Bantlar ve Kanallar

The Barking Rat PercentilesPercentile Reversion with Multi-Layered Smoothing

The Barking Rat Percentiles is a multi-tiered reversion strategy based on fixed percentage movements away from the mean, designed to capture price extremes through a structured, practical approach. It combines statistically derived percentile bands, RSI momentum filtering, and ATR-driven exits to identify potential turning points while managing opportunity with precision. The aim is to isolate high-quality reversal opportunities at progressively deeper extremes while avoiding noise and low-conviction setups.

At its core, the strategy measures the current market position relative to long-term percentile thresholds. When price moves significantly beyond these smoothed levels and momentum shows signs of exhaustion, staged entries are triggered. Exits are managed using independent ATR-based take profit and stop loss logic to adapt to varying volatility conditions.

🧠 Core Logic: Tiered Extremes & Structured Management

This strategy is intentionally methodical, layering multiple thresholds and validation checks before highlighting potential setups. By combining percentile-based extremes with momentum confirmation and adaptive trade management, it offers a disciplined and repeatable framework for mean reversion trading.

1. Percentile Thresholds as the Primary Framework

The script calculates the highest high and lowest low over a long lookback period of more than 1000 candles to define the overall price range. It then derives upper and lower percentile thresholds to determine extreme price levels. These thresholds are smoothed using a simple moving average to filter out short-term noise, ensuring that only statistically significant deviations from the mean are considered for potential trades.

2. Multi-Tier Entry Levels

Based on the percentile distance away from the mean, the script plots and references five discrete trigger levels beyond the primary thresholds for both long and short positions. Each tier represents progressively deeper extremes, typically 1–3% beyond the smoothed threshold, balancing the benefits of early entries with the safety of more confirmed extremes. Custom logic ensures only one signal is generated per threshold level, avoiding duplicate entries in the same zone.

3. RSI Momentum Filter

A 14-period RSI filter is applied to prevent entering trades against strong momentum. Long trades are only triggered when RSI falls below 30 (oversold), and short trades only when RSI rises above 70 (overbought). This helps align entries with potential exhaustion points, reducing the risk of entering prematurely into a strong ongoing trend.

4. ATR-Based Trade Management

For each trade sequence, the strategy will exit on the first exit condition met: either the take profit (TP) or the stop loss (SL). Because the TP uses a smaller ATR multiplier, it’s generally closer to the entry price, so most trades will hit the TP before reaching the SL. The SL is intentionally set with a larger ATR multiplier to give the trade room to develop, acting as a protective fallback rather than a frequent exit.

So in practice, you’ll usually see the TP executed for a trade, and the SL only triggers in cases where price moves further against the position than expected.

5. Position Reset Logic

Once price returns to the smoothed threshold region, all entry tiers in that direction are reset. This allows the system to prepare for new opportunities if the market revisits extreme levels, without triggering duplicate trades at the same threshold.

Why These Parameters Were Chosen

Multi-tier thresholds ensure that only meaningful extremes are acted upon, while the long-range SMA provides historical context and filters out noise. The staged entry logic per level balances the desire for early participation with the discipline of risk management. ATR-based TP and SL levels adapt to changing volatility, while the RSI filter improves timing by aligning trades with potential exhaustion points. Together, these elements create a balanced, structured, and repeatable approach to mean reversion trading.

📈 Chart Visuals: Clear & Intuitive

Green “▲” below a candle: Potential long entry

Red “▼” above a candle: Potential short entry

Blue “✔️”: Exit when ATR take profit is hit

Orange “✘”: Exit when ATR stop loss is hit

Tier threshold lines (smoothed upper/lower bounds)

🔔Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that signals are only triggered once fully confirmed.

You must manually set up alerts within your TradingView account. Once configured, you’ll be able to set up one alert per instrument. This one alert covers all relevant signals and exits — ideal for hands-free monitoring.

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: SOLUSDT

Backtesting range: Jul 28, 2025 — Aug 14, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Percentiles strategy is ultra-selective, filtering out over 90% of market noise by enforcing multiple validation layers. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍 What Makes This Strategy Unique?

Multi-Tier Percentile Triggers – Instead of relying on a single overbought/oversold zone, this strategy uses five distinct entry tiers per direction, allowing for staged, precision entries at progressively deeper extremes.

Long-Term Percentile Smoothing – By calculating extremes over a 1000+ candle range and smoothing them with a moving average, the strategy focuses only on statistically significant deviations.

Custom One-Signal-Per-Tier Logic – Prevents duplicate trades at the same threshold level, reducing overtrading and noise.

Dual ATR Exit System – Independent TP and SL levels adapt to volatility. TP uses a smaller ATR multiplier for realistic, achievable exits and generally executes first, while the SL has a larger ATR multiplier to provide protective breathing room if the trade moves further against the position.

Momentum-Aware Filtering – A 14-period RSI filter ensures trades are only taken when momentum is likely exhausted, avoiding entries into strong trends.

