Bitcoin Weekend FadeThis indicator is a tool for setting a bias based on weekend price movements, with the assumption that the crypto market often experiences stronger moves over the weekend due to thinner order books. It helps identify potential fade opportunities, suggesting that price movements from Saturday and Sunday may reverse during the weekdays.

How to use:

Sets a bias based on weekend price action.

Sets a bias based on weekend price action.

Use weekday price action for confirmation before acting on the bias.

Best suited for range-bound markets, where the price tends to revert to the mean.

Avoid fading high-timeframe breakouts, as they often indicate strong trends.

Bitcoin (Kriptopara)

PORTFOLIO TABLE Simple [Titans_Invest]PORTFOLIO TABLE Simple

This is a simple table for you to monitor your assets or cryptocurrencies in your SPOT wallet without needing to access your broker’s website or wallet app.

⯁ HOW TO USE THIS TABLE❓

You only need to select the asset and enter the amount of each one.

The table will show how much you have of each asset and the total value of your portfolio.

You’ll be able to monitor up to 39 assets in real time.

⯁ CONVERT VALUES

You can also activate and select a currency for conversion.

For example, cryptocurrency assets are calculated in US dollars, but you can select euros as the conversion currency.

The values originally in dollars will then be displayed in euros.

⯁ Track your Portfolio in real time:

⯁ Add your local Currency to Convert Values:

⯁ Follow your Portfolio Live:

___________________________________________________________

📜 SCRIPT : PORTFOLIO TABLE Simple

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

___________________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

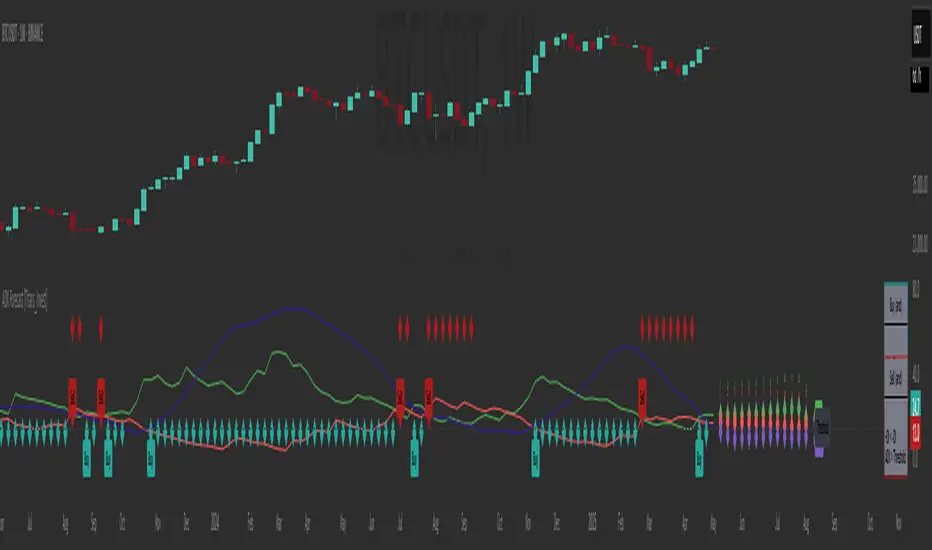

ADX Forecast [Titans_Invest]ADX Forecast

This isn’t just another ADX indicator — it’s the most powerful and complete ADX tool ever created, and without question the best ADX indicator on TradingView, possibly even the best in the world.

ADX Forecast represents a revolutionary leap in trend strength analysis, blending the timeless principles of the classic ADX with cutting-edge predictive modeling. For the first time on TradingView, you can anticipate future ADX movements using scientifically validated linear regression — a true game-changer for traders looking to stay ahead of trend shifts.

1. Real-Time ADX Forecasting

By applying least squares linear regression, ADX Forecast projects the future trajectory of the ADX with exceptional accuracy. This forecasting power enables traders to anticipate changes in trend strength before they fully unfold — a vital edge in fast-moving markets.

2. Unmatched Customization & Precision

With 26 long entry conditions and 26 short entry conditions, this indicator accounts for every possible ADX scenario. Every parameter is fully customizable, making it adaptable to any trading strategy — from scalping to swing trading to long-term investing.

3. Transparency & Advanced Visualization

Visualize internal ADX dynamics in real time with interactive tags, smart flags, and fully adjustable threshold levels. Every signal is transparent, logic-based, and engineered to fit seamlessly into professional-grade trading systems.

4. Scientific Foundation, Elite Execution

Grounded in statistical precision and machine learning principles, ADX Forecast upgrades the classic ADX from a reactive lagging tool into a forward-looking trend prediction engine. This isn’t just an indicator — it’s a scientific evolution in trend analysis.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the ADX, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an ADX time series like this:

Time →

ADX →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted ADX, which can be crossed with the actual ADX to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public ADX with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining ADX with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

ADX Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first ADX indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE ADX❓

The Average Directional Index (ADX) is a technical analysis indicator developed by J. Welles Wilder. It measures the strength of a trend in a market, regardless of whether the trend is up or down.

The ADX is an integral part of the Directional Movement System, which also includes the Plus Directional Indicator (+DI) and the Minus Directional Indicator (-DI). By combining these components, the ADX provides a comprehensive view of market trend strength.

⯁ HOW TO USE THE ADX❓

The ADX is calculated based on the moving average of the price range expansion over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and has three main zones:

• Strong Trend: When the ADX is above 25, indicating a strong trend.

• Weak Trend: When the ADX is below 20, indicating a weak or non-existent trend.

• Neutral Zone: Between 20 and 25, where the trend strength is unclear.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 +DI > -DI

🔹 +DI < -DI

🔹 +DI > ADX

🔹 +DI < ADX

🔹 -DI > ADX

🔹 -DI < ADX

🔹 ADX > Threshold

🔹 ADX < Threshold

🔹 +DI > Threshold

🔹 +DI < Threshold

🔹 -DI > Threshold

🔹 -DI < Threshold

🔹 +DI (Crossover) -DI

🔹 +DI (Crossunder) -DI

🔹 +DI (Crossover) ADX

🔹 +DI (Crossunder) ADX

🔹 +DI (Crossover) Threshold

🔹 +DI (Crossunder) Threshold

🔹 -DI (Crossover) ADX

🔹 -DI (Crossunder) ADX

🔹 -DI (Crossover) Threshold

🔹 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 +DI > -DI

🔸 +DI < -DI

🔸 +DI > ADX

🔸 +DI < ADX

🔸 -DI > ADX

🔸 -DI < ADX

🔸 ADX > Threshold

🔸 ADX < Threshold

🔸 +DI > Threshold

🔸 +DI < Threshold

🔸 -DI > Threshold

🔸 -DI < Threshold

🔸 +DI (Crossover) -DI

🔸 +DI (Crossunder) -DI

🔸 +DI (Crossover) ADX

🔸 +DI (Crossunder) ADX

🔸 +DI (Crossover) Threshold

🔸 +DI (Crossunder) Threshold

🔸 -DI (Crossover) ADX

🔸 -DI (Crossunder) ADX

🔸 -DI (Crossover) Threshold

🔸 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : ADX Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Spent Output Profit Ratio Z-Score | Vistula LabsOverview

The Spent Output Profit Ratio (SOPR) Z-Score indicator is a sophisticated tool designed by Vistula Labs to help cryptocurrency traders analyze market sentiment and identify potential trend reversals. It leverages on-chain data from Glassnode to calculate the Spent Output Profit Ratio (SOPR) for Bitcoin and Ethereum, transforming this metric into a Z-Score for easy interpretation.

