasks between two timeframes:

* **4-Hour Chart → Trend Manager (Boss)**

Determines the direction and strength of the trend.

* **4-Minute Chart → Entry Trigger (Operating Unit)**

Generates the ideal entry signal in the direction of the trend.

Thanks to this structure, the strategy both follows the long-term main direction and finds clear entries with low lag on smaller timeframes.

---

## **2. Trend Detection (4H)**

The strategy uses **KAMA (Kaufman Adaptive Moving Average)** and **ADX** to identify trends on the higher timeframe.

### **KAMA – Adaptive Trend Line**

* The KAMA is much more "smart" than traditional moving averages.

* It accelerates during price movements and decelerates during sideways movements.

* This allows for much clearer detection of trend direction.

### **ADX – Trend Strength Meter**

The strategy only opens trades when **trend strength** is rising (above the ADX average).

This prevents unnecessary trades when the trend is weak.

### **Trend Rules**

* Price above the KAMA → **Uptrend**

* Price below the KAMA → **Downtrend**

* ADX widening → **Trend strong**

The entry trigger is activated when these three conditions are met together.

---

## **3. Entry Engine (45m)**

On the 45-minute timeframe, the system uses the following components:

### **AlphaTrend (MFI + ATR-Based Adaptive Line)**

* Measures market flow direction with MFI (Money Flow Index),

* Measures price level breakouts with ATR (Volatility).

AlphaTrend detects whether the price is likely to reverse upwards or downwards.

### **Entry Signal**

* **Buy signal:** If the AlphaTrend has reversed upwards based on recent bars

* **Sell signal:** If the AlphaTrend has broken downwards

### **Pivot Points (For Stop)**

* The **pivotLow** and **pivotHigh** levels of the last 10 bars are calculated.

* These are used to determine the most logical stop distance.

---

## **4. Protection Shields**

The strategy uses two main filters to protect against the most dangerous conditions in the crypto market:

### **1. Pump/Dump Filter**

* A candlestick length greater than 4% is considered a "pump bar."

* Never open a trade on these bars.

The goal: to avoid sudden manipulation candlesticks.

### **2. RSI Filter**

* Long trades: RSI > 45 (open long on weak momentum)

* Short trades: RSI < 55 (open short on extremely strong momentum)

These filters provide more balanced entries.

---

## **5. Final Entry Conditions**

### **All conditions are required simultaneously for long:**

1. 4H trend up

2. ADX trend strength increasing

3. 45m AlphaTrend issued a "buy" signal

4. RSI > 45

5. No candlestick pump

6. Date range is suitable

### **All conditions apply in the opposite direction for short.**

---

## **6. Exit Mechanism (Stop, TP, Trailing)**

The strategy uses a three-layer structure on the exit side:

### **1. Pivot-Based Stop**

* Stop distance = Entry price − Pivot Low (for long)

* Minimum stop distance = **1% of the price**

Provides both structural and mathematical security.

### **2. Fixed R:R (Default 1:2)**

* TP = Entry + Stop Distance × R:R

The default 2R target is ideal for trend systems.

### **3. Optional Trailing Stop**

* Dynamic trailing stop that follows the price by a certain percentage.

* Allows trend trades to yield greater profits.

---

## **7. Chart Displays**

* Purple line:** 4H WEDGE (main trend line)

* Yellow background:** Pump protection is active (trades will not be opened on that bar)

---

## **8. Practical Effect of the Strategy**

This system has an adaptive structure based on trend variations.

**Strengths:**

* Very high accuracy (76–80% in SOL and ETH tests)

* Low drawdown (approximately 6–7%)

* Safe entries thanks to pump/dump and extreme momentum filters

* Clearly defined stop and target structure

* Low noise thanks to multi-timeframe compatibility

**Weaknesses:**

* Performance may decrease in sideways markets without trends

* Overtrading may occur if the ADX filter is closed

* Very small stops can sometimes cause unnecessary triggers

---

## **9. Conclusion**

**Adaptive Chameleon** is a trend-based and highly stable strategy with well-established risk management, manipulation filtering, and entry into lower timeframes with clear trend direction detection and low-latency signals.

SOL and ETH demonstrated strong and balanced performance in backtests with metrics such as:

* **600+ trades**

* **30–37% profit**

* **76–80% win rate**

* **Low max drawdown**

Dami's HMA Strategy"Dami's HMA Strategy: Dynamic Crossover with Momentum Filter"

Key Points to Include:

Foundation: The strategy is based on the Hull Moving Average (HMA), noted for its speed and reduced lag, making it ideal for identifying trend inflection points early.

Enhanced Logic: Unlike a simple moving average crossover, this strategy incorporates a momentum filter. A signal is only triggered if the HMA crossover coincides with a candle moving in the direction of the new trend (bullish candle for Long, bearish candle for Short). This aims to confirm the impulse and avoid false entries during consolidation periods or 'weak' crossovers.

