Golden BOS Strategy - ChecklistA clean, mechanical on-chart checklist designed for multi-timeframe traders using the Golden BOS / Institutional Retracement Framework.

This tool helps you stay disciplined by tracking each requirement of the strategy in real time:

Included Criteria

4H Bias: Bullish or bearish macro structure

1H Structure: Push/pull phase + golden zone retracement

5M Entry Model:

Break of Structure (BOS)

5M golden zone retracement

POI validation (OB/FVG/Breaker)

Final micro BOS or rejection confirmation

Risk Filters:

Session validity (London / NY)

Red news avoidance

Stop-loss placement check

Liquidity-based target confirmation

Purpose

This overlay ensures every trade meets strict criteria before execution, removing emotion and improvisation. Ideal for backtesting, forward testing, and staying consistent during live market conditions.

Golden BOS Strategy — Description

The Golden BOS Strategy is a structured, multi-timeframe trading system designed to capture high-probability continuation moves during London and New York sessions. The strategy combines institutional concepts with Fibonacci-based retracements to identify discounted entry zones aligned with higher-timeframe direction.

Using the 4H timeframe, traders establish the daily macro bias and identify the dominant trend. The 1H chart is then used to confirm the current phase of market structure, distinguishing between impulsive “push” moves and corrective “pullback” phases. A Fibonacci retracement is applied to the most recent 1H impulse leg to define a high-value discount or premium zone where entries become valid.

Execution takes place on the 5-minute chart. Once price reaches the 1H golden zone (61.8–78.6%), a Break of Structure (BOS) is required to confirm a shift in short-term momentum. A second Fibonacci retracement is then drawn on the 5M impulse leg that caused the BOS, and price must retrace back into the 5M golden zone. Traders refine their entry using a confluence point of interest (POI) such as a Fair Value Gap (FVG), Order Block, Breaker Block, or Inverse FVG, ideally accompanied by a final micro BOS or rejection candle.

Risk management is strict and rule-driven. Stop loss is placed beyond the extreme wick of the POI, while take-profit targets are set at logical liquidity pools in the direction of the higher-timeframe trend. The strategy avoids red-folder news and only allows trades during active sessions to ensure optimal volatility and reliability.

The Golden BOS Strategy is designed to impose discipline, reduce discretionary errors, and give traders a repeatable, mechanical framework for navigating trending markets with precision.

Backtester

Adaptive Trend SelectorThe Adaptive Trend Selector is a comprehensive trend-following tool designed to automatically identify the optimal moving average crossover strategy. It features adjustable parameters and an integrated backtester that delivers institutional-grade insights into the recommended strategy. The model continuously adapts to new data in real time by evaluating multiple moving average combinations, determining the best performing lengths, and presenting the backtest results in a clear, color-coded table that benchmarks performance against the buy-and-hold strategy.

At its core, the model systematically backtests a wide range of moving average combinations to identify the configuration that maximizes the selected optimization metric. Users can choose to optimize for absolute returns or risk-adjusted returns using the Sharpe, Sortino, or Calmar ratios. Alternatively, users can enable manual optimization to test custom fast and slow moving average lengths and view the corresponding backtest results. The label displays the Compounded Annual Growth Rate (CAGR) of the strategy, with the buy-and-hold CAGR in parentheses for comparison. The table presents the backtest results based on the fast and slow lengths displayed at the top:

Sharpe = CAGR per unit of standard deviation.

Sortino = CAGR per unit of downside deviation.

Calmar = CAGR relative to maximum drawdown.

Max DD = Largest peak-to-trough decline in value.

Beta (β) = Return sensitivity relative to buy-and-hold.

Alpha (α) = Excess annualized risk-adjusted returns.

Win Rate = Ratio of profitable trades to total trades.

Profit Factor = Total gross profit per unit of losses.

Expectancy = Average expected return per trade.

Trades/Year = Average number of trades per year.

This indicator is designed with flexibility in mind, enabling users to specify the start date of the backtesting period and the preferred moving average strategy. Supported strategies include the Exponential Moving Average (EMA), Simple Moving Average (SMA), Wilder’s Moving Average (RMA), Weighted Moving Average (WMA), and Volume-Weighted Moving Average (VWMA). To minimize overfitting, users can define constraints such as a minimum and maximum number of trades per year, as well as an optional optimization margin that prioritizes longer, more robust combinations by requiring shorter-length strategies to exceed this threshold. The table follows an intuitive color logic that enables quick performance comparison against buy-and-hold (B&H):

Sharpe = Green indicates better than B&H, while red indicates worse.

Sortino = Green indicates better than B&H, while red indicates worse.

Calmar = Green indicates better than B&H, while red indicates worse.

Max DD = Green indicates better than B&H, while red indicates worse.

Beta (β) = Green indicates better than B&H, while red indicates worse.

Alpha (α) = Green indicates above 0%, while red indicates below 0%.

Win Rate = Green indicates above 50%, while red indicates below 50%.

Profit Factor = Green indicates above 2, while red indicates below 1.

Expectancy = Green indicates above 0%, while red indicates below 0%.