What is SOPR?

Spent Output Profit Ratio (SOPR) measures the profit ratio of spent outputs (transactions) on the blockchain:

SOPR > 1: Indicates that, on average, coins are being sold at a profit.

SOPR < 1: Suggests that coins are being sold at a loss.

SOPR = 1: Break-even point, often seen as a key psychological level.

SOPR provides insights into holder behavior—whether they are locking in profits or cutting losses—making it a valuable gauge of market sentiment.

How It Works

The indicator applies a Z-Score to the SOPR data to normalize it relative to its historical behavior:

Z-Score = (Smoothed SOPR - Moving Average of Smoothed SOPR) / Standard Deviation of Smoothed SOPR

Smoothed SOPR: A moving average (e.g., WMA) of SOPR over a short period (default: 30 bars) to reduce noise.

Moving Average of Smoothed SOPR: A longer moving average (default: 180 bars) of the smoothed SOPR.

Standard Deviation: Calculated over a lookback period (default: 200 bars).

This Z-Score highlights how extreme the current SOPR is compared to its historical norm, helping traders spot significant deviations.

Key Features

Data Source:

Selectable between BTC and ETH, using daily SOPR data from Glassnode.

Customization:

Moving Average Types: Choose from SMA, EMA, DEMA, RMA, WMA, or VWMA for both smoothing and main averages.

Lengths: Adjust the smoothing period (default: 30) and main moving average length (default: 180).

Z-Score Lookback: Default is 200 bars.

Thresholds: Set levels for long/short signals and overbought/oversold conditions.

Signals:

Long Signal: Triggered when Z-Score crosses above 1.02, suggesting potential upward momentum.

Short Signal: Triggered when Z-Score crosses below -0.66, indicating potential downward momentum.

Overbought/Oversold Conditions:

Overbought: Z-Score > 2.5, signaling potential overvaluation.

Oversold: Z-Score < -2.0, indicating potential undervaluation.

Visualizations:

Z-Score Plot: Teal for long signals, magenta for short signals.

Threshold Lines: Dashed for long/short, solid for overbought/oversold.

Candlestick Coloring: Matches signal colors.

Arrows: Green up-triangles for long entries, red down-triangles for short entries.

Background Colors: Magenta for overbought, teal for oversold.

Alerts:

Conditions for Long Opportunity, Short Opportunity, Overbought, and Oversold.

Usage Guide

Select Cryptocurrency: Choose BTC or ETH.

Adjust Moving Averages: Customize types and lengths for smoothing and main averages.

Set Thresholds: Define Z-Score levels for signals and extreme conditions.

Monitor Signals: Use color changes, arrows, and background highlights to identify opportunities.

Enable Alerts: Stay informed without constant chart watching.

Interpretation

High Z-Score (>1.02): SOPR is significantly above its historical mean, potentially indicating overvaluation or strong bullish momentum.

Low Z-Score (<-0.66): SOPR is below its mean, suggesting undervaluation or bearish momentum.

Extreme Conditions: Z-Scores above 2.5 or below -2.0 highlight overbought or oversold markets, often preceding reversals.

Conclusion

The SOPR Z-Score indicator combines on-chain data with statistical analysis to provide traders with a clear, actionable view of market sentiment. Its customizable settings, visual clarity, and alert system make it an essential tool for both novice and experienced traders seeking an edge in the cryptocurrency markets.

Bitcoin Monthly Seasonality [Alpha Extract]The Bitcoin Monthly Seasonality indicator analyzes historical Bitcoin price performance across different months of the year, enabling traders to identify seasonal patterns and potential trading opportunities. This tool helps traders:

Visualize which months historically perform best and worst for Bitcoin.

Track average returns and win rates for each month of the year.

Identify seasonal patterns to enhance trading strategies.

Compare cumulative or individual monthly performance.

🔶 CALCULATION

The indicator processes historical Bitcoin price data to calculate monthly performance metrics

Monthly Return Calculation

Inputs:

Monthly open and close prices.

User-defined lookback period (1-15 years).

Return Types:

Percentage: (monthEndPrice / monthStartPrice - 1) × 100

Price: monthEndPrice - monthStartPrice

Statistical Measures

Monthly Averages: ◦ Average return for each month calculated from historical data.

Win Rate: ◦ Percentage of positive returns for each month.

Best/Worst Detection: ◦ Identifies months with highest and lowest average returns.

Cumulative Option

Standard View: Shows discrete monthly performance.

Cumulative View: Shows compounding effect of consecutive months.

Example Calculation (Pine Script):

monthReturn = returnType == "Percentage" ?

(monthEndPrice / monthStartPrice - 1) * 100 :

monthEndPrice - monthStartPrice

calcWinRate(arr) =>

winCount = 0

totalCount = array.size(arr)

if totalCount > 0

for i = 0 to totalCount - 1

if array.get(arr, i) > 0

winCount += 1

(winCount / totalCount) * 100

else

0.0

🔶 DETAILS

Visual Features

Monthly Performance Bars: ◦ Color-coded bars (teal for positive, red for negative returns). ◦ Special highlighting for best (yellow) and worst (fuchsia) months.

Optional Trend Line: ◦ Shows continuous performance across months.

Monthly Axis Labels: ◦ Clear month names for easy reference.

Statistics Table: ◦ Comprehensive view of monthly performance metrics. ◦ Color-coded rows based on performance.

Interpretation

Strong Positive Months: Historically bullish periods for Bitcoin.

Strong Negative Months: Historically bearish periods for Bitcoin.

Win Rate Analysis: Higher win rates indicate more consistently positive months.

Pattern Recognition: Identify recurring seasonal patterns across years.

Best/Worst Identification: Quickly spot the historically strongest and weakest months.