Automatic Position Reset – Once price normalizes, tiers reset, allowing for fresh entries without interference from previous trades.

Breakout asia USD/CHF1 — Customizable Parameters

sess1 & sess2: The two time ranges that define the Asian session (e.g., 20:00–23:59 and 00:00–08:00).

Important: format is HHMM-HHMM.

rr: The risk/reward ratio (default = 3.0, meaning TP = 3× risk size).

onePerSess: Toggle to allow only one trade per Asian session or multiple.

bufTicks: Extra margin for the SL beyond the signal candle.

2 — Detecting the Asian Session

The script checks if the candle’s time is inside the first range (sess1) or inside the second range (sess2).

While inside the Asian session, it updates the current high and low.

When the session ends, it locks in these levels as rangeHigh and rangeLow.

3 — Step 1: Detecting the Initial Breakout

Bullish breakout → close above rangeHigh → flag breakoutUp is set to true.

Bearish breakout → close below rangeLow → flag breakoutDown is set to true.

No trade yet — this is just the breakout signal.

4 — Step 2: Waiting for the Retest

If a bullish breakout occurred, wait for the price to return to or slightly below rangeHigh and then close back above it.

If a bearish breakout occurred, wait for the price to return to or slightly above rangeLow and then close back below it.

5 — Entry & Exit

When the retest is confirmed:

strategy.entry() is triggered.

SL = behind the retest confirmation candle (with optional bufTicks margin).

TP = entry price ± RR × risk size.

If onePerSess is enabled, no further trades happen until the next Asian session.

6 — Chart Display

Green line = locked Asian session high.

Red line = locked Asian session low.

Light blue background = active Asian session hours.

Trade entries are shown on the chart when retests occur.

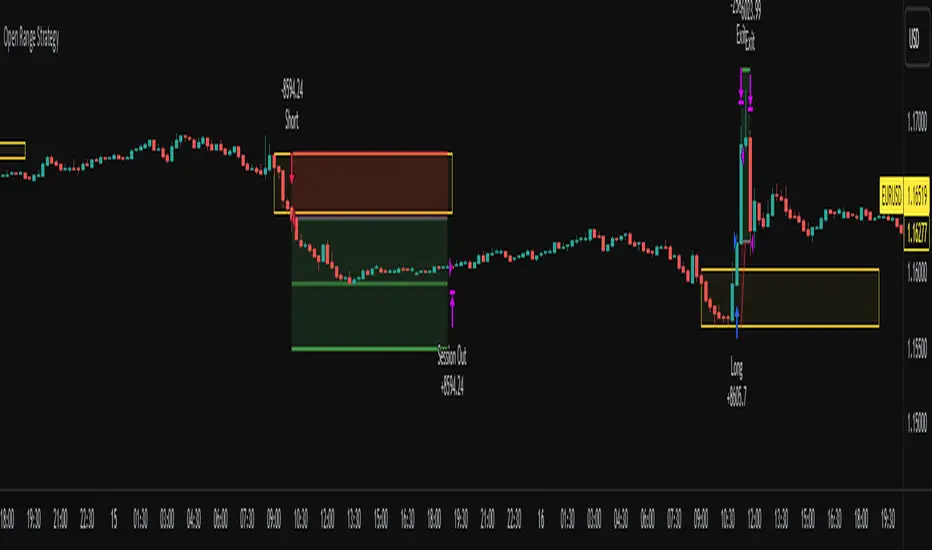

Open Range Breakout Strategy With Multi TakeProfitHello everyone,

For a while, I’ve been wanting to develop new scripts, but I couldn’t decide what to create. Eventually, I came up with the idea of coding traditional and well-known trading strategies—while adding modern features such as multi–take profit options. For the first strategy in this series, I chose the Open Range Strategy .

For those unfamiliar with it, the Open Range Strategy is a trading approach where you define a specific time period at the beginning of a trading session—such as the first 15 minutes, 30 minutes, or 1 hour—and mark the highest and lowest prices within that range. These levels then act as reference points for potential breakouts: if the price breaks above the range, it may signal a long entry; if it breaks below, it may indicate a short entry. This method is popular among day traders for capturing early momentum in the market.

Since this strategy is generally used as an intraday strategy , I added a Trade Session feature. This allows you to define the exact time window during which trades can be opened. Once the session ends, all positions are automatically closed, ensuring trades remain within your chosen intraday period.

Even though it’s a relatively simple concept, I’ve come across many different variations of it. That’s why I created a highly customizable project. Under the Session Settings, you can select the time window you want to define as your range. Whether it’s the first 15-minute candle or the entire first hour, the choice is entirely yours.

For stop-loss placement, there are two different options:

Middle of the Range – The stop loss is placed at the midpoint between the high and low of the defined range, offering a balanced buffer for both bullish and bearish setups.

Top/Bottom of the Range – The stop loss is placed just beyond the range’s high for short trades or just below the range’s low for long trades, providing a more conservative risk approach.

