OPEN-SOURCE SCRIPT

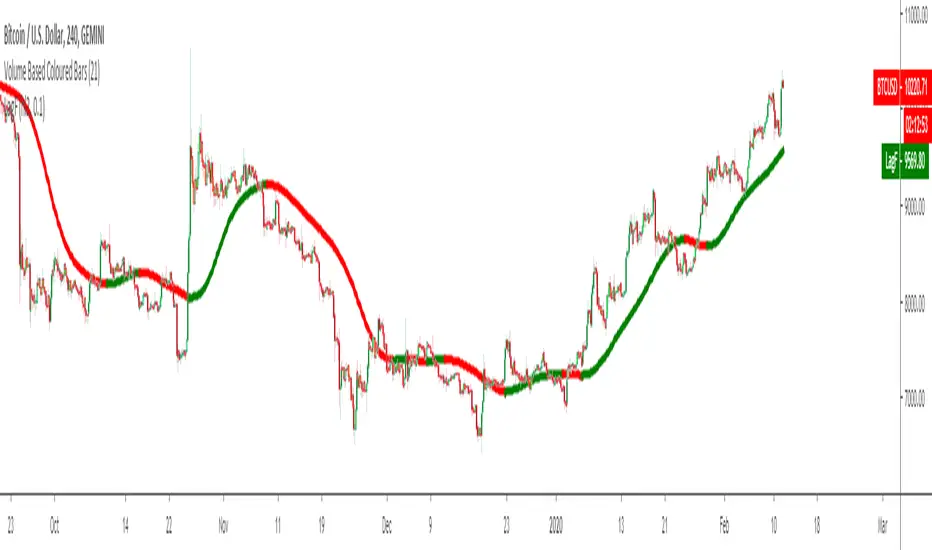

Laguerre Filter

Laguerre Filter is developed by John EHLERS. change alpha coefficient to increase/decrease lag and smoothness.

This is a four element Laguerre Filter derived from Finite Impulse Response (FIR) filter by changing

the relative amplitudes of the samples.

However, the lag of a FIR filter is

approximately half the filter length. The result is that if we want greater smoothing we

must accept the additional lag in conventional filters. Laguerre is the method says EHLERS in one of his articles about Laguerre Filter.

"The FIR filter has a lag of only 1.5 bars and only moderately

smoothes the price data. On the other hand, the Laguerre filter is dramatically

smoother and also has significant lag. You can decrease the smoothing and the lag by

decreasing the damping factor. When the damping factor is reduced to zero, the

Laguerre filter is identical to the FIR filter. This is a simple way to control the action of a

moving average and still use only a few data samples in the calculation."

For further information here is the article about the indicator by the developer John EHLERS.

forex-station.com/download/file.php?id=3326725

kivancozbilgic

This is a four element Laguerre Filter derived from Finite Impulse Response (FIR) filter by changing

the relative amplitudes of the samples.

However, the lag of a FIR filter is

approximately half the filter length. The result is that if we want greater smoothing we

must accept the additional lag in conventional filters. Laguerre is the method says EHLERS in one of his articles about Laguerre Filter.

"The FIR filter has a lag of only 1.5 bars and only moderately

smoothes the price data. On the other hand, the Laguerre filter is dramatically

smoother and also has significant lag. You can decrease the smoothing and the lag by

decreasing the damping factor. When the damping factor is reduced to zero, the

Laguerre filter is identical to the FIR filter. This is a simple way to control the action of a

moving average and still use only a few data samples in the calculation."

For further information here is the article about the indicator by the developer John EHLERS.

forex-station.com/download/file.php?id=3326725

kivancozbilgic

Açık kaynak kodlu komut dosyası

Gerçek TradingView ruhuna uygun olarak, bu komut dosyasının oluşturucusu bunu açık kaynaklı hale getirmiştir, böylece yatırımcılar betiğin işlevselliğini inceleyip doğrulayabilir. Yazara saygı! Ücretsiz olarak kullanabilirsiniz, ancak kodu yeniden yayınlamanın Site Kurallarımıza tabi olduğunu unutmayın.

Telegram t.me/AlgoRhytm

YouTube (Turkish): youtube.com/c/kivancozbilgic

YouTube (English): youtube.com/c/AlgoWorld

YouTube (Turkish): youtube.com/c/kivancozbilgic

YouTube (English): youtube.com/c/AlgoWorld

Feragatname

Bilgiler ve yayınlar, TradingView tarafından sağlanan veya onaylanan finansal, yatırım, işlem veya diğer türden tavsiye veya tavsiyeler anlamına gelmez ve teşkil etmez. Kullanım Şartları'nda daha fazlasını okuyun.

Açık kaynak kodlu komut dosyası

Gerçek TradingView ruhuna uygun olarak, bu komut dosyasının oluşturucusu bunu açık kaynaklı hale getirmiştir, böylece yatırımcılar betiğin işlevselliğini inceleyip doğrulayabilir. Yazara saygı! Ücretsiz olarak kullanabilirsiniz, ancak kodu yeniden yayınlamanın Site Kurallarımıza tabi olduğunu unutmayın.

Telegram t.me/AlgoRhytm

YouTube (Turkish): youtube.com/c/kivancozbilgic

YouTube (English): youtube.com/c/AlgoWorld

YouTube (Turkish): youtube.com/c/kivancozbilgic

YouTube (English): youtube.com/c/AlgoWorld

Feragatname

Bilgiler ve yayınlar, TradingView tarafından sağlanan veya onaylanan finansal, yatırım, işlem veya diğer türden tavsiye veya tavsiyeler anlamına gelmez ve teşkil etmez. Kullanım Şartları'nda daha fazlasını okuyun.