🔶 EXAMPLES

The indicator helps identify key seasonal patterns

Bullish Seasons: Visualize historically strong months where Bitcoin tends to perform well, allowing traders to align long positions with favorable seasonality.

Bearish Seasons: Identify historically weak months where Bitcoin tends to underperform, helping traders avoid unfavorable periods or consider short positions.

Seasonal Strategy Development: Create trading strategies that capitalize on recurring monthly patterns, such as entering positions in historically strong months and reducing exposure during weak months.

Year-to-Year Comparison: Assess how current year performance compares to historical seasonal patterns to identify anomalies or confirmation of trends.

🔶 SETTINGS

Customization Options

Lookback Period: Adjust the number of years (1-15) used for historical analysis.

Return Type: Choose between percentage returns or absolute price changes.

Cumulative Option: Toggle between discrete monthly performance or cumulative effect.

Visual Style Options: Bar Display: Enable/disable and customize colors for positive/negative bars, Line Display: Enable/disable and customize colors for trend line, Axes Display: Show/hide reference axes.

Visual Enhancement: Best/Worst Month Highlighting: Toggle special highlighting of extreme months, Custom highlight colors for best and worst performing months.

The Bitcoin Monthly Seasonality indicator provides traders with valuable insights into Bitcoin's historical performance patterns throughout the year, helping to identify potentially favorable and unfavorable trading periods based on seasonal tendencies.

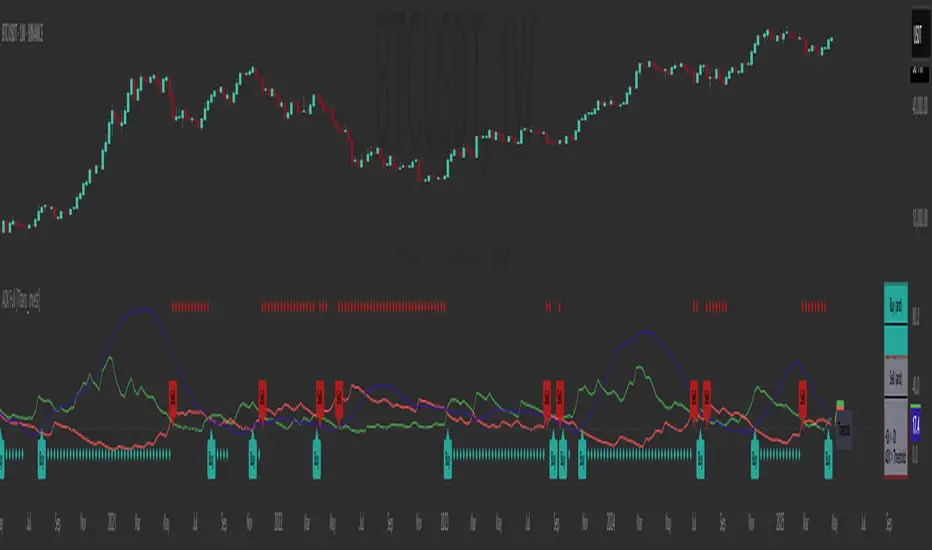

ADX Full [Titans_Invest]ADX Full

This is, without a doubt, the most complete ADX indicator available on TradingView — and quite possibly the most advanced in the world. We took the classic ADX structure and fully optimized it, preserving its essence while elevating its functionality to a whole new level. Every aspect has been enhanced — from internal logic to full visual customization. Now you can see exactly what’s happening inside the indicator in real time, with tags, flags, and informative levels. This indicator includes over 22 long entry conditions and 22 short entry conditions , covering absolutely every possibility the ADX can offer. Everything is transparent, adjustable, and ready to fit seamlessly into any professional trading strategy. This isn’t just another ADX — it’s the definitive ADX, built for traders who take the market seriously.

⯁ WHAT IS THE ADX❓

The Average Directional Index (ADX) is a technical analysis indicator developed by J. Welles Wilder. It measures the strength of a trend in a market, regardless of whether the trend is up or down.

The ADX is an integral part of the Directional Movement System, which also includes the Plus Directional Indicator (+DI) and the Minus Directional Indicator (-DI). By combining these components, the ADX provides a comprehensive view of market trend strength.

⯁ HOW TO USE THE ADX❓

The ADX is calculated based on the moving average of the price range expansion over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and has three main zones:

Strong Trend: When the ADX is above 25, indicating a strong trend.

Weak Trend: When the ADX is below 20, indicating a weak or non-existent trend.

Neutral Zone: Between 20 and 25, where the trend strength is unclear.

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 +DI > -DI

🔹 +DI < -DI

🔹 +DI > ADX

🔹 +DI < ADX

🔹 -DI > ADX

🔹 -DI < ADX

🔹 ADX > Threshold

🔹 ADX < Threshold

🔹 +DI > Threshold

🔹 +DI < Threshold

🔹 -DI > Threshold

🔹 -DI < Threshold

🔹 +DI (Crossover) -DI

🔹 +DI (Crossunder) -DI

🔹 +DI (Crossover) ADX

🔹 +DI (Crossunder) ADX

🔹 +DI (Crossover) Threshold

🔹 +DI (Crossunder) Threshold

🔹 -DI (Crossover) ADX

🔹 -DI (Crossunder) ADX

🔹 -DI (Crossover) Threshold

🔹 -DI (Crossunder) Threshold

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 +DI > -DI

🔸 +DI < -DI

🔸 +DI > ADX

🔸 +DI < ADX

🔸 -DI > ADX

🔸 -DI < ADX

🔸 ADX > Threshold

🔸 ADX < Threshold

🔸 +DI > Threshold

🔸 +DI < Threshold

🔸 -DI > Threshold

🔸 -DI < Threshold

🔸 +DI (Crossover) -DI

🔸 +DI (Crossunder) -DI

🔸 +DI (Crossover) ADX

🔸 +DI (Crossunder) ADX

🔸 +DI (Crossover) Threshold

🔸 +DI (Crossunder) Threshold

🔸 -DI (Crossover) ADX

🔸 -DI (Crossunder) ADX

🔸 -DI (Crossover) Threshold

🔸 -DI (Crossunder) Threshold

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : ADX Full

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Global M2 Money Supply Top20 + Offset & WaveThe M2 Top20 is a global aggregation of the M2 money supply from the 20 largest economies in the world , providing a comprehensive view of the total liquidity in the global financial system. It is expressed in trillions of USD.

This script calculates and visualizes the M2 Money Supply of the Top 20 Global Economies, adjusted to various timeframes (4H, 1D, 1W, 1M) with customizable offset adjustments (in days) from -1000 days to +1000 days. This indicator includes data from the Americas, Europe, Africa, and the Asia Middle East , offering a diverse and balanced representation of major economic regions. The M2 of each country has been converted to USD.