I’ve always been a big fan of the multi take-profit feature, so I added two different take-profit targets to this project. Take profits are calculated based on a Risk-to-Reward Ratio, which you can adjust in the settings. You can also set different position sizes for each target, allowing you to scale out of trades in a way that suits your strategy.

The result is a flexible, user-friendly strategy script that brings together a classic approach with modern risk management tools—ready to be tailored to your trading style

Spread Mean Reversion Strategy [SciQua]╭───────────────────────────────────────╮

Spread Mean Reversion Strategy

╰───────────────────────────────────────╯

This invite-only futures spread strategy applies a statistical mean reversion framework, executing limit orders exclusively at calculated Z-score thresholds for precise, rules-based entries and exits. It is designed for CME-style spreads and synthetic instruments with well-defined reversion tendencies.

╭────────────╮

Core Concept

╰────────────╯

The strategy calculates a rolling mean and standard deviation of a chosen spread or synthetic price series, then computes the Z-score to measure deviation from the mean in standard deviation units.

Long entries trigger when Z crosses upward through a negative entry threshold (`-devEnter`). A buy limit is placed exactly at the price corresponding to that Z-score, optionally offset by a configurable tick amount.

Short entries trigger when Z crosses downward through a positive entry threshold (`+devEnter`). A sell limit is placed at the corresponding threshold price, also with optional offset.

Exits use the same threshold method, with an independent `Close Limit Offset` to fine-tune exit placement.

╭────────────╮

Key Features

╰────────────╯

Persistence filter – Requires the Z-score to remain beyond threshold for a configurable number of bars before entry.

Cooldown after exits – Prevents immediate re-entry to reduce over-trading.

Daily and weekend flattening – Force-flattens positions via limit orders before exchange maintenance breaks and weekend closes.

Auto-rollover detection with persistence – Detects when the second contract month’s daily volume exceeds the first for a set number of days, then blocks new entries (optional).

Configurable tick offsets – Independently adjust entry and exit levels relative to threshold prices.

Minimum spread width filter – Blocks trades when long/short entry thresholds are too close together.

Contract multiplier override – Allows correct sizing for synthetic symbols where `syminfo.pointvalue` is incorrect or missing.

Limit-only execution – All entries, exits, and forced-flat actions are executed with limit orders for price control.

╭────────────────────╮

Entry Blocking Rules

╰────────────────────╯

New trades are blocked:

During daily maintenance break pre-windows

During weekend close pre-windows

After rollover triggers, if `Block After Roll` is enabled

╭────────────────────────╮

Intended Markets & Usage

╰────────────────────────╯

Built for futures spreads and synthetic instruments , including calendar spreads.

Performs best in markets with clear seasonal or statistical mean-reverting tendencies.

Not designed for strongly trending, non-reverting markets.

╭──────────────────────────╮

Risk Management & Defaults

╰──────────────────────────╯

Fixed default position size of 1 contract (qty calc function available for customization).

Realistic commission and slippage assumptions pre-set.

Pyramiding disabled by default.

Default Z-score levels: Entry at ±2.0, Exit at ±0.5.

Separate tick offset controls for entries and exits.

Note: This strategy is for research and backtesting purposes only. Past performance does not guarantee future results. All use is subject to explicit written permission from the author.

ZapTeam Pro Strategy v6 — EMA The Pro Strategy v6 script is a versatile trading strategy for TradingView that combines trend indicators, filters, and levels.

Main features:

EMA 21, EMA 50, EMA 200 — trend detection and entry signals via EMA crossovers.

Ichimoku Cloud (optional) — trend filtering and price position relative to the cloud.

ETH Dominance filter (optional) — filters trades based on Ethereum dominance (ETH.D).

ATR Stop-Loss — dynamic stop-loss based on volatility.

Two take-profits (TP1 and TP2) with optional 50/50 split.

Dynamic Fibonacci Levels — automatic or manual swings, with 1.272 and 1.618 extensions.

Custom S/R Levels — user-defined support/resistance levels.

Level lines extend across the chart and automatically adjust when zooming or panning.

Designed for trading in trending market conditions on any timeframe.

The strategy calculates position size based on percentage risk per equity.

Robotic-ATM V6.6 Professional🤖 Robotic-ATM V6.6 Pro - Advanced Multi-Indicator Algorithmic Trading Strategy

Professional algo system combining 4 proven indicators: R-ATM KISS V5 trend detection, LG_TRSpeed momentum analysis, R-ATM Oscillator scoring, WaveTrend wave analysis. Features 3 signal modes (ALL_IMMEDIATE/ALL_SYNC/PARTIAL_SYNC), advanced risk mgmt with stop-loss/profit targets, daily P&L limits, position controls, and volatility filtering. Real-time dashboard tracks trades, win rate, profit/loss, and drawdown. $300/month subscription, 21-day FREE trial, cancel anytime. 3+3 months free when paying quarterly. Educational purposes only. Past performance doesn't guarantee future results. Trading involves substantial risk. Only trade with capital you can afford to lose. Contact: support@robotic-atm.com | robotic-atm.com | Robotic-ATM Inc.