In summary, the Adaptive Trend Selector is a powerful tool designed to help investors make data-driven decisions when selecting moving average crossover strategies. By optimizing for risk-adjusted returns, investors can confidently identify the best lengths using institutional-grade metrics. While results are based on the selected historical period, users should be mindful of potential overfitting, as past results may not persist under future market conditions. Since the model recalibrates to incorporate new data, the recommended lengths may evolve over time.

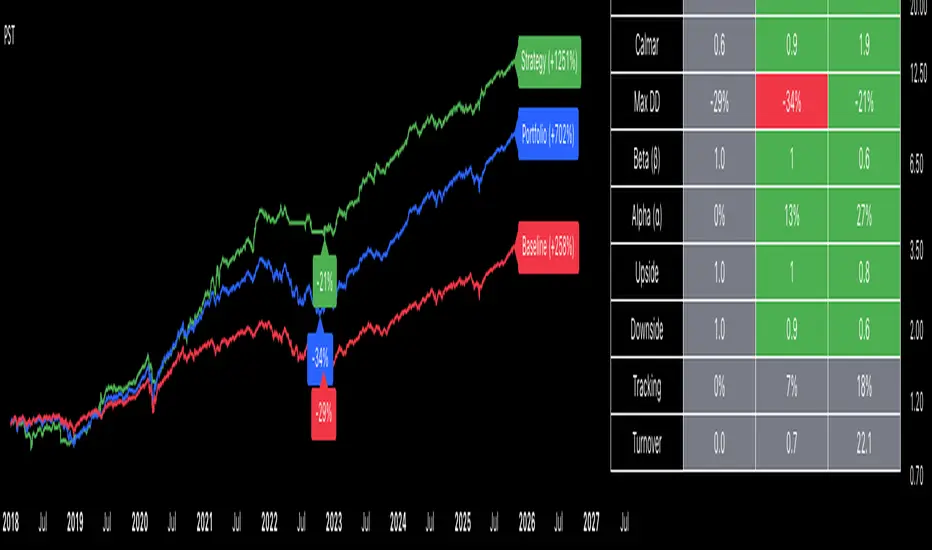

Portfolio Strategy TesterThe Portfolio Strategy Tester is an institutional-grade backtesting framework that evaluates the performance of trend-following strategies on multi-asset portfolios. It enables users to construct custom portfolios of up to 30 assets and apply moving average crossover strategies across individual holdings. The model features a clear, color-coded table that provides a side-by-side comparison between the buy-and-hold portfolio and the portfolio using the risk management strategy, offering a comprehensive assessment of both approaches relative to the benchmark.

Portfolios are constructed by entering each ticker symbol in the menu, assigning its respective weight, and reviewing the total sum of individual weights displayed at the top left of the table. For strategy selection, users can choose between Exponential Moving Average (EMA), Simple Moving Average (SMA), Wilder’s Moving Average (RMA), Weighted Moving Average (WMA), Moving Average Convergence Divergence (MACD), and Volume-Weighted Moving Average (VWMA). Moving average lengths are defined in the menu and apply only to strategy-enabled assets.

To accurately replicate real-world portfolio conditions, users can choose between daily, weekly, monthly, or quarterly rebalancing frequencies and decide whether cash is held or redistributed. Daily rebalancing maintains constant portfolio weights, while longer intervals allow natural drift. When cash positions are not allowed, capital from bearish assets is automatically redistributed proportionally among bullish assets, ensuring the portfolio remains fully invested at all times. The table displays a comprehensive set of widely used institutional-grade performance metrics:

CAGR = Compounded annual growth rate of returns.

Volatility = Annualized standard deviation of returns.

Sharpe = CAGR per unit of annualized standard deviation.

Sortino = CAGR per unit of annualized downside deviation.

Calmar = CAGR relative to maximum drawdown.

Max DD = Largest peak-to-trough decline in value.

Beta (β) = Sensitivity of returns relative to benchmark returns.

Alpha (α) = Excess annualized risk-adjusted returns relative to benchmark.

Upside = Ratio of average return to benchmark return on up days.

Downside = Ratio of average return to benchmark return on down days.

Tracking = Annualized standard deviation of returns versus benchmark.

Turnover = Average sum of absolute changes in weights per year.

Cumulative returns are displayed on each label as the total percentage gain from the selected start date, with green indicating positive returns and red indicating negative returns. In the table, baseline metrics serve as the benchmark reference and are always gray. For portfolio metrics, green indicates outperformance relative to the baseline, while red indicates underperformance relative to the baseline. For strategy metrics, green indicates outperformance relative to both the baseline and the portfolio, red indicates underperformance relative to both, and gray indicates underperformance relative to either the baseline or portfolio. Metrics such as Volatility, Tracking Error, and Turnover ratio are always displayed in gray as they serve as descriptive measures.

In summary, the Portfolio Strategy Tester is a comprehensive backtesting tool designed to help investors evaluate different trend-following strategies on custom portfolios. It enables real-world simulation of both active and passive investment approaches and provides a full set of standard institutional-grade performance metrics to support data-driven comparisons. While results are based on historical performance, the model serves as a powerful portfolio management and research framework for developing, validating, and refining systematic investment strategies.