Additionally, the user can set a minimum and maximum offset to create a wave around the main offset and expand the comparison.

Combining these options, this indicator enables users to visualize a range of the global money supply, making it useful for market analysis, economic forecasting, and understanding macroeconomic trends. This indicator is particularly valuable for traders and analysts interested in understanding the dynamics of global monetary systems and their potential impact on financial markets.

Key Features:

Global M2 Money Supply calculation from the Top 20 Economies.

Adjustable Offset: Adjust the offset to align the indicator with the best bar. Adjustment in days, usable on different timeframes (1D, 1W, 4H, 1M).

Wave Projection: Displays a "probability cloud"—a smoothed area that shows the probable path of Bitcoin, derived from shifts in global liquidity.

Min/Max Offset Adjustments: Customizable offsets allow you to determine the range of future windows, helping to shape the wave and better identify liquidity-driven turning points.

Use Cases:

Economic Forecasting: Identify trends in global money supply and their potential market impact (e.g., historically leads Bitcoin price by +/- 78 days to +/-108 days).

Market Analysis: Track the growth or contraction of money supply across key economies.

Macro-Economic Analysis: Understand the relationship between monetary policies and market performance.

How to use:

Add the indicator to your chart.

Set the timeframe to 1D to customize the offset.

Set the Offset (in days).

Set the Offset Range Minimum and Maximum.

Show/Hide the Range Wave

.

Use offset = 0 to have the indicator align directly with the current data, without any shift, providing a baseline for comparison with the most recent market conditions.

Countries included in the M2 Top20:

China (CN), Japan (JP), South Korea (KR), Hong Kong (HK), Taiwan (TW), India (IN), Saudi Arabia (SA), Thailand (TH), Vietnam (VN), United Arab Emirates (AE), Malawi (MW) – Africa, United States (US), Canada (CA), Brazil (BR), Mexico (MX), Eurozone (EU), United Kingdom (GB), Russia (RU), Poland (PL), Switzerland (CH).

These countries were selected from the ranking of the World Economy Indicator of Trading View .

Global M2 [BizFing]MARKETSCOM:BITCOIN ECONOMICS:USM2

This is an indicator designed to show the correlation between the global M2 money supply and Bitcoin.

This indicator basically provides a Global M2 index by summing the M2 money supply data from the United States, South Korea, China, Japan, the EU, and the United Kingdom.

Furthermore, it is configured to allow you to add or remove the M2 data of desired countries within the settings.

I hope this proves to be a small aid in predicting the future price of Bitcoin.

If you have any questions or require any improvements while using it, please feel free to contact me.

Thank you.

BTC Price-Volume Efficiency Z-Score (PVER-Z)Overview:

This PVER-Z Score measures Bitcoin’s price movement efficiency relative to trading volume, normalized using a Z-Score over a long-term 200-day period.

It highlights statistically rare inefficiencies, helping investors spot extreme accumulation and distribution zones for systematic SDCA strategies.

Concept:

- Measures how efficiently price has moved relative to the volume that supported it over a long historical window (Default 200 days) but can be adjustable.

- It compares cumulative price changes vs cumulative volume flow.

- Then normalizes those inefficiencies using Z-Score statistics.

How It Works:

1. Calculates the absolute daily price change divided by volume (price-volume efficiency ratio).

2. Applies EMA smoothing to remove noisy fluctuations.

3. Normalizes the result into a Z-Score to detect statistically significant outliers.

4. Plots dynamic heatmap colors as the efficiency score moves through different deviation zones.

5. Background fills appear when the Z-Score moves beyond ±2 to ±3 SD, signaling rare macro opportunities.

Why is Bitcoin price rising while PVER-Z is falling toward green zone?

1. PVER-Z is not just "price" — it's price change relative to volume. PVER-Z measures how efficient the price movement is relative to volume. It's not "price going up" or "price going down" directly. It's how unusual or inefficient the price versus volume relationship is, compared to its historical average.

2. A rising Bitcoin price + weak efficiency = PVER-Z falls.

If Bitcoin rises but volume is super strong (normal buying volume), no problem, the PVER-Z stays normal. If Bitcoin rises but with very weak volume support, PVER-Z falls.

***Usage Notes***:

- Best used on the daily timeframe or higher.

- When the Z-Score enters the green zone (-2 to -3 SD), it signals a historically rare accumulation zone — favoring long-term buying for SDCA.

- When the Z-Score enters the red zone (+2 to +3 SD), it signals overextended distribution — caution recommended.

- Designed strictly for mean-reversion analysis, no trend-following signals.

- The red zone on a proper Z chart would be -2SD to -3SD and +2SD to +3SD for the green zone. At the time of publishing I do not know how to adjust the values on the indicator itself. The red zone at -2SD is actually +2 Standard Deviations on a Z Score SD Chart. (overbought zone).

- Your green zone at +2SD is actually -2SD Standard Deviations (oversold zone).

- Built manually with no reliance on built-in indicators

- Designed for Bitcoin on the 1D, 3D, or Weekly timeframes. NOT for intraday trading.

- DO NOT SOELY RELY ON THIS INDICATOR FOR YOUR LONG TERM VALUATION. I AM NOT RESPONSIBLE FOR YOUR FINANICAL ASSETS.

M2 Liqudity WaveGlobal Liquidity Wave Indicator (M2-Based)

The Global Liquidity Wave Indicator is designed to track and visualize the impact of global M2 liquidity on risk assets—especially those highly correlated to monetary expansion, like Bitcoin, MSTR, and other macro-sensitive equities.

Key features include:

Leading Signal: Historically leads Bitcoin price action by approximately 70 days, offering traders and analysts a forward-looking edge.

Wave-Based Projection: Visualizes a "probability cloud"—a smoothed band representing the most likely trajectory for Bitcoin based on changes in global liquidity.

Min/Max Offset Controls: Adjustable offsets let you define the range of lookahead windows to shape the wave and better capture liquidity-driven inflection points.

Explicit Offset Visualization: Option to manually specify an exact offset to fine-tune the overlay, ideal for testing hypotheses or aligning with macro narratives.

Macro Alignment: Particularly effective for assets with high sensitivity to global monetary policy and liquidity cycles.

This tool is not just a chart overlay—it's a lens into the liquidity engine behind the market, helping anticipate directional bias in advance of price moves.

How to use?

- Enable the indicator for BTCUSD.

- Set Offset Range Start and End to 70 and 115 days

- Set Specific Offset to 78 days (this can change so you'll need to play around)

FAQ

Why a global liquidity wave?