Robotic-ATM V6.6.3/IO🤖 Robotic-ATM V6.6 3.3 IO - Advanced Multi-Indicator Algorithmic Trading Strategy

Professional algo system combining 4 proven indicators: R-ATM KISS V5 trend detection, LG_TRSpeed momentum analysis, R-ATM Oscillator scoring, WaveTrend wave analysis. Features 3 signal modes (ALL_IMMEDIATE/ALL_SYNC/PARTIAL_SYNC), advanced risk mgmt with stop-loss/profit targets, daily P&L limits, position controls, and volatility filtering. Real-time dashboard tracks trades, win rate, profit/loss, and drawdown. $300/month subscription, 21-day FREE trial, cancel anytime. 3+3 months free when paying quarterly. Educational purposes only. Past performance doesn't guarantee future results. Trading involves substantial risk. Only trade with capital you can afford to lose. Contact: sales@robotic-atm.com | robotic-atm.com | Robotic-ATM Inc.

BB & RSI Trailing Stop StrategySimple BB & RSI generated using AI, gets 60% on S&P 500 with the right settings

Keltner Channel Based Grid Strategy # KC Grid Strategy - Keltner Channel Based Grid Trading System

## Strategy Overview

KC Grid Strategy is an innovative grid trading system that combines the power of Keltner Channels with dynamic position sizing to create a mean-reversion trading approach. This strategy automatically adjusts position sizes based on price deviation from the Keltner Channel center line, implementing a systematic grid-based approach that capitalizes on market volatility and price oscillations.

## Core Principles

### Keltner Channel Foundation

The strategy builds upon the Keltner Channel indicator, which consists of:

- **Center Line**: Moving average (EMA or SMA) of the price

- **Upper Band**: Center line + (ATR/TR/Range × Multiplier)

- **Lower Band**: Center line - (ATR/TR/Range × Multiplier)

### Grid Trading Logic

The strategy implements a sophisticated grid system where:

1. **Position Direction**: Inversely correlated to price position within the channel

- When price is above center line → Short positions

- When price is below center line → Long positions

2. **Position Size**: Proportional to distance from center line

- Greater deviation = Larger position size

3. **Grid Activation**: Positions are adjusted only when the difference exceeds a predefined grid threshold

### Mathematical Foundation

The core calculation uses the KC Rate formula:

```

kcRate = (close - ma) / bandWidth

targetPosition = kcRate × maxAmount × (-1)

```

This creates a mean-reversion system where positions increase as price moves further from the mean, expecting eventual return to equilibrium.

## Parameter Guide

### Time Range Settings

- **Start Date**: Beginning of strategy execution period

- **End Date**: End of strategy execution period

### Core Parameters

1. **Number of Grids (NumGrid)**: Default 12

- Controls grid sensitivity and position adjustment frequency

- Higher values = More frequent but smaller adjustments

- Lower values = Less frequent but larger adjustments

2. **Length**: Default 10

- Period for moving average and volatility calculations

- Shorter periods = More responsive to recent price action

- Longer periods = Smoother, less noisy signals

3. **Grid Coefficient (kcRateMult)**: Default 1.33

- Multiplier for channel width calculation

- Higher values = Wider channels, less frequent trades

- Lower values = Narrower channels, more frequent trades

4. **Source**: Default Close

- Price source for calculations (Close, Open, High, Low, etc.)

- Close price typically provides most reliable signals

5. **Use Exponential MA**: Default True

- True = Uses EMA (more responsive to recent prices)

- False = Uses SMA (equal weight to all periods)

6. **Bands Style**: Default "Average True Range"

- **Average True Range**: Smoothed volatility measure (recommended)

- **True Range**: Current bar's volatility only

- **Range**: Simple high-low difference

## How to Use

### Setup Instructions

1. **Apply to Chart**: Add the strategy to your desired timeframe and instrument

2. **Configure Parameters**: Adjust settings based on market characteristics:

- Volatile markets: Increase Grid Coefficient, reduce Number of Grids

- Stable markets: Decrease Grid Coefficient, increase Number of Grids

3. **Set Time Range**: Define your backtesting or live trading period

4. **Monitor Performance**: Watch strategy performance metrics and adjust as needed

### Optimal Market Conditions

- **Range-bound markets**: Strategy performs best in sideways trending markets

- **High volatility**: Benefits from frequent price oscillations around the mean

- **Liquid instruments**: Ensures efficient order execution and minimal slippage

### Position Management

The strategy automatically:

- Calculates optimal position sizes based on account equity

- Adjusts positions incrementally as price moves through grid levels

- Maintains risk control through maximum position limits

- Executes trades only during specified time periods

## Risk Warnings

### ⚠️ Important Risk Considerations

1. **Trending Market Risk**:

- Strategy may underperform or generate losses in strong trending markets

- Mean-reversion assumption may fail during sustained directional moves

- Consider market regime analysis before deployment

2. **Leverage and Position Size Risk**:

