OPEN-SOURCE SCRIPT

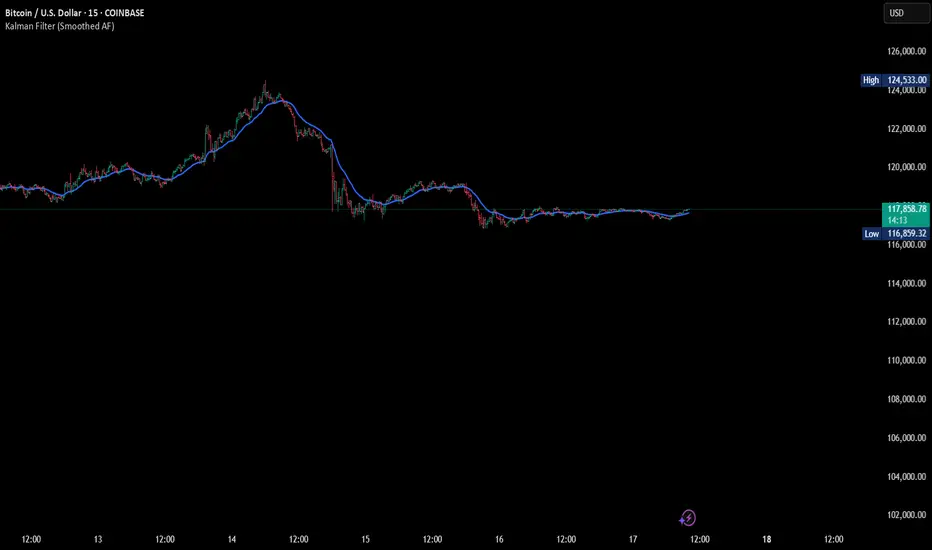

Kalman Filter (Smoothed)

The Kalman Filter is a recursive statistical algorithm that smooths noisy price data while adapting dynamically to new information. Unlike simple moving averages or EMAs, it minimizes lag by balancing measurement noise (R) and process noise (Q), giving traders a clean, adaptive estimate of true price action.

🔹 Core Features

Real-time recursive estimation

Adjustable noise parameters (R = sensitivity to price, Q = smoothness vs. responsiveness)

Reduces market noise without heavy lag

Overlay on chart for direct comparison with raw price

🔹 Trading Applications

Smoother trend visualization compared to traditional MAs

Spotting true direction during volatile/sideways markets

Filtering out market “whipsaws” for cleaner signals

Building blocks for advanced quant/trading models

⚠️ Note: The Kalman Filter is a state-space model; it doesn’t predict future price, but smooths past and present data into a more reliable signal.

🔹 Core Features

Real-time recursive estimation

Adjustable noise parameters (R = sensitivity to price, Q = smoothness vs. responsiveness)

Reduces market noise without heavy lag

Overlay on chart for direct comparison with raw price

🔹 Trading Applications

Smoother trend visualization compared to traditional MAs

Spotting true direction during volatile/sideways markets

Filtering out market “whipsaws” for cleaner signals

Building blocks for advanced quant/trading models

⚠️ Note: The Kalman Filter is a state-space model; it doesn’t predict future price, but smooths past and present data into a more reliable signal.

Açık kaynak kodlu komut dosyası

Gerçek TradingView ruhuyla, bu komut dosyasının mimarı, yatırımcıların işlevselliğini inceleyip doğrulayabilmesi için onu açık kaynaklı hale getirdi. Yazarı tebrik ederiz! Ücretsiz olarak kullanabilseniz de, kodu yeniden yayınlamanın Topluluk Kurallarımıza tabi olduğunu unutmayın.

Feragatname

Bilgiler ve yayınlar, TradingView tarafından sağlanan veya onaylanan finansal, yatırım, alım satım veya diğer türden tavsiye veya öneriler anlamına gelmez ve teşkil etmez. Kullanım Koşulları bölümünde daha fazlasını okuyun.

Açık kaynak kodlu komut dosyası

Gerçek TradingView ruhuyla, bu komut dosyasının mimarı, yatırımcıların işlevselliğini inceleyip doğrulayabilmesi için onu açık kaynaklı hale getirdi. Yazarı tebrik ederiz! Ücretsiz olarak kullanabilseniz de, kodu yeniden yayınlamanın Topluluk Kurallarımıza tabi olduğunu unutmayın.

Feragatname

Bilgiler ve yayınlar, TradingView tarafından sağlanan veya onaylanan finansal, yatırım, alım satım veya diğer türden tavsiye veya öneriler anlamına gelmez ve teşkil etmez. Kullanım Koşulları bölümünde daha fazlasını okuyun.