The global liquidity wave accounts for variability in how much global liquidity affects an underlying asset. Think of the Global Liquidity Wave as an area that tracks the most probable path of Bitcoin, MSTR, etc. based on the total global liquidity.

Why the offset?

Global liquidity takes time to make its way into assets such as #Bitcoin, Strategy, etc. and there can be many reasons for that. It's never a specific number of days of offset, which is why a global liquidity wave is helpful in tracking probable paths for highly correlated risk assets.

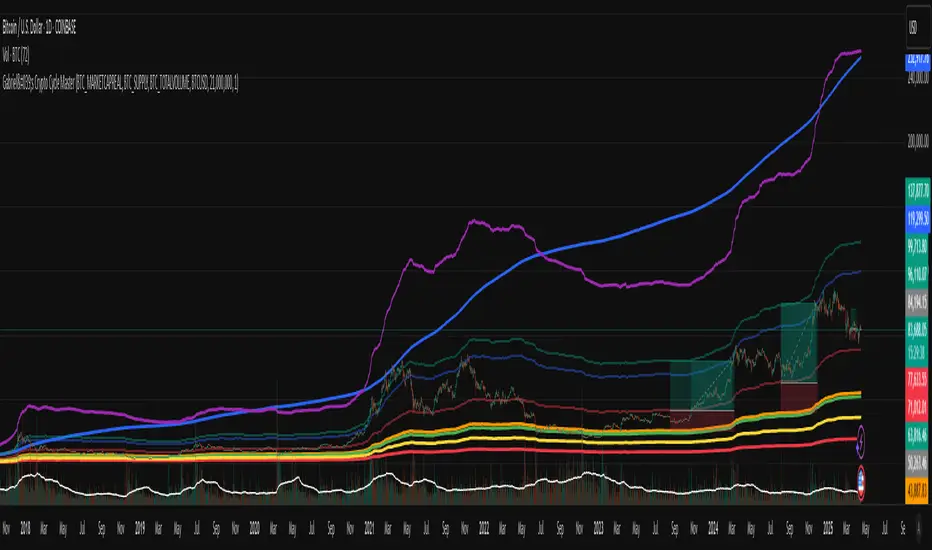

Gabriel's Crypto Cycle Master [Multi-Asset]🧠 Gabriel's Crypto Cycle Master

Gabriel’s Crypto Cycle Master is a comprehensive macro valuation tool designed to identify long-term accumulation and distribution zones for any crypto asset using custom on-chain and price-based models.

🔹 Fully Multi-Asset Support

Manually input full tickers from COINMETRICS, GLASSNODE, or INDEX to track:

Realized Market Cap

On-chain Supply

Total Transaction Volume

USD-denominated Price

🔹 Core Metrics Modeled

This script computes major macroeconomic valuation layers based on widely researched concepts:

Realized Price – Network's cost basis

Top Cap – 35× average historical cap

Delta Top – Gap between Realized Price and Average Cap

CVDD – Cumulative Value Days Destroyed

Terminal Price – Network floor based on age and velocity

Balanced Price – Realized minus Terminal (via regression)

🔹 Advanced Bands for Over/Undervaluation

Around Realized Price, this tool dynamically plots:

Golden Ratio Band (×φ) — "Warm Zone" undervaluation

Euler's e Band (×e) — "Caution Zone" deeper value

Pi Band (×π) — "Overheated" zone when crossed upward

🔹 Built-in Alerts

Alerts fire when:

Price crosses below or above any band

Price drops under Terminal Price

Price recovers above the network floor

🔹 Ideal For

Long-term crypto cycle investors

On-chain analysts

DCA accumulation and distribution timing

Macro-level Bitcoin or ETH valuation zones

⚙️ Setup

Manually enter tickers for Market Cap, Supply, Volume, and Price for your preferred crypto asset.

Adjust CVDD cap (21M for BTC, ~120M for ETH) if analyzing a different coin.

Enable/disable specific valuation layers and alert bands via checkboxes.

Built by OneWallStreetQuant | Dynamic adaptation by Gabriel

Published for educational and cycle analysis use — not financial advice.

Ideal for Daily Charts, since the estimate formula was created on that timeframe.

Reversal Strength Meter – Adib NooraniThe Reversal Strength Meter is an oscillator designed to identify potential reversal zones based on supply and demand dynamics. It uses smoothed stochastic logic to reduce noise and highlight areas where momentum may be weakening, signaling possible market turning points.

🔹 Smooth, noise-reduced stochastic oscillator

🔹 Custom zones to highlight potential supply and demand imbalances

🔹 Non-repainting, compatible across all timeframes and assets

🔹 Visual-only tool — intended to support discretionary trading decisions

This oscillator assists scalpers and intraday traders in tracking subtle shifts in momentum, helping them identify when a market may be preparing to reverse — always keeping in mind that trading is based on probabilities, not certainties.

📘 How to Use the Indicator Efficiently

For Reversal Trading:

Buy Setup

– When the blue line dips below the 20 level, wait for it to re-enter above 20.

– Look for reversal candlestick patterns (e.g., bullish engulfing, hammer, or morning star).

– Enter above the pattern’s high, with a stop loss below its low.

Sell Setup

– When the blue line rises above the 80 level, wait for it to re-enter below 80.

– Look for bearish candlestick patterns (e.g., bearish engulfing, inverted hammer, or evening star).

– Enter below the pattern’s low, with a stop loss above its high.

🛡 Risk Management Guidelines

Risk only 0.5% of your capital per trade

Book 50% profits at a 1:1 risk-reward ratio

Trail the remaining 50% using price action or other supporting indicators

Reversal Scalping Ribbon - Adib NooraniThe Reversal Scalping Ribbon is a trend-following overlay tool designed to visually identify potential reversal zones based on price extremes and dynamic volatility bands. It calculates adaptive upper and lower bands using price action and custom ATR logic, helping traders quickly assess market direction and possible turning points

🔹 Volatility-adjusted bands based on price highs/lows

🔹 Color-coded ribbons to indicate trend bias and potential reversal shifts

🔹 No repainting, works on all timeframes and assets

🔹 Visual-only display, no trade signals — supports discretion-based entries

This ribbon is designed for scalpers and intraday traders to spot reversal setups with clarity. It enhances your trading by showing real-time market bias without unnecessary distractions. By focusing on probabilities, it helps to improve decision-making in fast-paced environments

How to use the indicator efficiently

For Reversal Trading:

Buy: When price closes below the green ribbon with a red candle, then re-enters with a green candle. Enter above the high of the green candle with a stop loss below the lowest low of the recent green/red candles

Sell: When price closes above the red ribbon with a green candle, then re-enters with a red candle. Enter below the low of the red candle with a stop loss above the highest high of the recent red/green candles

Risk Management:

Limit risk to 0.5% of your capital per trade

Take 50% profit at a 1:1 risk-reward ratio

For the remaining 50%, trail using the lower edge of the green band for buys and the upper edge of the red band for sells

Volumen trend indicator 5MVOLUMEN TREND INDICATOR

Introduction

This indicator on TradingView provides a combination of technical analysis through a data table and visual elements on the chart. Its purpose is to provide a comprehensive view of the analyzed asset, facilitating decision-making.