- Strategy uses pyramiding (up to 20 positions)

- Large positions may accumulate during extended moves

- Monitor account equity and margin requirements closely

3. **Volatility Risk**:

- Sudden volatility spikes may trigger multiple rapid position adjustments

- Consider volatility filters during high-impact news events

- Backtest across different volatility regimes

4. **Execution Risk**:

- Strategy calculates on every tick (calc_on_every_tick = true)

- May generate frequent orders in volatile conditions

- Ensure adequate execution infrastructure and consider transaction costs

5. **Parameter Sensitivity**:

- Performance highly dependent on parameter optimization

- Over-optimization may lead to curve-fitting

- Regular parameter review and adjustment may be necessary

## Suitable Scenarios

### Ideal Market Conditions

- **Sideways/Range-bound markets**: Primary use case

- **Mean-reverting instruments**: Forex pairs, some commodities

- **Stable volatility environments**: Consistent ATR patterns

- **Liquid markets**: Major currency pairs, popular stocks/indices

## Important Notes

### Strategy Limitations

1. **No Stop Loss**: Strategy relies on mean reversion without traditional stop losses

2. **Capital Requirements**: Requires sufficient capital for grid-based position sizing

3. **Market Regime Dependency**: Performance varies significantly across different market conditions

## Disclaimer

This strategy is provided for educational and research purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Users should thoroughly test the strategy and understand its mechanics before risking real capital. The author assumes no responsibility for trading losses incurred through the use of this strategy.

---

# KC网格策略 - 基于肯特纳通道的网格交易系统

## 策略概述

KC网格策略是一个创新的网格交易系统,它将肯特纳通道的力量与动态仓位调整相结合,创建了一个均值回归交易方法。该策略根据价格偏离肯特纳通道中心线的程度自动调整仓位大小,实施系统化的网格方法,利用市场波动和价格振荡获利。

## 核心原理

### 肯特纳通道基础

该策略建立在肯特纳通道指标之上,包含:

- **中心线**: 价格的移动平均线(EMA或SMA)

- **上轨**: 中心线 + (ATR/TR/Range × 乘数)

- **下轨**: 中心线 - (ATR/TR/Range × 乘数)

### 网格交易逻辑

该策略实施复杂的网格系统:

1. **仓位方向**: 与价格在通道中的位置呈反向关系

- 当价格高于中心线时 → 空头仓位

- 当价格低于中心线时 → 多头仓位

2. **仓位大小**: 与距离中心线的距离成正比

- 偏离越大 = 仓位越大

3. **网格激活**: 只有当差异超过预定义的网格阈值时才调整仓位

### 数学基础

核心计算使用KC比率公式:

```

kcRate = (close - ma) / bandWidth

targetPosition = kcRate × maxAmount × (-1)

```

这创建了一个均值回归系统,当价格偏离均值越远时仓位越大,期望最终回归均衡。

## 参数说明

### 时间范围设置

- **开始日期**: 策略执行期间的开始时间

- **结束日期**: 策略执行期间的结束时间

### 核心参数

1. **网格数量 (NumGrid)**: 默认12

- 控制网格敏感度和仓位调整频率

- 较高值 = 更频繁但较小的调整

- 较低值 = 较少频繁但较大的调整

2. **长度**: 默认10

- 移动平均线和波动率计算的周期

- 较短周期 = 对近期价格行为更敏感

- 较长周期 = 更平滑,噪音更少的信号

3. **网格系数 (kcRateMult)**: 默认1.33

- 通道宽度计算的乘数

- 较高值 = 更宽的通道,较少频繁的交易

- 较低值 = 更窄的通道,更频繁的交易

4. **数据源**: 默认收盘价

- 计算的价格来源(收盘价、开盘价、最高价、最低价等)

- 收盘价通常提供最可靠的信号

5. **使用指数移动平均**: 默认True

- True = 使用EMA(对近期价格更敏感)

- False = 使用SMA(对所有周期等权重)

6. **通道样式**: 默认"平均真实范围"

- **平均真实范围**: 平滑的波动率测量(推荐)

- **真实范围**: 仅当前K线的波动率

- **范围**: 简单的高低价差

## 使用方法

### 设置说明

1. **应用到图表**: 将策略添加到您所需的时间框架和交易品种

2. **配置参数**: 根据市场特征调整设置:

- 波动市场:增加网格系数,减少网格数量

- 稳定市场:减少网格系数,增加网格数量

3. **设置时间范围**: 定义您的回测或实盘交易期间

4. **监控表现**: 观察策略表现指标并根据需要调整

### 最佳市场条件

- **区间震荡市场**: 策略在横盘趋势市场中表现最佳

- **高波动性**: 受益于围绕均值的频繁价格振荡

- **流动性强的品种**: 确保高效的订单执行和最小滑点

### 仓位管理

策略自动:

- 根据账户权益计算最优仓位大小

- 随着价格在网格水平移动逐步调整仓位

- 通过最大仓位限制维持风险控制

- 仅在指定时间段内执行交易

## 风险警示

### ⚠️ 重要风险考虑

1. **趋势市场风险**:

- 策略在强趋势市场中可能表现不佳或产生损失

- 在持续方向性移动期间均值回归假设可能失效

- 部署前考虑市场制度分析

2. **杠杆和仓位大小风险**:

- 策略使用金字塔加仓(最多20个仓位)

- 在延长移动期间可能积累大仓位

- 密切监控账户权益和保证金要求

3. **波动性风险**:

- 突然的波动性激增可能触发多次快速仓位调整

- 在高影响新闻事件期间考虑波动性过滤器

- 在不同波动性制度下进行回测

4. **执行风险**:

- 策略在每个tick上计算(calc_on_every_tick = true)

- 在波动条件下可能产生频繁订单

- 确保充足的执行基础设施并考虑交易成本

5. **参数敏感性**:

- 表现高度依赖于参数优化

- 过度优化可能导致曲线拟合

- 可能需要定期参数审查和调整

## 适用场景

### 理想市场条件

- **横盘/区间震荡市场**: 主要用例

- **均值回归品种**: 外汇对,某些商品

- **稳定波动性环境**: 一致的ATR模式

- **流动性市场**: 主要货币对,热门股票/指数

## 注意事项

### 策略限制

1. **无止损**: 策略依赖均值回归而无传统止损

2. **资金要求**: 需要充足资金进行基于网格的仓位调整

3. **市场制度依赖性**: 在不同市场条件下表现差异显著

## 免责声明

该策略仅供教育和研究目的。过往表现不保证未来结果。交易涉及重大损失风险,并非适合所有投资者。用户应在投入真实资金前彻底测试策略并理解其机制。作者对使用此策略产生的交易损失不承担任何责任。

---

**Strategy Version**: Pine Script v6

**Author**: Signal2Trade

**Last Updated**: 2025-8-9

**License**: Open Source (Mozilla Public License 2.0)

Vegas Tunnel StrategyVegas Tunnel Strategy is a trend-following breakout system based on exponential moving averages (EMAs). It uses a "tunnel" formed by the 144 EMA and 169 EMA to identify the market's long-term trend direction. Entry signals are generated when a shorter-term EMA (12 EMA) breaks above or below this tunnel, confirming momentum alignment.

Long Setup: Price and EMA12 are above the tunnel (EMA144 < EMA169); entry on pullback near the tunnel.

Short Setup: Price and EMA12 are below the tunnel (EMA144 > EMA169); entry on rebound near the tunnel.

Exit Rules: Fixed stop loss below/above the tunnel or based on ATR; take profit at 1.5–2× the risk.

This strategy works best on 4H or daily charts and is suitable for trending assets like FX pairs, gold, oil, or indices.

[Stratégia] VWAP Mean Magnet v9 (Simple Alert)This strategy is specifically designed for a ranging (sideways-moving) Bitcoin market.

A trade is only opened and signaled on the chart if all three of the following conditions are met simultaneously at the close of a candle:

Zone Entry

The price must cross into the signal zone: the red band for a Short (sell) position, or the green band for a Long (buy) position.

RSI Confirmation

The RSI indicator must also confirm the signal. For a Short, it must go above 65 (overbought condition). For a Long, it must fall below 25 (oversold condition).

Volume Filter

The volume on the entry candle cannot be excessively high. This safety filter is designed to prevent trades during risky, high-momentum breakouts.

Martin Strategy - No Loss Exit v3Martin Strategy - No Loss Exit v3Martin Strategy - No Loss Exit v3Martin Strategy - No Loss Exit v3

AUD/USD 1-Min Scalping Strategy with LabelsHere’s a complete TradingView Pine Script v5 for the 1-minute AUD/USD scalping strategy we just discussed. This strategy uses:

EMA 13 and EMA 26 for trend filtering

Bollinger Bands for volatility extremes

RSI (4) for momentum confirmation

Dynamic DCA Envelope – Beta V1.1Dynamic DCA Envelope-Beta V1.1 is a preview version of a Dollar-Cost Averaging (DCA) strategy designed for trending or volatile markets.

-Long Positions Only

-Intended for Cryptocurrency, but can be used in any market

-1 and 4 hour timeframe

-Average Commissions 0.1%-0.3% per trade (Cryptocurrency)

What it does:

This strategy identifies buying opportunities when price closes below a dynamic envelope (based on EMA). After 3 consecutive closes below the lower envelope, the system arms a buy condition. A DCA buy-in is triggered when price bounces by a configurable percentage from the trailing low. The strategy supports up to 3 buy-ins, each equally sized, and closes the entire position at a fixed take profit or stop loss.