Risk Reward Optimiser [ChartPrime]█ CONCEPTS

In modern day strategy optimization there are few options when it comes to optimizing a risk reward ratio. Users frequently need to experiment and go through countless permutations in order to tweak, adjust and find optimal in their data.

Therefore we have created the Risk Reward Optimizer.

The Risk Reward Optimizer is a technical tool designed to provide traders with comprehensive insights into their trading strategies.

It offers a range of features and functionalities aimed at enhancing traders' decision-making process.

With a focus on comprehensive data, it is there to help traders quickly and efficiently locate Risk Reward optimums for inbuilt of custom strategies.

█ Internal and external Signals:

The script can optimize risk to reward ratio for any type of signals

You can utilize the following :

🔸Internal signals ➞ We have included a number of common indicators into the optimizer such as:

▫️ Aroon

▫️ AO (Awesome Oscillator)

▫️ RSI (Relative Strength Index)

▫️ MACD (Moving Average Convergence Divergence)

▫️ SuperTrend

▫️ Stochastic RSI

▫️ Stochastic

▫️ Moving averages

All these indicators have 3 conditions to generate signals :

Crossover

High Than

Less Than

🔸External signal

▫️ by incorporating your own indicators into the analysis. This flexibility enables you to tailor your strategy to your preferences.

◽️ How to link your signal with the optimizer:

In order to be able to analysis your signal we need to read it and to do so we would need to PLOT your signal with a defined value

plot( YOUR LONG Condition ? 100 : 0 , display = display.data_window)

█ Customizable Risk to Reward Ratios:

This tool allows you to test seven different customizable risk to reward ratios , helping you determine the most suitable risk-reward balance for your trading strategy. This data-driven approach takes the guesswork out of setting stop-loss and take-profit levels.

█ Comprehensive Data Analysis:

The tool provides a table displaying key metrics, including:

Total trades

Wins

Losses

Profit factor

Win rate

Profit and loss (PNL)

This data is essential for refining your trading strategy.

🔸 It includes a tooltip for each risk to reward ratio which gives data for the:

Most Profitable Trade USD value

Most Profitable Trade % value

Most Profitable Trade Bar Index

Most Profitable Trade Time (When it occurred)

Position and size is adjustable

█ Visual insights with histograms:

Visualize your trading performance with histograms displaying each risk to reward ratio trade space, showing total trades, wins, losses, and the ratio of profitable trades.

This visual representation helps you understand the strengths and weaknesses of your strategy.

It offers tooltips for each RR ratio with the average win and loss percentages for further analysis.

█ Dynamic Highlighting:

A drop-down menu allows you to highlight the maximum values of critical metrics such as:

Profit factor

Win rate

PNL

for quick identification of successful setups.

█ Stop Loss Flexibility:

You can adjust stop-loss levels using three different calculation methods:

ATR

Pivot

VWAP

This allows you to align risk-reward ratios with your preferred risk tolerance.

█ Chart Integration:

Visualize your trades directly on your price chart, with each trade displayed in a distinct color for easy tracking.

When your take-profit (TP) level is reached , the tool labels the corresponding risk-reward ratio for that specific TP, simplifying trade management.

█ Detailed Tooltips:

Tooltips provide deeper insights into your trading performance. They include information about the most profitable trade, such as the time it occurred, the bar index, and the percentage gain. Histogram tooltips also offer average win and loss percentages for further analysis.

█ Settings:

█ Code:

In summary, the Risk Reward Optimizer is a data-driven tool that offers traders the ability to optimize their risk-reward ratios, refine their strategies, and gain a deeper understanding of their trading performance. Whether you're a day trader, swing trader, or investor, this tool can help you make informed decisions and improve your trading outcomes.

Trade Helper [Trading Nerd]Position Size Calculator / Lot Size Calculator

Disclaimer: I do my best to avoid wrong calculations and bugs. I provide this indicator without warranties of any kind. You bear all risks associated with the use of this indicator.

Inputs:

Market: Adds a name tag to the Table to keep track of the trades.

Entry Price: The entry Price of the Position.

Entry Time: The entry Time/Candle of the Position. If Stop Loss Type is 'ATR' or 'HH/LL' the Value for this is calculated by this Candle.

Stop Loss Type: Changes the Stop Loss Type.

Direction: Define if the trade direction is 'Long' or 'Short'. Has no effect on Stop Loss Type 'Custom'. For this you can just set the Stop Loss below/above the Entry Price .

ATR Multiplier: Multiplies the ATR Value by this number. Has only an effect on Stop Loss Type 'ATR'.

HH/LL Lookback Length: Lookback length for determine Highest High/Lowest Low value. Has only an effect on Stop Loss Type 'HH/LL'.

Custom SL Price: The Stop Loss Price if the Stop Loss Type is set to 'Custom'.

Risk Reward Ratio: The Risk is multiplied by this number to determine the Take Profit Price.

Balance: Balance Amount and Currency

Contract Size: The Position Size is divided by this number. E.G. in Forex one Lot is 100.000 Contracts. Change this Value depending on your Broker and Market.

Risk in %: Percent that is risked of the Balance for one Trade.