How It Works

The indicator operates on two levels:

Data Table:

Displays key information about the asset's trend.

Includes metrics such as the current price, percentage change, volatility, and other relevant variables.

Can be customized to include additional indicators as needed.

Provides a quick analysis without the need to interpret complex charts.

Technical Elements on the Chart:

Incorporates dynamic support and resistance lines.

Can include moving averages, Bollinger Bands, RSI, or other custom indicators.

Offers visual alerts for significant changes in the asset's trend.

Facilitates detailed technical analysis through direct observation of patterns and signals.

Default Technical Indicators

The indicator comes with the following default pre-configured technical indicators:

Exponential Moving Average (EMA) 9:

This EMA responds more quickly to price movements, making it ideal for identifying short-term trends. It is generally used to detect crossovers with other EMAs or prices and is considered an entry or exit signal.

Exponential Moving Average (EMA) 21:

The 21-period EMA is used to identify medium-term trends. Its interaction with the 9 EMA is key to confirming buy or sell signals when both cross.

RSI (Relative Strength Index):

It is used to measure the magnitude of recent gains and losses of an asset, helping to identify overbought or oversold conditions.

Bollinger Bands:

These bands help identify volatility levels and potential reversal points. Price touching the upper or lower bands can be an important signal of trend change or continuation.

Customization

The user can modify several aspects of the indicator, such as:

Colors and styles of visual elements on the chart.

Types of indicators to include in the table.

Configuration of alerts and notifications.

Time interval for calculations and data updates.

EMA values (the periods can be changed if other configurations are desired).

Recommended Usage

To make the most of the indicator:

Use the data table to get an overview of the asset.

Analyze the technical elements on the chart to confirm trends.

Set alerts to avoid missing key opportunities.

Compare the information with other indicators and data sources before making decisions.

Precautions and Best Practices

Avoid relying solely on the indicator: Complement it with other technical and fundamental analysis.

Adjust the settings according to the asset's volatility: Not all strategies work the same across different markets.

Don’t overload the chart with too many elements: This can create visual noise and confusion in interpretation.

Test it on a demo account before trading live: To familiarize yourself with the indicator's functionality and adjustments.

----------------------------------------------

Remember that no system is perfect, keep these considerations in mind for this indicator:

Do not trade when a signal appears during an opposite trend:

Do not trade when the market is uncertain in its direction or within a parallel channel:

Relative Crypto Dominance Polar Chart [LuxAlgo]The Relative Crypto Dominance Polar Chart tool allows traders to compare the relative dominance of up to ten different tickers in the form of a polar area chart, we define relative dominance as a combination between traded dollar volume and volatility, making it very easy to compare them at a glance.

🔶 USAGE

The use is quite simple, traders just have to load the indicator on the chart, and the graph showing the relative dominance will appear.

The 10 tickers loaded by default are the major cryptocurrencies by market cap, but traders can select any ticker in the settings panel.

Each area represents dominance as volatility (radius) by dollar volume (arc length); a larger area means greater dominance on that ticker.

🔹 Choosing Period

The tool supports up to five different periods

Hourly

Daily

Weekly

Monthly

Yearly

By default, the tool period is set on auto mode, which means that the tool will choose the period depending on the chart timeframe

timeframes up to 2m: Hourly

timeframes up to 15m: Daily

timeframes up to 1H: Weekly

timeframes up to 4H: Monthly

larger timeframes: Yearly

🔹 Sorting & Sizing

Traders can sort the graph areas by volatility (radius of each area) in ascending or descending order; by default, the tickers are sorted as they are in the settings panel.

The tool also allows you to adjust the width of the chart on a percentage basis, i.e., at 100% size, all the available width is used; if the graph is too wide, just decrease the graph size parameter in the settings panel.

🔹 Set your own style

The tool allows great customization from the settings panel, traders can enable/disable most of the components, and add a very nice touch with curved lines enabled for displaying the areas with a petal-like effect.

🔶 SETTINGS

Period: Select up to 5 different time periods from Hourly, Daily, Weekly, Monthly and Yearly. Enable/disable Auto mode.

Tickers: Enable/disable and select tickers and colors

🔹 Style

Graph Order: Select sort order

Graph Size: Select percentage of width used

Labels Size: Select size for ticker labels

Show Percent: Show dominance in % under each ticker

Curved Lines: Enable/disable petal-like effect for each area

Show Title: Enable/disable graph title

Show Mean: Enable/disable volatility average and select color

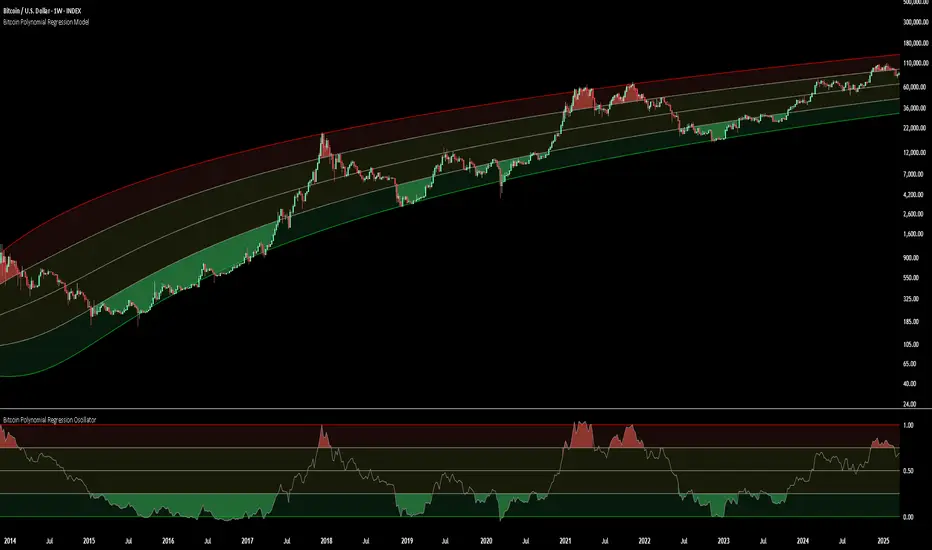

Bitcoin Polynomial Regression ModelThis is the main version of the script. Click here for the Oscillator part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines. The Oscillator version can be found here.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Bitcoin Polynomial Regression OscillatorThis is the oscillator version of the script. Click here for the other part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

M2SL/DXY RatioThis is the ratio of M2 money supply (M2SL) to the U.S. dollar index (DXY), taking into account the impact of U.S. dollar strength and weakness on liquidity.