How it works:

-Entry logic is based on price deviation from an EMA envelope

-Waits for 3 closes below the envelope to detect weakness

-Uses bounce percentage from the lowest point to trigger each buy

-Includes cooldown logic between buys to avoid clustering

-All positions are closed when TP or SL is hit

How to use it:

-Use on trending assets with volatility (e.g., crypto, tech stocks)

-Adjust inputs to match asset behavior:

-EMA Length

-Envelope Offset %

-Bounce % (Trailing DCA)

-Take Profit / Stop Loss

-View strategy performance in the Strategy Tester tab

What’s unique:

Unlike most DCA scripts that immediately average down, this version includes:

-Trigger logic requiring multiple closes below trend

-Bounce-based entry to avoid catching a falling knife

-Cooldown resets to prevent overtrading

-A true entry–wait–buy–reset loop mimicking disciplined execution

*This is a beta version intended as a preview. A full Pro version is in development, which includes:

-SmartScaling logic

-Trailing take profit

-Multi-symbol scanning

-Backtest range limits

-Risk-adjusted filtering

The Real DealThis strategy uses a closed source 3 EMA band, as well as a few other closed source indicators that I prefer no to mention right now. Play with it and tell me what you think. The stock settings are definitely not what I use.

Bollinger Bands SMA 20_2 StrategyMean reversion strategy using Bollinger Bands (20-period SMA with 2.0 standard deviation bands).

Trade Triggers:

🟢 BUY SIGNAL:

When: Price crosses above the lower Bollinger Band

Logic: Price has hit oversold territory and is bouncing back

Action: Places a long position with stop at the lower band

🔴 SELL SIGNAL:

When: Price crosses below the upper Bollinger Band

Logic: Price has hit overbought territory and is pulling back

Action: Places a short position with stop at the upper band

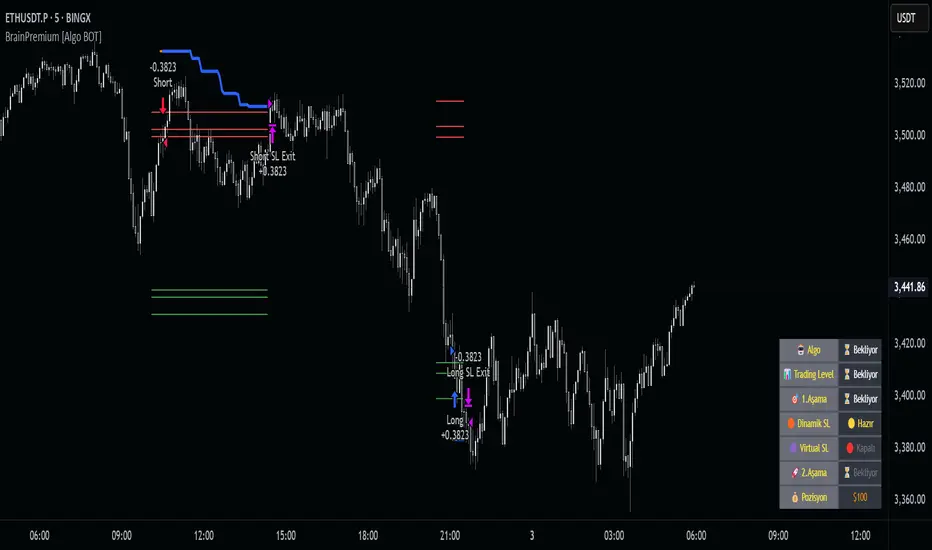

Brain Premium [ALGO]💡 Brain Premium ALGO

Brainpremium ALGO is a strategy algorithm that analyzes a two-phase regional liquidity structure and only opens positions on price breakouts occurring within these liquidity zones.

This system is developed based on the market experience of manual traders and automatically executes trade decisions using AI-like rules and specific triggers.

💡 Two-Phase Liquidity-Based Entry Strategy

This strategy operates by detecting liquidity sweep zones and confirmed reversal signals:

🔹 Phase 1 – Liquidity Sweep:

Price is expected to sweep areas where equal highs/lows or liquidity clusters exist. These zones are considered potential reversal levels.

🔹 Phase 2 – Confirmed Entry:

After liquidity is swept, entries are triggered only by confirmed reversal signals such as structural breaks, inside bars, or breakouts in the opposite direction.

✅ Entries are triggered only when liquidity and reversal confirmation occur simultaneously.

🎯 This approach targets high-probability, low-risk trades.

⚙️ Key Features

🔍 Dynamic Liquidity Detection — Automatically identifies liquidity zones.

🧩 Modular Entry Options (1–2–3) — Allows opening positions via different strategy paths.

🛡️ Dynamic Stop Loss System — Stop Loss adjusts as price moves favorably.

📈 Advanced Risk Management — Adjustable Take Profit, Stop Loss, leverage, balance, and mode.

🔔 JSON Alert Support — Connects to platforms like BingX via webhook.

🧾 Information Panel — Displays real-time trade data and strategy status.