100% Market Coverage System: It is a continuous reversal system. Every new signal (Long or Short) closes the opposite position, ensuring the trader is always positioned in the direction indicated by the HMA.

Complementary Visualization: It includes the 8-Period High/Low Bands (Dami's Bands) to provide visual context of the recent price range, although they do not affect trading orders.

Adjustment and Optimization: The HMA length (hma_len=9 by default) is the key parameter to optimize based on the specific pair and timeframe. Higher values will generate fewer signals and be slower, while lower values (like the current 9) make it more sensitive.

Simple MA Crossover w/ SLTPPicture two cheetahs on a racetrack made of price candles. One cheetah is fast and twitchy (the short-term EMA). The other is chill, lumbering, and takes its sweet time (the long-term EMA). When the twitchy cheetah sprints ahead and crosses above the chill one → “BUY, YOU MAGNIFICENT DEGEN!” When the twitchy one gets tired, slows down, and gets lapped from above → “SELL before this turns into a horror movie!”

That, my friend, is the EMA crossover strategy in its purest, most dramatic form.

15m ORB + FVG Strategy (ChadAnt)Core Logic

The indicator's logic revolves around three main phases:

1. Defining the 15-Minute Opening Range (ORB)

The script calculates the highest high (rangeHigh) and lowest low (rangeLow) that occurred during the first 15 minutes of the trading day.

This time window is defined by the sessionStr input, which defaults to 0930-0945 (exchange time).

The high and low of this range are plotted as small gray dots once the session ends (rangeSet = true).

2. Identifying a Fair Value Gap (FVG) Setup

After the 15-minute range is set, the indicator waits for a breakout of either the range high or range low.

A "Strict FVG breakout" requires two conditions on the first candle that closes beyond the range:

The candle before the breakout candle ( bars ago) must have been inside the range.

The breakout candle ( bar ago) must have closed outside the range.

A Fair Value Gap (FVG) must form on the most recent three candles (the current bar and the two previous bars).

Bullish FVG (Long Setup): The low of the current bar (low) is greater than the high of the bar two periods prior (high ). This FVG represents a price inefficiency that the trade expects to fill.

Bearish FVG (Short Setup): The high of the current bar (high) is less than the low of the bar two periods prior (low ).

If a valid FVG setup occurs, the indicator marks a pending setup and draws a colored box to highlight the FVG area (Green for Bullish FVG, Red for Bearish FVG).

3. Trade Entry and Management

If a pending setup is identified, the trade is structured as a re-entry trade into the FVG zone:

Entry Price: Set at the outer boundary of the FVG, which is the low of the current bar for a Long setup, or the high of the current bar for a Short setup.

Stop Loss (SL): Set at the opposite boundary of the FVG, which is the low for a Long setup, or the high for a Short setup.

The trade is triggered (tradeActive = true) once the price retraces to the pendingEntry level.

Risk/Reward (RR) Targets: Three Take Profit (TP) levels are calculated based on the distance between the Entry and Stop Loss:

$$\text{Risk} = | \text{Entry} - \text{SL} |$$

$$\text{TP}n = \text{Entry} \pm (\text{Risk} \times \text{RR}n)$$

where $n$ is 1, 2, or 3, corresponding to the input $\text{RR}1$, $\text{RR}2$, and $\text{RR}3$ values (defaults: 1.0, 1.5, and 2.0).

Trade Lines: Upon triggering, lines for the Entry, Stop Loss, and three Take Profit levels are drawn on the chart for a specified length (lineLength).

A crucial feature is the directional lock (highBroken / lowBroken):

If the price breaks a range level (e.g., simpleBrokeHigh) but without a valid FVG setup, the corresponding directional flag (e.g., highBroken) is set to true permanently for the day.

This prevents the indicator from looking for any subsequent trade setups in that direction for the rest of the day, suggesting that the initial move, without an FVG, exhausted the opportunity.

Open-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

ChadAnt

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied

Risk-Managed StrategyRisk-Managed Strategy is a complete algorithmic trading framework that blends multiple technical systems—RSI, MACD, EMA crossover, Bollinger Bands, and SuperTrend—into a unified signal engine.

The script dynamically calculates position size based on capital, risk percentage, ATR-based stop loss, and reward-ratio targets.

It features:

-Multi-indicator signal voting (BUY / SELL / NEUTRAL)

- Dynamic capital tracking across trades

- Automatic position sizing based on risk amount

- Auto-generated Stop Loss and Take Profit using recent highs/lows

- On-chart SL, TP, and CMP plotting for clarity

This strategy is designed for traders who want a professional, rule-based system that balances accuracy, risk control, and automation.