M2SL/DXY better represents the current impact of the United States on cryptocurrency prices.

Global M2 Money Supply (USD) GrowthThe Global M2 Growth indicator evaluates the total liquid money supply, including cash, checking deposits, and assets that can be easily converted to cash. It reflects changes in global liquidity by tracking year-on-year (YoY) changes in the Global M2 money supply rather than its absolute value. This approach highlights the velocity of liquidity expansion or contraction, offering a clearer understanding of its correlation with asset performance, such as Bitcoin.

How It Works

When the Global M2 money supply expands, it reflects an increase in available liquidity. This often leads to an influx of capital into higher-yielding and riskier assets like Bitcoin, equities, and commodities. Conversely, when M2 contracts, liquidity tightens, leading to declines in the values of these assets.

An essential insight is that Bitcoin's price is not immediately affected by changes in M2. Research shows a lag of approximately 56-60 days (around two months) between liquidity changes and Bitcoin's price movements. Shifting the liquidity data forward by this period improves the correlation between Global M2 and Bitcoin performance.

How to Use

Track Global M2 YoY Change: Focus on liquidity's yearly change to identify trends. Rapid increases in liquidity often signify favorable conditions for Bitcoin and other risk assets to rise, while contractions often predict price declines or consolidation phases.

Account for the Lag Effect: Incorporate the two-month lag into your analysis to predict Bitcoin's potential moves more accurately. For instance, a recent resurgence in liquidity growth could signal a Bitcoin rally within the next two months.

Use as a Macro Indicator: Monitor liquidity trends alongside other economic indicators and asset performance metrics to build a more comprehensive investment framework.

By tracking these dynamics, traders and investors can better anticipate Bitcoin's trajectory and make informed decisions.

Economic Crises by @zeusbottradingEconomic Crises Indicator by @zeusbottrading

Description and Use Case

Overview

The Economic Crises Highlight Indicator is designed to visually mark major economic crises on a TradingView chart by shading these periods in red. It provides a historical context for financial analysis by indicating when major recessions occurred, helping traders and analysts assess the performance of assets before, during, and after these crises.

What This Indicator Shows

This indicator highlights the following major economic crises (from 1953 to 2020), which significantly impacted global markets:

• 1953 Korean War Recession

• 1957 Monetary Tightening Recession

• 1960 Investment Decline Recession

• 1969 Employment Crisis

• 1973 Oil Crisis

• 1980 Inflation Crisis

• 1981 Fed Monetary Policy Recession

• 1990 Oil Crisis and Gulf War Recession

• 2001 Dot-Com Bubble Crash

• 2008 Global Financial Crisis (Great Recession)

• 2020 COVID-19 Recession

Each of these periods is shaded in red with 80% transparency, allowing you to clearly see the impact of economic downturns on various financial assets.

How This Indicator is Useful

This indicator is particularly valuable for:

✅ Comparative Performance Analysis – It allows traders and investors to compare how different assets (e.g., Gold, Silver, S&P 500, Bitcoin) performed before, during, and after major economic crises.

✅ Identifying Market Trends – Helps recognize recurring patterns in asset price movements during times of financial distress.

✅ Risk Management & Strategy Development – Understanding how markets reacted in the past can assist in making better-informed investment decisions for future downturns.

✅ Gold, Silver & Bitcoin as Safe Havens – Comparing precious metals and cryptocurrencies against traditional stocks (e.g., SPY) to analyze their performance as hedges during economic turmoil.

How to Use It in Your Analysis

By overlaying this indicator on your Gold, Silver, SPY, and Bitcoin chart (for example), you can quickly spot historical market reactions and use that insight to predict possible behaviors in future downturns.

⸻

How to Apply This in TradingView?

1. Click on Use on chart under the image.

2. Overlay it with Gold ( OANDA:XAUUSD ), Silver ( OANDA:XAGUSD ), SPY ( AMEX:SPY ), and Bitcoin ( COINBASE:BTCUSD ) for comparative analysis.

⸻

Conclusion

This indicator serves as a powerful historical reference for traders analyzing asset performance during economic downturns. By studying past crises, you can develop a data-driven investment strategy and improve your market insights. 🚀📈

Let me know if you need any modifications or enhancements!

Ragi's 24h volumeThis script is a TradingView Pine Script indicator that displays the 24-hour trading volume for a given asset. It provides both the native volume of the asset and, if the asset is not already listed on Binance, also displays the 24-hour volume from Binance (if applicable). Here's a breakdown of the key components:

Volume Calculation:

It sums the volume data over different time frames: 1-minute, 5-minute (for daily charts), or 60-minute intervals.

The volume is calculated based on the asset's volume type (either "quote" volume or a calculated value of close * volume).

For crypto assets, if the volume data is unavailable, it raises an error.

Binance Volume:

If the asset is not from Binance, the script fetches 24-hour volume data from Binance for that symbol, ensuring it is using the correct currency rate.

Display:

The indicator displays a table with the 24-hour volume in the chosen position on the chart (top, middle, or bottom).

The table displays the current exchange's volume, and if applicable, the Binance volume.

The volume is color-coded based on predefined thresholds:

Attention: Displays a warning color for volumes exceeding the attention level.

Warning: Shows an alert color for volumes above the warning threshold.

Normal: Displays in standard color when the volume is lower than the warning level.

The text and background color are customizable, and users can adjust the text size and position of the table.

User Inputs:

The script allows customization of table text size, position, background color, and volume thresholds for attention and warning.

In summary, this indicator is designed to track and display 24-hour volume on a chart, with additional volume information from Binance if necessary, and provides visual cues based on volume levels to help traders quickly assess trading activity.

Crypto Fear & Greed Score [Underblock]Crypto Fear & Greed Score - Methodology & Functioning

Introduction

The Crypto Fear & Greed Score is a comprehensive indicator designed to assess market sentiment by detecting extreme conditions of panic (fear) and euphoria (greed). By combining multiple technical factors, it helps traders identify potential buying and selling opportunities based on the emotional state of the market.

This indicator is highly customizable, allowing users to adjust weight parameters for RSI, volatility, Bitcoin dominance, and trading volume, making it adaptable to different market conditions.