📊 Backtest & Default Settings

Strategy tests are conducted with realistic and sustainable parameters:

Parameter Value

Trading Balance: $100 (%10 of total wallet)

Leverage: 10x

Stop Loss: 1%

Take Profit Type : High TP (optional: Low and Risky also available)

Entry Option 1 (optional: 2 and 3 also available)

Mode: NORMAL

Commission 0.05%

Dynamic Stop Loss: Enabled

Timeframe: 5 minute

Pair ETH/USDT

Duration: 30 days

🧭 Usage Instructions

Add Brain Premium ALGO to your TradingView chart.

Set position size, leverage, and SL/TP levels from the settings panel.

Select entry option (1, 2, or 3).

Activate backtesting and alert systems to monitor the strategy.

⚠️ Disclaimer

This strategy is not financial advice. Past performance does not guarantee future results. Trade only with capital you can afford to risk and always test thoroughly in a demo environment first.

TOT Strategy, The ORB Titan (Configurable)This is a strategy script adapted from Deniscr 's indicator script found here:

All feedback welcome!

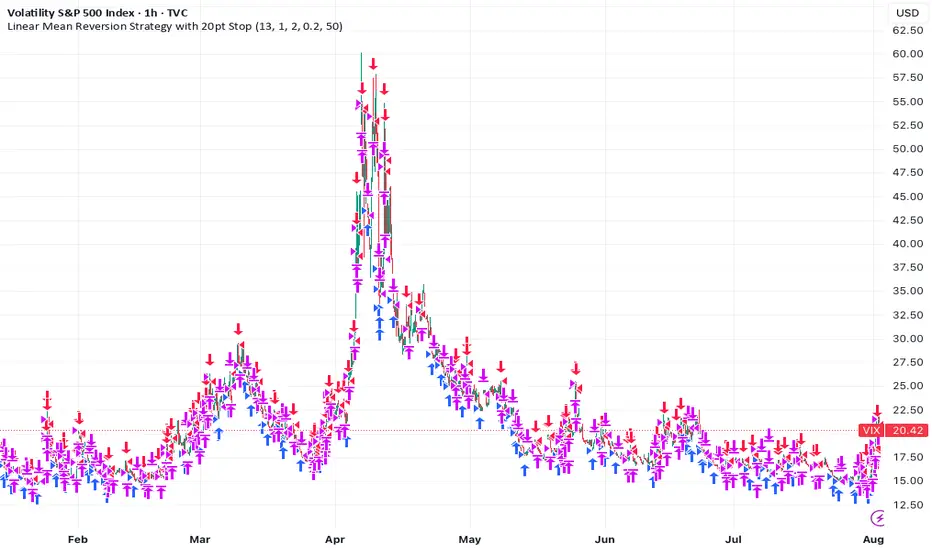

Linear Mean Reversion Strategy📘 Strategy Introduction: Linear Mean Reversion with Fixed Stop

This strategy implements a simple yet powerful mean reversion model that assumes price tends to oscillate around a dynamic average over time. It identifies statistically significant deviations from the moving average using a z-score, and enters trades expecting a return to the mean.

🧠 Core Logic:

A z-score is calculated by comparing the current price to its moving average, normalized by standard deviation, over a user-defined half-life window.

Trades are entered when the z-score crosses a threshold (e.g., ±1), signaling overbought or oversold conditions.

The strategy exits positions either when price reverts back near the mean (z-score close to 0), or if a fixed stop loss of 100 points is hit, whichever comes first.

⚙️ Key Features:

Dynamic mean and volatility estimation using moving average and standard deviation

Configurable z-score thresholds for entry and exit

Position size scaling based on z-score magnitude

Fixed stop loss to control risk and avoid prolonged drawdowns

🧪 Use Case:

Ideal for range-bound markets or assets that exhibit stationary behavior around a mean, this strategy is especially useful on assets with mean-reverting characteristics like currency pairs, ETFs, or large-cap stocks. It is best suited for traders looking for short-term reversions rather than long-term trends.

BTC 1m Chop Top/Bottom Reversal (Stable Entries)Strategy Description: BTC 5m Chop Top/Bottom Reversal (Stable Entries)

This strategy is engineered to capture precise reversal points during Bitcoin’s choppy or sideways price action on the 5-minute timeframe. It identifies short-term tops and bottoms using a confluence of volatility bands, momentum indicators, and price structure, optimized for high-probability scalping and intraday reversals.

Core Logic:

Volatility Filter: Uses an EMA with ATR bands to define overextended price zones.

Momentum Divergence: Confirms reversals using RSI and MACD histogram shifts.

Price Action Filter: Requires candle confirmation in the direction of the trade.

Locked Signal Logic: Prevents repaints and disappearing trades by confirming signals only once per bar.

Trade Parameters:

Short Entry: Above upper band + overbought RSI + weakening MACD + bearish candle

Long Entry: Below lower band + oversold RSI + strengthening MACD + bullish candle

Take Profit: ±0.75%

Stop Loss: ±0.4%

This setup is tuned for traders using tight risk control and leverage, where execution precision and minimal drawdown tolerance are critical.