Disclaimer:

The information provided is for educational and informational purposes only. It does not constitute financial or investment advice. Trading and investing in stocks involves risk, including the possible loss of capital. Any decisions to buy, sell, or hold securities are the sole responsibility of the reader. Past performance is not indicative of future results. Always do your own research and, if necessary, consult with a licensed financial advisor before making investment decisions.

Macketings 1min ScalpingThis is a hyper-reactive scalping strategy designed for the 1-minute chart. It utilizes a strict four-EMA hierarchy (80/90/340/500) to ensure trades are only taken in the strongest aligned market trend. The strategy is built to be extremely tight on risk and focuses on capturing the immediate, high-momentum swing that follows a confirmed EMA retest or breakout.

Key Mechanics (How it Works):

Strict Trend Alignment: Entry is only permitted when the faster EMA band (80/90) and the price action are correctly aligned with the slow trend (340/500).

Long: EMA 80/90 must be above EMA 340/500, AND EMA 340 must be above EMA 500. (And vice-versa for Short.)

Expanded Retest Entry: The strategy waits for the price to retest or briefly enter the 80/90 band, then immediately enters upon the confirmed momentum breakout from that band.

Dynamic Risk Management (Tight Ride): The strategy is engineered to ride the wave aggressively while protecting capital immediately:

Extremely Tight Initial Stop Loss (0.2% default): Limits initial risk instantly.

Break-Even Security: Once profit hits 0.3%, the Stop Loss is automatically trailed to secure 0.2% profit (a risk-free trade).

Aggressive Exit Logic: Positions are closed not only upon hitting the Take Profit target (2.5%) but also immediately if the 80/90 EMA band crosses the 340 EMA, signaling a critical loss of momentum.

Disclaimer:

This strategy requires high-liquidity instruments and is best used on low timeframes (1-minute) due to its dependency on fast momentum shifts and tight stops. Backtesting and forward testing are crucial before deployment.

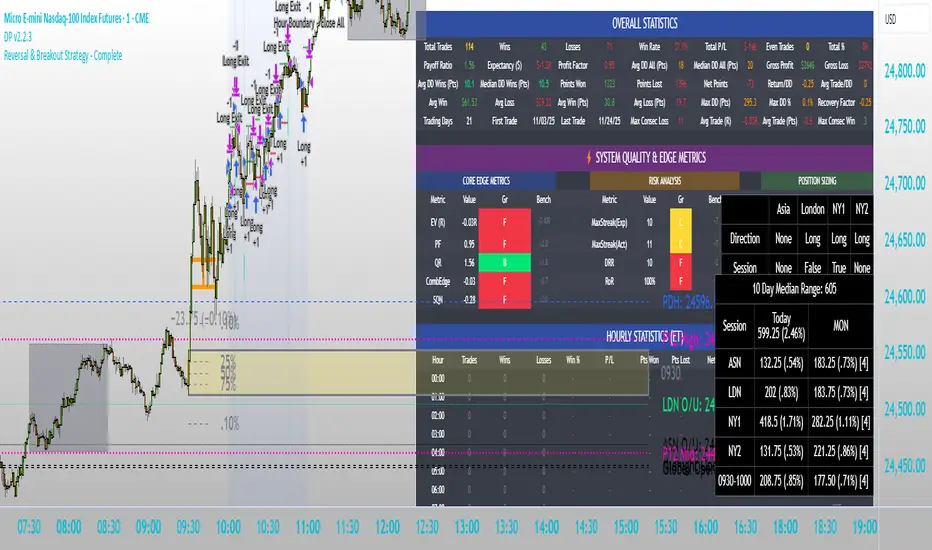

Intraday Market Structure Research Tool (Reversal + Breakout)This script is a fully rule-based intraday strategy designed for research and backtesting purposes, not financial advice. It is intended to help traders study market behavior, time-based price patterns, and statistical trade outcomes under realistic trading assumptions.

What the Strategy Does

This strategy operates in two selectable trade modes:

1. Reversal Mode

Identifies statistically large candles relative to recent volatility

Enters counter-direction trades when price shows exhaustion behavior

Designed to study fade-type behavior around session extremes

2. Breakout Mode

Tracks recent swing highs/lows over a user-defined lookback

Executes trades only after confirmed price expansion beyond these levels

Designed to test momentum continuation behavior

Time & Session Filtering

Trades are only taken during user-defined market sessions, including:

New York 1

New York 2

London

Asia

This allows users to analyze performance differences between global trading sessions.

9:30 AM Opening Range Logic

The script captures the 9:30 AM (Eastern) one-minute candle high/low and uses that as an Opening Range:

Breakout trades can be confirmed above or below this range

The range is visualized for clarity

Risk Management & Realism Controls

This script includes realistic execution mechanics:

Fixed stop-loss and take-profit defined by the user (points or ticks)

Built-in slippage modeling

Commission assumptions included

Position sizing designed to keep risk per trade under 5–10% of account equity when used with realistic account sizes

Users are responsible for choosing realistic account sizes and risk values when running backtests.