Key Components

The indicator consists of two primary sub-scores:

Fear Score (Panic) - Measures the intensity of fear in the market.

Greed Score (Euphoria) - Measures the level of overconfidence and excessive optimism.

The difference between these two values results in the Net Score, which indicates the dominant market sentiment at any given time.

1. Relative Strength Index (RSI)

The indicator utilizes multiple RSI timeframes to measure momentum and overbought/oversold conditions:

RSI 1D (Daily) - Captures medium-term sentiment shifts.

RSI 4H (4-hour) - Identifies short-term market movements.

RSI 1W (Weekly) - Helps detect long-term overbought/oversold conditions.

2. Volatility Analysis

High volatility is often associated with fear and panic-driven selling.

Low volatility in bullish markets may indicate complacency and overconfidence.

3. Bitcoin Dominance (BTC.D)

Bitcoin dominance provides insights into capital flow between Bitcoin and altcoins:

Rising BTC dominance suggests fear as investors move into BTC for safety.

Declining BTC dominance indicates increased risk appetite and potential market euphoria.

4. Buying and Selling Volume

The indicator analyzes both buying and selling volume, ensuring a clearer confirmation of market sentiment.

High buying volume in uptrends reinforces bullish momentum.

Spikes in selling volume indicate panic and possible market bottoms.

Calculation Methodology

The indicator allows users to adjust weight parameters for each component, making it adaptable to different trading strategies. The formulas are structured as follows:

Fear Score (Panic Calculation)

Fear Score = (1 - RSI_1D) * W_RSI1D + (1 - RSI_4H) * W_RSI4H + (1 - Dominance) * W_Dominance + Volatility * W_Volatility + Sell Volume * W_SellVolume

Greed Score (Euphoria Calculation)

Greed Score = RSI_1D * W_RSI1D + RSI_4H * W_RSI4H + Dominance * W_Dominance + (1 - Volatility) * W_Volatility + Buy Volume * W_BuyVolume

Net Fear & Greed Score

Net Score = (Greed Score - Fear Score) * 100

Interpretation:

Above 70: Extreme greed -> possible overbought conditions.

Below -70: Extreme fear -> potential buying opportunity.

Near 0: Neutral market sentiment.

Trend Reversal Detection

The indicator includes two moving averages for enhanced trend detection:

Short-term SMA (50-periods) - Reacts quicklier to changes in sentiment.

Long-term SMA (200-periods) - Captures broader trend reversals.

How Crossovers Work:

Short SMA crossing above Long SMA -> Potential bullish reversal.

Short SMA crossing below Long SMA -> Possible bearish trend shift.

Alerts for SMA crossovers help traders act on momentum shifts in real-time.

Customization and Visualization

The Net Score dynamically changes color: green for greed, red for fear.

Users can adjust weightings directly from settings, avoiding manual script modifications.

Reference levels at 70 and -70 provide clarity on extreme market conditions.

Conclusion

The Crypto Fear & Greed Score provides a powerful and objective measure of market sentiment, helping traders navigate extreme conditions effectively.

🟢 If the Net Score is below -70, panic may present a buying opportunity.

🔴 If the Net Score is above 70, excessive euphoria may indicate a selling opportunity.

⚖️ Neutral values suggest a balanced market sentiment.

By customizing weight parameters and utilizing trend reversal alerts, traders can gain a deeper insight into market psychology and make more informed trading decisions. 🚀

Cash And Carry Arbitrage BTC Compare Month 6 by SeoNo1Detailed Explanation of the BTC Cash and Carry Arbitrage Script

Script Title: BTC Cash And Carry Arbitrage Month 6 by SeoNo1

Short Title: BTC C&C ABT Month 6

Version: Pine Script v5

Overlay: True (The indicators are plotted directly on the price chart)

Purpose of the Script

This script is designed to help traders analyze and track arbitrage opportunities between the spot market and futures market for Bitcoin (BTC). Specifically, it calculates the spread and Annual Percentage Yield (APY) from a cash-and-carry arbitrage strategy until a specific expiry date (in this case, June 27, 2025).

The strategy helps identify profitable opportunities when the futures price of BTC is higher than the spot price. Traders can then buy BTC in the spot market and short BTC futures contracts to lock in a risk-free profit.

1. Input Settings

Spot Symbol: The real-time BTC spot price from Binance (BTCUSDT).

Futures Symbol: The BTC futures contract that expires in June 2025 (BTCUSDM2025).

Expiry Date: The expiration date of the futures contract, set to June 27, 2025.

These inputs allow users to adjust the symbols or expiry date according to their trading needs.

2. Price Data Retrieval

Spot Price: Fetches the latest closing price of BTC from the spot market.

Futures Price: Fetches the latest closing price of BTC futures.

Spread: The difference between the futures price and the spot price (futures_price - spot_price).

The spread indicates how much higher (or lower) the futures price is compared to the spot market.

3. Time to Maturity (TTM) and Annual Percentage Yield (APY) Calculation

Current Date: Gets the current timestamp.

Time to Maturity (TTM): The number of days left until the futures contract expires.

APY Calculation:

Formula:

APY = ( Spread / Spot Price ) x ( 365 / TTM Days ) x 100

This represents the annualized return from holding a cash-and-carry arbitrage position if the trader buys BTC at the spot price and sells BTC futures.

4. Display Information Table on the Chart

A table is created on the chart's top-right corner showing the following data:

Metric: Labels such as Spread and APY

Value: Displays the calculated spread and APY

The table automatically updates at the latest bar to display the most recent data.

5. Alert Condition

This sets an alert condition that triggers every time the script runs.

In practice, users can modify this alert to trigger based on specific conditions (e.g., APY exceeds a threshold).

6. Plotting the APY and Spread

APY Plot: Displays the annualized yield as a blue line on the chart.

Spread Plot: Visualizes the futures-spot spread as a red line.

This helps traders quickly identify arbitrage opportunities when the spread or APY reaches desirable levels.

How to Use the Script

Monitor Arbitrage Opportunities:

A positive spread indicates a potential cash-and-carry arbitrage opportunity.

The larger the APY, the more profitable the arbitrage opportunity could be.

Timing Trades:

Execute a buy on the BTC spot market and simultaneously sell BTC futures when the APY is attractive.

Close both positions upon futures contract expiry to realize profits.

Risk Management:

Ensure you have sufficient margin to hold both positions until expiry.

Monitor funding rates and volatility, which could affect returns.

Conclusion

This script is an essential tool for traders looking to exploit price discrepancies between the BTC spot market and futures market through a cash-and-carry arbitrage strategy. It provides real-time data on spreads, annualized returns (APY), and visual alerts, helping traders make informed decisions and maximize their profit potential.