Statistical Performance Tracking

The strategy records and displays performance data including:

Win rate

Average win and loss

Maximum drawdown per trade series

Expectancy

Trade distribution by:

Time of day

Session

Market classification

This allows users to study market tendencies and structural behavior over large sample sizes.

Visual Tools

The script displays:

Entry and exit markers

Blocked trade labels (when conditions are not met)

Opening range box

Breakout levels

Use Case Disclaimer

This script is designed for:

Backtesting

Market structure research

Statistical study

It is not guaranteed to be profitable, and results depend heavily on user-selected settings, market conditions, and realistic brokerage assumptions.

Premarket Breakout (TP1 → BE → ATR Trail)this is the best ever you will really like i t and it does a lot its a really good scirpt please use it to make trades

Premarket Breakout (TP1 → BE → ATR Trail)the best one you can find a very good indicator and strategy to help with al l trading needs in every way

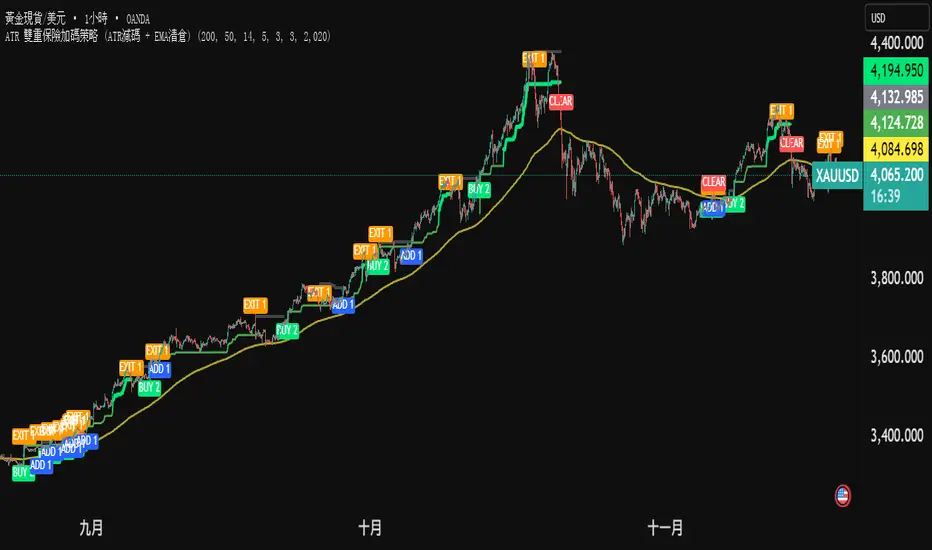

ATR 雙重保險加碼策略 (ATR減碼 + EMA清倉) (三寶爸黃金版)黃金雙保險戰法 (兩口單策略)

核心概念: 進場買兩口。一口賺了就跑(保本),一口死抱到底(拚大賺)。

1. 進場 (買 2 口):

只要價格站上黃線,而且突破前高。

別猶豫,直接買 2 口。

2. 減碼 (賣 1 口):

價格回檔碰到綠線。

代表短線轉弱,先賣掉 1 口。

好處: 錢先放口袋,心裡踏實。

3. 加碼 (買回 1 口):

如果你手上只剩 1 口,結果行情沒死,又創新高。

代表剛才賣錯了,趕快買回 1 口 (補回滿倉)。

好處: 繼續跟著趨勢賺錢。

4. 清倉 (全跑):

價格跌破黃線。

代表趨勢真的結束了,不管剩幾口,全部賣掉。

一句話總結: 「震盪時先賣一半保命,趨勢噴出時永遠滿倉在車上。」

Gold Dual-Insurance Tactic (2-Lot System)

Core Concept: Enter with 2 lots. Sell one early to lock in profits (Play Safe), and hold the other to catch the big wave (Go Big).

1. Entry (Buy 2 Lots):

When price is above the Yellow Line AND breaks the previous High.

Don't hesitate. Buy 2 lots immediately.

2. Scale Out (Sell 1 Lot):

When price pulls back and hits the Green Line.

This means short-term weakness. Sell 1 lot.

Benefit: Put money in your pocket. Peace of mind.

3. Add Position (Buy Back 1 Lot):

If you have only 1 lot left, but the market hits a New High.

It means the trend is alive. Quickly Buy back 1 lot (refill to full position).

Benefit: Continue maximizing profits with the trend.

4. Clear All (Exit Everything):

When price falls below the Yellow Line.

The trend is officially over. Sell everything, no matter what.

CyberG TestTesting the ability to test scripts. I have been working on multiple scripts I want to show my stats for, for possible interests in my scripts